On March 23, the day the S&P 500 sank to its lowest ebb in more than three years, Mark Kiesel convened a conference call to deliver a simple message to clients: now is the time to buy high-grade US corporate debt.

“This is a once in a decade opportunity,” Kiesel, Pimco's chief investment officer for global credit, told the hundreds of clients sitting in Asia, Europe and the US.

The sales pitch from the largest active bond management firm in the world came against a bleak backdrop. Deaths from the novel coronavirus were mounting in the US and Europe and markets were in full-blown panic mode.

But Kiesel outlined a number of reasons to buy. Market volatility was peaking, the growth in virus cases was set to slow with stricter distancing measures and – most importantly – a massive government and central bank response was on its way that would underpin credit markets.

Those reasons still hold true today, Kiesel argues, predicting returns in the high single digits for US corporate bonds this year.

“US investment-grade corporate bonds got incredibly cheap relative to default risk,” he told IFR in an interview. “We basically rang the bell. We said on a scale from one to 10, this is a nine.”

UNPRECEDENTED RESPONSE

Pimco's client call came on the same day the US Federal Reserve said it would buy corporate debt for the first time alongside a raft of other measures aimed at steadying markets. The US government, meanwhile, was preparing to unleash trillions of dollars in fiscal stimulus packages to support the economy.

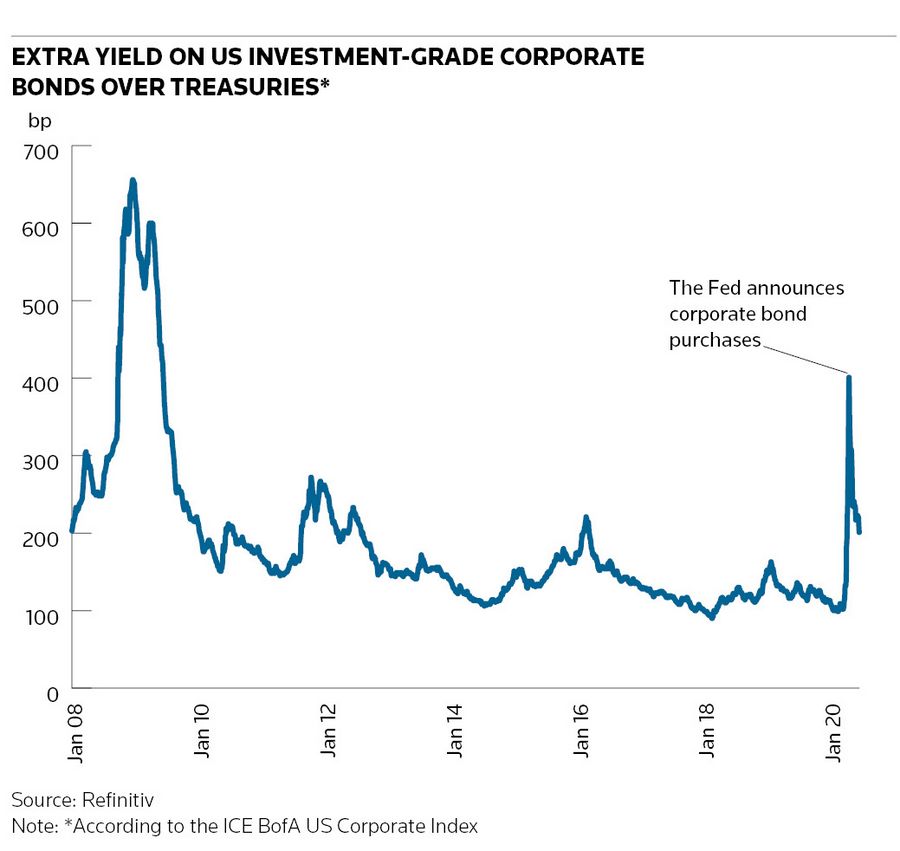

After a tumultuous few weeks, markets began to stage a recovery. The extra yield investors demand to hold US high-grade corporate bonds over Treasuries dropped from more than four percentage points – its highest in over a decade – to about two percentage points now, according to the ICE BofA US Corporate Index.

“The US has been the most powerful in terms of the policy response,” said Kiesel. “We’re talking about running fiscal deficits and an expansion of the Fed’s balance sheet we haven’t seen since World War Two. What we’ve seen over the last two months is truly unprecedented.”

Investors appeared to heed the call, pouring US$4.1bn into Pimco’s three largest investment-grade credit funds in April after withdrawing about US$2.5bn in March, according to estimates from Morningstar.

Another Fed policy – establishing central bank swap lines to make it cheaper for foreign entities to access US dollars – was instrumental in encouraging European and Japanese investors to buy. Faced with negative rates at home, they could suddenly purchase US corporate bonds hedged back to their own currency at their highest yields in four to five years, Kiesel said.

"Hedging costs have collapsed," he added.

New sales of high-grade US corporate debt broke records in March and April, topping half a trillion US dollars in total, providing ample opportunities to put money to work.

Kiesel says Pimco snapped up the bonds of investment-grade US companies still generating free cashflow across sectors including cable, telecommunications, cell towers, healthcare and pharmaceuticals.

“We’re lending to companies that are actually holding up very well, even in this global crisis,” he said.

TOTAL RETURNS

Kiesel was one of a group of senior executives the US$1.8trn asset manager turned to following co-founder Bill Gross’s acrimonious departure in 2014, taking over management of Gross’s Total Return Fund alongside Scott Mather, head of US core strategies, and the recently-retired Mihir Worah.

The Total Return Fund, which once nearly totalled US$300bn in assets, has shrunk dramatically – to US$67bn. Still, it remains one of the largest such funds in the industry, outperforming 82% of peers since Gross departed, according to Morningstar.

This year, the fund was up 4.1% at the end of April, compared with 1.6% for its peer group, Morningstar said. Kiesel attributes this to a cautious stance on corporate bonds in particular at the start of the year.

“We didn’t think the valuations on credit warranted being overweight," he said. "Over the past two months, we’ve been able to essentially switch from defence to offence."

BUYING OPPORTUNITY

Kiesel concedes that they did not get every call right, such as owning some bonds in the travel and tourism sector heading into the crisis. Pimco’s largest US investment-grade fund was down nearly 9% in March, about 1.7 percentage points worse off than a peer group it had outperformed in the previous two years.

"If we had known there was going to be a global shutdown, we probably would not have had that exposure,” he said.

But he argues Pimco identified the buying opportunity ahead of time, first flagging the opportunity in a March 20 video.

The fund rebounded 4.6% in April and Kiesel believes the outlook for credit returns is still good. Spreads on US high-grade bonds are currently in the top 15% of the past 30 years in terms of attractiveness, he said.

“As the economy starts to recover in the third quarter, these spreads should start to tighten," Kiesel said.

Drawing parallels to the aftermath of the 2008 financial crisis, he argues bondholders should benefit in the coming months at shareholders’ expense, as companies repair balance sheets.

“When you have a severe recession, companies become more bondholder-friendly,” he said. “The pendulum has shifted to the bondholder.”