When Boris Johnson visited The Charter Building, a swanky new office block at the heart of his Uxbridge constituency, for an event in mid-January, he was greeted by a surprising figure. Instead of being welcomed by the leader of the local council, as might be expected on such occasions, the prime minister was met by the leader of a rival council from 20 miles away.

Ian Harvey had travelled north as leader of Spelthorne Borough Council – and master of a vast property empire that includes the building hosting that day's event. In just three years, the tiny council – one of the smallest in the country – had bought up £1bn of real estate. The Charter Building, acquired for £136m, was one of its latest purchases.

As the two men chatted in the busy foyer, Harvey explained how the portfolio was generating a steady stream of income for Spelthorne, an area to the south-west of London immediately south of Heathrow Airport. Even after paying interest on money borrowed to fund the purchases, surplus rent contributed £10m to the council's budget. Johnson was impressed and asked why his own council wasn't doing the same, Harvey later posted on his LinkedIn account.

Four months on, the building's foyer is eerily quiet, and Spelthorne's outsized property bet is now threatening to backfire. Commercial property has been hit hard by the coronavirus pandemic, as some tenants struggle to pay rent and others reconsider office working entirely. Land Securities, a big UK landlord, says office rental income could drop 20% this year, while Aviva predicts a 15% fall in commercial property prices.

Spelthorne is vulnerable on a number of fronts: The Charter Building was just one-quarter rented out when the virus hit; three of its properties have principal tenants in the badly affected shared workspace business – including beleaguered operator WeWork; while two of its office blocks are part of the complex around Heathrow Airport, now facing years of subdued demand.

'BORROWED TOO MUCH'

Until now, the £50m of rental income from Spelthorne's property empire has been more than enough to pay the £35m annual cost of servicing its hefty debt pile. The surplus has been put into a rainy-day sinking fund and provided £10m year to fund local services - half the council's budget. The fear is that a big drop in rental income could force the council to make deep cuts to frontline services at a time when they are needed most as it prioritises the servicing of its debts.

"Spelthorne borrowed too much," said Rob Whiteman, chief executive at the Chartered Institute of Public Finance and Accountancy, which has written a prudential code for councils. "You don't have to be accountant of the year to know that that's quite a lot of excessive leverage and commercial risk. Councils should not take on debt for yield that they can't afford if things go wrong."

EXTREME EXAMPLE

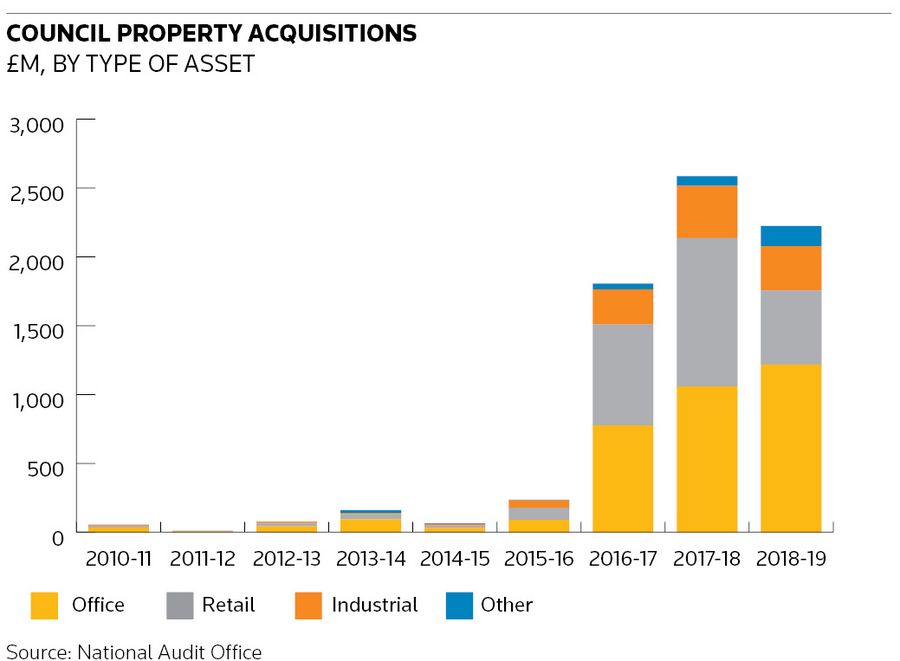

While Spelthorne is an extreme example, it is not alone. Up and down the UK, local authorities spent £6.6bn on commercial property in the three years leading up to March 2019 – almost all of it funded by debt. Office buildings have been popular, accounting for almost half of all purchases, but councils have bought all kinds: supermarkets, hotels, gyms, warehouses, even a lingerie factory.

