Regulators forced trillions of dollars worth of derivatives through central clearing after the global financial crisis of 2008 to help avoid repeats of that meltdown. Now, the coronavirus-inspired market slump is providing the greatest test yet of these crucial financial institutions.

Central counterparties, or clearing houses, act as middlemen in derivatives trades to prevent losses cascading through the financial system if one of the parties involved in trades defaults. But concentrating such enormous amounts of risk in a handful of CCPs has also led many to question whether these institutions are secure enough.

Nineteen prominent banks, asset managers and other financial institutions signed a paper only a few weeks ago urging regulators to consider a broad range of measures to bolster the resilience of CCPs, including forcing them to hold more capital.

Clearing houses say they are well prepared for the current crisis. The same goes for the largest clearing member banks, which have far higher capital reserves than 12 years ago. But there are signs of increased strain across the wider clearing landscape.

On March 20, CME Group said it had auctioned off the portfolios of Ronin Capital, one of its clearing members, after Ronin was unable to meet its capital requirements. Six days later, ABN AMRO said its clearing arm had suffered a US$200m net loss related to one of its US clients.

Clearing experts highlight spikes in margin calls for listed derivatives in particular, and warn that further defaults could follow. Many are also concerned about the potential for losses arising from operational failures or cyber attacks at CCPs in this febrile market environment.

"We do have significant concerns about the amount of capital and resources CCPs have outside of the default waterfall," said a senior risk manager at a large financial institution.

The default waterfall refers to the order of financial resources that a CCP can use to cover losses arising from the default of a clearing member.

SHOCK ABSORBERS

Clearing houses have existed for centuries as shock absorbers in financial transactions. Regulators decided to force huge tracts of the US$640trn over-the-counter derivatives market through these hubs following the 2008 crisis, when concerns over the solvency of a handful of firms threatened to bring down the entire financial system.

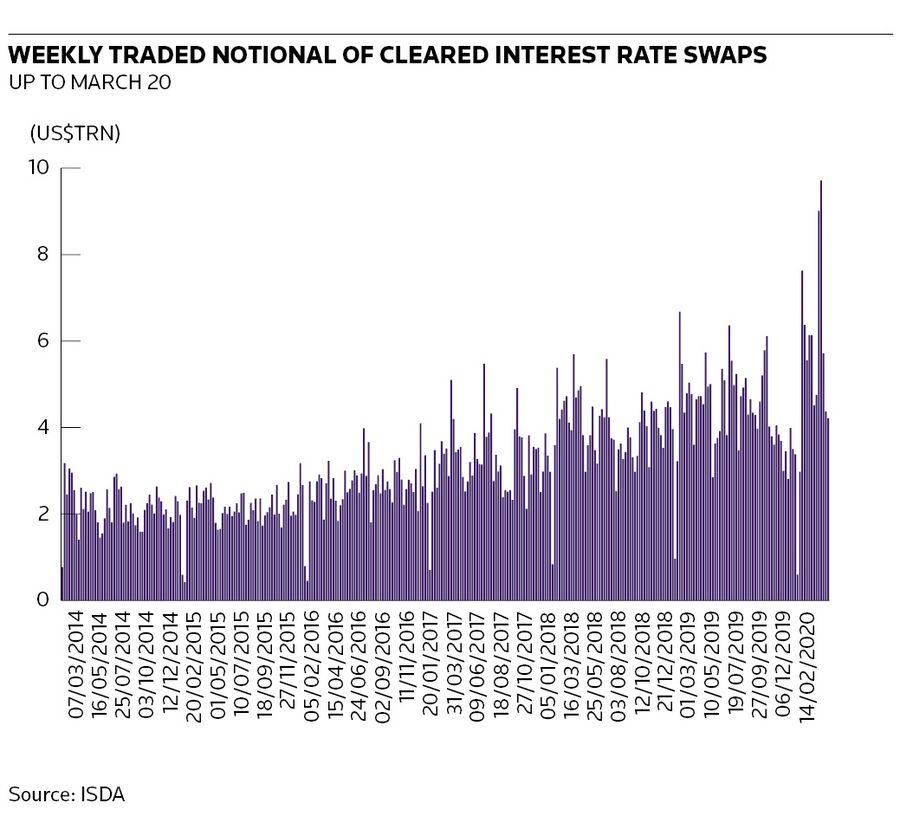

There has been a spike in trading volumes during the coronavirus selloff, testing clearing systems like never before. A record US$10.7trn in interest-rate swaps traded in the week ended March 6, according to data provided by the International Swaps and Derivatives Association. Over 90% – or US$9.7trn – was cleared through CCPs. There have also been record trading volumes in the volatile credit-default swap market.

LCH Group, the largest clearer for interest-rate swaps, sent a note to clients on Monday stating it had “robust business continuity arrangements in place to ensure the safe and orderly conduct of our businesses and clearing operations around the world”, revealing it had asked some staff to work from home “remotely or in split site teams”.

It added that it continued to operate all clearing services as normal “notwithstanding the recent market volatility and trading volumes".

The Association for Financial Markets in Europe recently said it and three other trade bodies were gathering key information about the preparedness and response plans of market infrastructure providers, including exchanges and clearing houses in light of the coronavirus and the resulting market volatility.

“It is a test. I understand CCPs are preparing very well,” said Ulrich Karl, head of clearing services at ISDA.

“Now, recovery and resolution rules for banks are much more sophisticated and banks are better capitalised compared to the 2008 crisis. It’s far less likely big banks will default and, if it happens, then CCPs have resources to withstand shocks.”

FIERCE DEBATE

Despite the apparently improved resiliency of the wider system, there has still been a fierce industry debate about whether CCPs need reform.

The 19 firms that called for clearing houses to hold more capital as part of a raft of measures aimed at increasing their resilience included Allianz Global Investors, BlackRock, Citigroup, Goldman Sachs and JP Morgan.

“There isn’t a market-wide consensus yet on the recovery and resolution framework for CCPs. How should the risks and burdens be balanced? In the current CCP rules, quite a lot of that burden falls on clearing members. Regulators will have to make the final judgement on that,” said Karl.

Many expect the extreme increases in margin calls for listed derivatives in particular to cause further defaults among smaller clearing firms.

ABN AMRO, one of the signatories to the clearing paper, said the losses it took came from a client that had a “specific strategy, trading US options and futures, and failed to meet the minimum risk and margin requirements following extreme stress and dislocations in US markets". The bank decided to close out the client positions to prevent further losses, it added.

“We’re seeing continual jumps in margin requirements," said the senior risk manager.