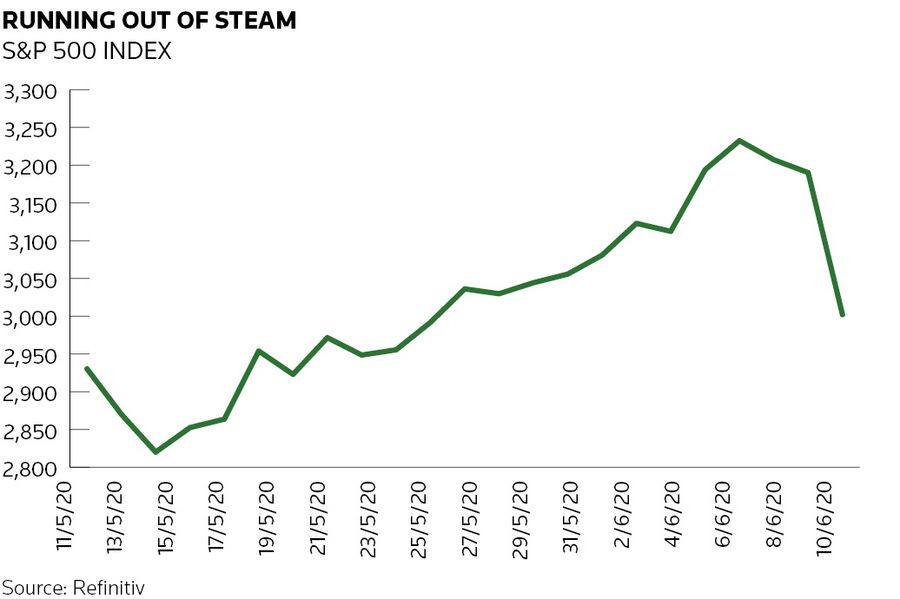

Questions about the intensity of the credit binge were being raised towards the end of last week after US and European equity markets suffered their biggest one-day falls since March on Thursday, bringing doubts about whether the pace would be sustained.

A sober assessment of the US economic outlook by Federal Reserve Chair Jerome Powell on Wednesday, and a jump in reported coronavirus cases in some US states in the south and west on Thursday, led to renewed selling.

Whether this becomes a prolonged sell-off or just a minor correction of a market that had risen too fast, too soon remains to be seen, but both Powell's comments and the coronavirus data delivered a reality check to investors who had begun to get excited about the prospect of a quick economic recovery.

"I think we needed it as the market was too frothy and issuers were getting greedy," said a senior banker on Friday.

Bankers may now have to reassess their pipelines and the speed at which they planned to bring deals into the market. "We had a few issuers early in the week that said 'no' as we were a few basis points wider. Now I guess they are 25bp wider. So that could mean they say 'no way, I need to get the 25bp back' or they could say 'OK, I messed up and this could retrace more'. It's too early to tell," said the banker.

The good news for bond markets is that the technical support is still huge. "Investors – and the ECB – are still buying. We will just need to see higher new-issue premiums. Net-net, I think we slow a bit, but don't stop," said the banker.

Even on Thursday as the S&P 500 fell nearly 6%, some bond issuers still managed to print deals. While a public holiday in parts of Europe meant the euro market took a breather, three US high-yield issuers priced deals and ThaiOil sold a US$1bn dual-tranche offering – inside fair value too – with some of the paper going to US accounts.

The second half of the week was in stark contrast to the first half as primary markets on both sides of the Atlantic were busy – despite the odd no-go call.

While sovereigns led the way, with five eurozone governments raising funds and three other European nations pricing publicly syndicated bonds, the credit markets across the world were also active as investors gravitated towards lower-rated issuers and riskier structures.

"The huge bid for bank capital, corporate hybrids, Asian high-yield and so on is incredible," said another senior banker earlier in the week.

The market backdrop was so good ahead of Wednesday's FOMC meeting that some thought it was even better than at the start of the year even if credit spreads haven't recovered to the tights of that period.