That's been possible because of an unusual lending facility open to councils. Officials just need to make a phone call to the Public Works Loan Board, an arm of the Treasury, stating how much they want. Because of the separation between local and central government, they don't need to explain why they want the loan or how it will be repaid. Within two days, the money is transferred.

The arrangement has allowed many councils to pile up debt with little external oversight. Annual borrowing has doubled in recent years, pushing total council debt over £120bn, most of it provided by the PWLB. The set-up has allowed a handful of small councils including Woking, Warrington, Croydon and Spelthorne to rack up more than £1bn of debt each – no questions asked.

"In the private sector, an organisation the size of Spelthorne wouldn't have been able to attract that amount of leverage and borrowing," said Whiteman.

Spelthorne has debts of £1.1bn and total income from council tax, business rates and government grants of just £14m. That works out at a debt-to-income ratio of 80 times. If its annual rental income of £50m is included, leverage comes down to about 17 times.

"The majority of councils continue to use the prudential code. However, for a few councils that were overexposed through borrowing for commercial purposes ... we are quite worried about them," Whiteman said.

LITTLE SCRUTINY

Critics say that investment decisions at UK councils are often made by officials with no commercial property experience and that there is an absence of effective scrutiny at the local level. The most aggressive borrowers are often councils dominated by a single political party.

Certainly Spelthorne has been subject to criticism. Its auditor KPMG found "significant weaknesses" in processes around its first acquisition in 2016 – the sale and leaseback of a BP research centre in Sunbury for £385m. Few Spelthorne councillors have commercial property experience, although Harvey does have a background as a buy-to-let landlord. The Conservatives have run the council since it was created in 1973.

Lawrence Nichols, a councillor for the Liberal Democrats, the main opposition on the council to the Conservatives, said council meetings dominated by the ruling party did not provide effective scrutiny and that the portfolio's positive contribution to the budget has blinded many local people to the risks. "Central government has been taking money away from councils. Spelthorne has been able to maintain and, to some degree, expand certain services because it's generated this income. It is a fabulous good news story if you don't want to look at the downside risks."

CLAMPDOWN

Some moves have been made to clamp down on excessive borrowing by councils. CIPFA tightened up its prudential code, but it remains optional. The PWLB last year hiked rates to deter councils and ruled out lending for pure profit – although there are loopholes if a project benefits the local area. The National Audit Office has also recommended a series of changes to address the issue.

But all of that may be too little too late. A handful of councils are now highly leveraged and heavily exposed to a commercial property market facing its biggest crisis for decades. Few have much financially to fall back on: most councils are living hand to mouth after successive cuts to their budgets. There has been a 30% real-terms decline in councils' spending power over the last decade.

At the same time, the pandemic is creating additional strains. The opposition Labour Party says councils will need to cut spending by 20% because of the crisis. At the same time, they are facing a social care funding shortfall of £3.5bn because of increased strains on social care directly linked to the coronavirus outbreak.

SINKING FUND

Harvey acknowledged that Spelthorne had "problems" with its property portfolio but said that it had managed to collect 91% of the rent due to it for the current quarter and had agreed with tenants the rescheduling of a further 8%. He also said that the council had built up a £20m sinking fund over the past three years that could be used if tenants failed to pay, which would help shield frontline services from cuts.

"Obviously like everybody else we've got one or two problems," he told IFR. "But we have, as part of our financial modelling for each property, put in significant provisions for a sinking fund to cover void periods. That sinking fund is over and above the £10m a year that is going into support the normal services of the council. Clearly that then gives us quite a significant buffer and leeway."

He added that a potential drop in property values was not a big concern. "Unless you actually go and dispose of property, there is actually no loss solidified. When we bought each of our properties we very carefully considered each on its own merits. And we were very very careful. They are all within what we call our Heathrow area of economic influence. They are all in areas of strong demand."

Central government, which is planning a further clampdown on commercial property acquisitions by local councils, will be watching closely how the Spelthorne experiment fares in the current economic backdrop, both because what happens to Spelthorne is likely to happen to other councils and because if Spelthorne's £1bn property bet were to go wrong it would have to step in.

But Harvey is sticking to his guns. Without the investments, the situation in the borough would have been very different.

"We wouldn't be in the town hall – that would have been sold as a building site," he said. "We would probably be operating out of a converted warehouse unit on an industrial estate. Our day centres would be closed. We'd be collecting bins once a fortnight. All the statutory services would be at the absolute minimum. There would be nothing other than that which is legally required."