Trading in ESG-friendly credit derivatives has got off to a slow start, with only a handful of contracts of the iTraxx MSCI ESG Screened Europe index changing hands since its launch in late June.

There is no volume or position data on the new index in the Depository Trust & Clearing Corp’s Trade Information Warehouse, a central repository that collects data on the credit-default swap market. That indicates there were fewer than 10 contracts outstanding across the entire market after the first two weeks of trading.

Funds focused on investing in companies that meet certain environmental, social and governance standards have grown markedly in recent years to almost US$790bn, according to Morningstar. Bond traders believe IHS Markit’s ESG-friendly CDS index, the first widely available sustainable CDS product, can serve as a useful tool for such investors.

But the muted take-up so far underlines the challenges facing new products in gaining traction – even in this increasingly popular corner of finance.

“The overall market interest has been lower than we thought it would be,” said Jasdeep Singh Aneja, head of European macro credit trading at Goldman Sachs. “From what we understand clients are keen to see liquidity develop before they commit to it."

Europe accounts for 80% of the assets in ESG funds globally, according to Morningstar, with about US$170bn of those focused on fixed income.

The iTraxx MSCI ESG Screened Europe index began trading on June 22 after its planned launch date in March was delayed amid wider market turmoil. It is an adapted version of the iTraxx Europe Main index – the CDS benchmark for European investment-grade corporate debt – referencing the CDS of 81 of the 125 companies in that index.

The original iTraxx Main index is one of the most frequently traded products in credit markets, with average weekly volumes of US$40bn in the first half of the year. By contrast, only about US$30m to US$50m of the ESG version of the index had traded about 10 days after its launch, according to one source.

Six banks are currently quoting prices: Bank of America, Barclays, BNP Paribas, Deutsche Bank, Goldman Sachs and JP Morgan. Citigroup and Credit Suisse are applying to become market-makers, while Morgan Stanley is supportive of the initiative and is monitoring it closely, according to sources familiar with the matter.

“We are confident activity could grow – it's extremely early days,” said Olivier Renart, global head of credit trading at BNP Paribas, who said his firm had done a few client trades.

"The main interest is coming from institutional clients with ESG mandates. I believe they will use it just as they use normal CDS indices: to hedge, to quickly ramp up risk when they have inflows or to manage leverage."

SELECTION PROCESS

There are three separate screens used to exclude companies from the original iTraxx Europe Main based on MSCI’s research to create the new ESG index. The first is to remove companies prominent in certain sectors, such as tobacco and armaments. Others are more subjective, such as using MSCI’s ratings to judge how ESG-friendly a company is.

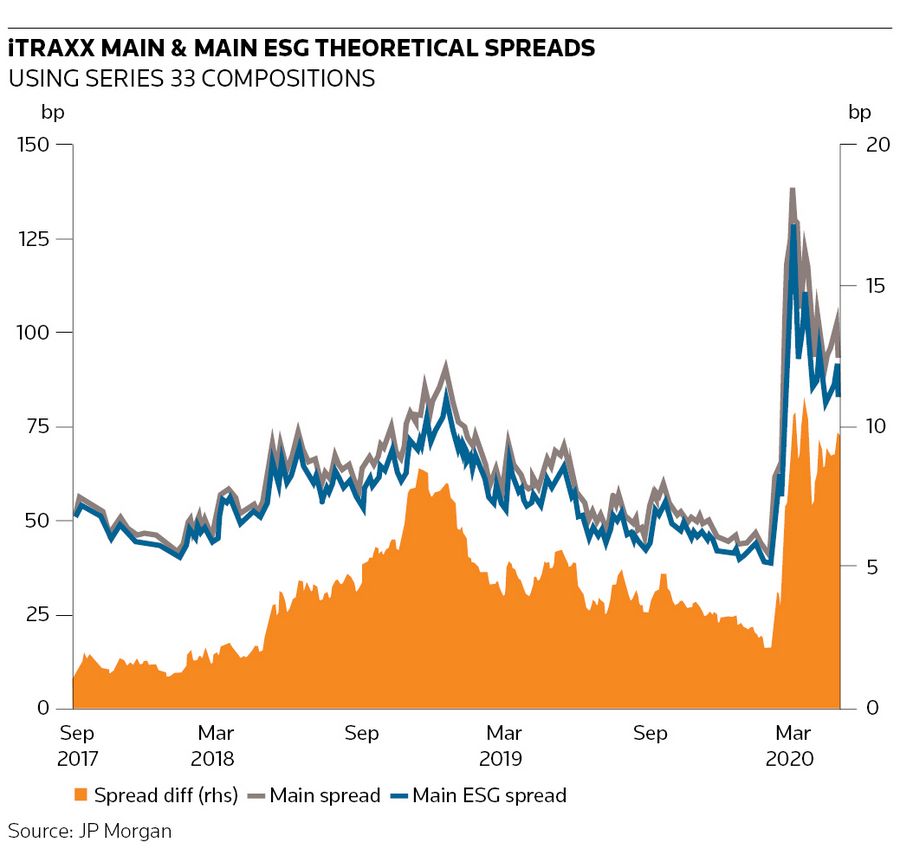

Credit spreads on the ESG index trades about 10bp tighter than the Main index, outperforming in particular during times of market stress, according to analysis from JP Morgan's credit research.

Overall, the ESG index has a higher exposure to telecoms companies and a lower one to banks than its forebear. But there are notable differences even within sectors: BBVA, BMW and BT all make the ESG cut; Banco Santander, Daimler and Deutsche Telekom don’t.

This selection process is one potential stumbling block for investors given many have their own ESG selection criteria.

“It is a challenge. There is not one universally accepted gold standard of what an ESG methodology should look like. It varies from investor to investor,” said Wolfgang Bauer, a fund manager at M&G Investments.

CHICKEN AND EGG

There is also the chicken-and-egg problem of building liquidity in an index in which investors may want to see a critical mass of activity before committing. Banks have quoted the ESG index at bid-offer spreads of 3bp to 3.5bp compared to usually below 1bp for iTraxx Main.

Bauer said that the lower level of liquidity of the ESG index – something that is "pretty normal in the beginning" – along with the lack of a live track record could act as deterrents for investors initially. But those issues should fade in time.

“The demand for ESG strategies in Europe is growing, so I would expect the importance of iTraxx ESG to increase as well,” he said.

Traders point to some encouraging signs such as notable interest from hedge funds, which may solve a potential issue arising from a general aversion among investors to short the ESG index.

The lack of short interest is causing the ESG index to look unusually expensive versus the level implied by the spreads of all the individual company CDS. Traders say that phenomenon – known as the “skew” – should tempt hedge funds to put on an arbitrage trade of shorting the index and going long the single-name CDS, as well as potentially shorting the ESG index versus the Main index.

“You have various forces to ensure some balance in terms of the direction of interest,” said Renart.

Overall, banks appear confident the index will take off, even if it takes some time.

“ESG is just getting started," said Singh Aneja at Goldman Sachs. "This is a theme that is going to come more and more to the forefront and having a liquid index will be a valuable tool."