"The market is on fire and probably better than January and February when it was thought we were in a utopian phase," said a syndicate banker before Powell's comments.

REALITY CHECK?

At €269bn, publicly syndicated issuance by European sovereigns in the euro and sterling markets is already almost double the amount raised in the whole of 2019. No other year in recent times has seen €200bn of issuance.

As for euro issuance overall, the total for the year has already surpassed €900bn. The first three days of last week saw about €60bn of issuance – from SSA through to high-yield – with the week shortened by the Corpus Christi holiday on Thursday.

It is an even more incredible story in the US where investment-grade issuance volume of US$1.1trn is just US$27bn shy of the amount raised in the whole of 2019. The full-year record of US$1.33trn set in 2017 looks set to be smashed.

But while supply has boomed ever since central banks began pumping unprecedented amounts of liquidity into the financial system in response to the coronavirus outbreak, the rally was causing a sense of disquiet in some quarters.

"I personally don't buy this strength. Short term fine; there is a huge amount of cash trying to find a home and certain sectors, such as tech, will benefit and rightly should be strong. But give it three to six months and I think it has to unravel as the reality and costs of Covid are seen," said one fund manager.

Others agreed that there will be an eventual fallout. "Maybe financial markets have now just been commoditised by fiscal and monetary stimulus, the latter mostly. It's simply now too much money chasing too few financial assets, whether that is bonds or stocks," wrote Tim Ash, EM sovereign strategist at BlueBay.

"And the instruments themselves now have no relationship to the underlying assets or investments, whether that is companies or sovereigns. There has to be a price for all this, surely. Maybe later on in inflation, or perhaps bad policy choices."

In the meantime, though, the fear of missing out pushed investors into corners of the market they would not have looked at just a few weeks ago.

"It looks like the yield hunt has reached its illogically logical height," said Olga Budnovits, a portfolio manager at Main Partners.

TAKING ADVANTAGE

Borrowers can hardly be blamed for taking advantage. In emerging markets, for example, supply from Africa tentatively started again even though several governments from the region are seeking debt relief.

Helios Towers (B2/B), a telecommunications company in Africa with a portfolio of around 7,000 towers across five countries, priced a US$750m 5.5-year non-call two issue at a yield of 7.125%. That compared with initial talk of the 7.75% area.

Initially the company was targeting a US$425m deal to fund a tender offer on its US$600mn 9.125% senior notes due 2022.

But such was the level of interest following a day of marketing, the tender was cancelled and the deal was upsized with the proceeds now to be used to fully take out the 2022s at their call date next month.

Another regional issuer, Africa Finance Corp (A3, negative outlook) was also in the market on the same day. The pan-African multilateral institution, based in Nigeria, sold a US$700m five-year bond at a yield of 3.25%, signifying a minimal premium at most.

"The screen was full on Tuesday and order books everywhere were stellar. Fish aren't biting – they're swallowing the whole bloody arm you hold out," said the syndicate banker.

Another example of the growing interest in esoteric credits was evident in the euro corporate market as three unrated issuers – Portuguese utility Galp Energia, French small appliance manufacturer SEB, and Iliad, a telecommunications operator across France and Italy – raised funds. Galp and SEB had not issued since 2017.

"It was not that long ago that you would have advised against unrated borrowers issuing, but the market is in good shape," said another syndicate banker as these deals priced.

MOMENTUM PLAY

Deutsche Borse and VW, meanwhile, maintained the momentum in the recently reopened corporate hybrid market.

"It is amazing how some of those credits that a few months ago you would have been wary of have really rallied," said a banker at one of the leads as VW priced its €3bn dual-tranche offering.

"Hybrids are of great interest to us at the moment. I am getting something like a Double B yield on a bond from what is usually a very high quality issuer," said an investor.

"Given the yield I can find in senior, even if I go to the more riskier issuers which I don't really want to do, there is a clear benefit to hybrids and we have actually increased their share in our portfolio."

