Barclays avoided significant derivatives-related losses in the first quarter of 2020 through rejigging its derivatives exposures with telecommunications giant Verizon, one of its largest corporate swaps clients, according to sources familiar with the matter.

Those trades, some of which may have involved a circular movement of money between the two companies, could have saved the UK lender as much as US$100m, experts estimate.

Verizon took the unusual step of posting US$1.3bn of collateral against derivatives trades in the first quarter of the year, public filings show. The US company borrowed the same amount of money – US$1.3bn – from an asset-backed bank loan facility in March, in what experts say was probably a carefully coordinated set of transactions.

It is not clear which bank (or banks) lent the US$1.3bn to Verizon and there is no suggestion of wrongdoing by either Barclays or Verizon.

But banks in the past have lent money to companies to post collateral against, or restructure, swaps trades – a practice that regulations permit, but some supervisors appear to frown on.

“This practice is essentially motivated by an arbitrage,” the European Banking Authority stated in a 2015 paper. “The overall level of risk has not changed. However, the net level of capital [for the bank] has.”

Differences in the regulatory capital treatment of banks’ derivatives exposures compared with their loans can make such arrangements hugely beneficial for lenders, allowing them to reduce credit provisions and capital charges incurred on certain swaps trades.

“There is a potential regulatory arbitrage where the bank lends money to the corporate so as to restrike the derivatives or to post collateral,” said Jon Gregory, a senior adviser at consultancy Solum Financial. “Some banks will take the view the regulation permits this."

Spokespeople for Barclays and Verizon declined to comment.

QUESTION ANSWERED?

Barclays' reshuffling of its swaps exposure to Verizon goes some way to answering a question that had puzzled rival bankers: how did Barclays avoid sustaining derivatives-related losses in the first quarter at a time when most big banks reported hundreds of millions of dollars of writedowns associated with credit and funding charges?

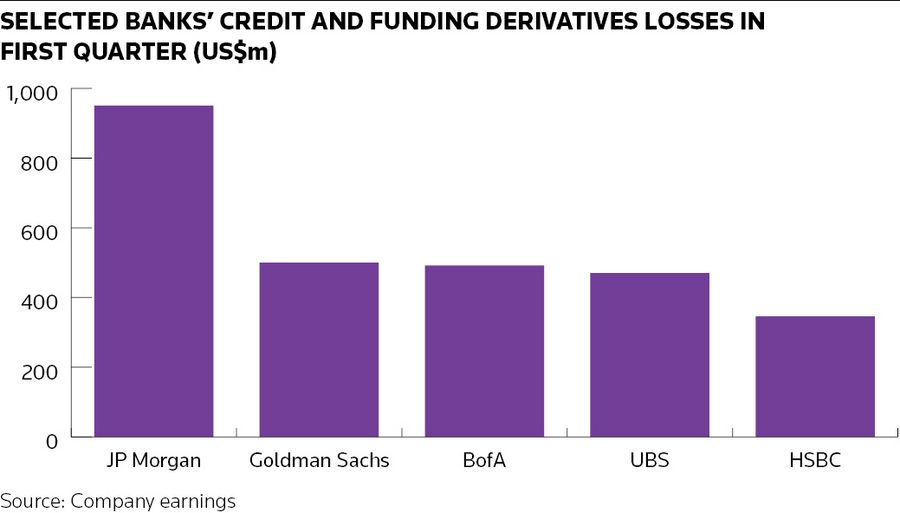

JP Morgan and Goldman Sachs recorded losses of US$951m and US$500m, respectively, in the first quarter. Barclays, by contrast, did not report any such hit.

That is despite the UK lender having a substantial presence in parts of derivatives markets where the lion’s share of these losses originated at other banks: those where corporate treasurers and other clients do not post margin when the trade moves against them.

MARGIN CALL

Not receiving margin hurts banks at times such as March’s slump in financial markets, when a collapse in interest rates altered the value of contracts struck at higher levels and company borrowing costs rocketed. That dynamic forced banks to lay aside more money to guard against a potential rise in client defaults as well as an increase in bank funding rates.

Restructuring trades or a client posting collateral can significantly reduce regulatory capital charges for the bank. The problem is most companies refuse to do so because of the large costs involved. To get around this, banks have in the past lent companies money to post margin against the swaps trades.

"This is an area in which banks could look to make capital savings," said George Garston, risk advisory manager at Deloitte.

"The loan could potentially attract lower capital requirements than the counterparty risk exposure on the derivatives depending on the maturity of the derivatives, the seniority of the loan, and whether the loan is secured by additional collateral," he said.

"From a risk perspective, however, it is more or less just shifting risk from one part of the balance sheet to another."

BIG USER

Verizon is a big user of derivatives to hedge risks associated with its business, with about US$20bn in different types of interest-rate swaps and US$23bn in cross-currency swaps, filings show.

The Verizon trades alone are unlikely to explain Barclays' lack of credit and funding-related derivatives losses in the first quarter. Industry executives estimate these could have totalled as much as US$400m without Barclays taking mitigating action. But they undoubtedly played a key role in that process given Verizon represents one of the largest exposures in Barclays' uncollateralised swaps book, sources say.

Public filings offer clues to how Barclays may have done that. Verizon settled US$1.5bn of interest-rate swaps in the first quarter and entered US$2.4bn in new trades.

But potentially of greater significance, experts say, is the US$1.3bn in collateral Verizon posted against derivatives trades at the end of March – by far the highest sum it has ever pledged. Since renegotiating its swap agreements in recent years, seemingly to reduce the likelihood of having to meet large margin calls, Verizon has not posted more than US$100m.

Meanwhile, Verizon borrowed US$1.3bn in March under an uncommitted asset-backed loan facility it has with several banks secured on customer mobile device payment plan agreements, having only just repaid US$1.3bn under that same facility in January.

LUMPY EXPOSURES

There would probably have been benefits for Verizon in agreeing to the trades, particularly if they freed up capacity for Barclays to offer derivatives at attractive prices in the future.

It is unclear whether Barclays managed to make similar arrangements with other important clients.

“These exposures are quite lumpy," said Solum's Gregory. “If a bank has an extremely large exposure to half a dozen corporates, which has just blown up because of the move in the market, then restructuring trades with just a small number of those clients could make a big impact."