IN ON THE ACT

High-yield issuers were also getting in on the act. Following only a trickle of deals in European primary over the past three months, supply began to pick up.

Leading the way was Virgin Media as it dipped into the euro, sterling and US dollar markets to clean up its debt stack prior to its merger with O2.

"Finally the European issuers are coming out of hiding," said a high-yield analyst.

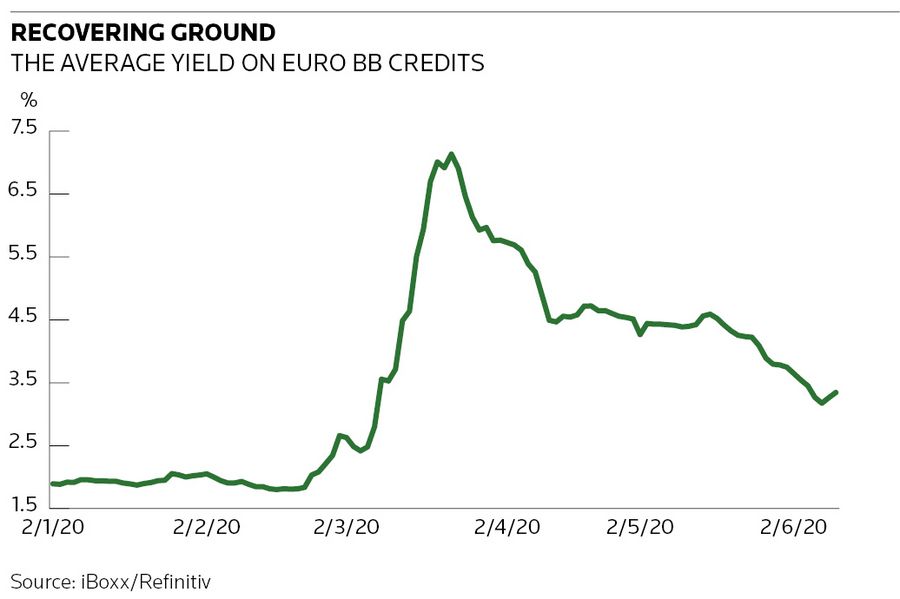

Average junk bond yields have recovered to 4.3%, down from a peak of 8.9% in March, according to Refinitiv data. Some analysts are cautiously optimistic about the outlook, thanks to supportive technicals.

"In high-yield, there's been no supply, because issuers haven't needed to come. But because of government support they've got liquidity anyway and that's reducing defaults," said Azhar Hussain, head of global credit at Royal London Asset Management.

"That creates an environment on the technical side that is very supportive. Defaults aren't going to be anything like what people thought they were going to be two months or even a month ago."

CAUTIONARY TALE

But while sectors such as high-yield and emerging markets play catch up, other areas were providing a cautionary tale.

On Monday, Additional Tier 1 transactions from Commerzbank and ABN AMRO demonstrated the strength of the primary market, with combined demand for the two trades peaking above €19.5bn.

But by mid-morning on Tuesday both deals were bid below par, at 99 and 98.60, respectively, setting a new tone, bankers said. By Friday morning they had fallen to 97 and 97.62 respectively, according to Refinitiv prices.

Still, demand for less straightforward deals did not disappear as on Wednesday BPER Banca became the first Italian lender outside the country's top tier to enter the market since the coronavirus outbreak.

And Nationwide Building Society took the AT1 revival to the sterling market, printing a £750m deal on more than £4.4bn of demand. It was the first sterling-denominated AT1 since November.

"It's amazing how far we've come and we really are getting very close [to pre-crisis spreads]," said a DCM banker. "The worry is whether we have, in the last three or four days, moved too far too fast?"

"The market needs to consolidate because you can't go 10bp tighter every day."

Additional reporting by Eleanor Duncan, Tom Revell, Ed Clark, Robert Hogg