Banks are scrambling to assess the implications of a US law that would impose sanctions on parties closely involved with the imposition of China's national security legislation in Hong Kong.

The Hong Kong Autonomy Act was passed by Congress on July 2 and may be signed into law by President Donald Trump this week. It is widely expected to target a limited number of senior government officials in China and Hong Kong, but could be used to apply wide-ranging sanctions and penalties.

Bankers and lawyers were busy evaluating possible scenarios last week, including the worst case in which they would be forced to sever ties with numerous clients, three sources familiar with the deliberations told IFR. Several banks are drawing up contingency plans, which include reviewing existing client relationships to determine how difficult it would be to sever those and what impact it would have on their bottom lines.

"When examining how their operations might be impacted, financial institutions should take into consideration the broadest possible range of potential sanctions," said Nick Turner, a lawyer specialising in sanctions and anti-money laundering at Steptoe and Johnson in Hong Kong.

"The way the law is written, the State and Treasury Departments do have discretion in how they apply the sanctions, the specific transactions that might be covered by them, whether there might be thresholds, etc.”

EXPANSIVE INTERPRETATION

The HKAA states that, within 90 days of the bill being enacted, the Secretary of State must draw up a list of foreign entities and individuals that have contributed to what the US deems the erosion of Hong Kong's autonomy.

Between 30 and 60 days after the initial report is delivered to Congress, the Treasury Secretary has to draw up a similar list of foreign financial institutions that continue to carry out any "significant transaction" with those singled out in the first report.

The potential sanctions for those in the first report range from freezing assets to revoking visas, while those for foreign financial institutions are more extensive. They include a ban on carrying out foreign exchange transactions in the US and acting as primary dealers in US government debt. US banks, though only mentioned once explicitly in the act regarding loans to sanctioned foreign financial institutions, would be barred from dealing with any sanctioned individuals or entities.

Several sources expressed concern that banks applying US sanctions could also breach Hong Kong's new national security legislation, which refers to sanctions in a clause outlawing collusion with foreign forces against China or Hong Kong.

Banks might effectively be forced to choose between obeying the US law on sanctioned individuals and Hong Kong law on not cooperating with US sanctions. As the Hong Kong law has an extra-territorial aspect, it will only partially relieve the dilemma if decisions are made by those working for banks outside Hong Kong or China.

Bankers said it was far from fanciful to suggest that banks might have to choose between being barred from the US dollar system, on the one hand, or having their licence to operate in Hong Kong revoked, on the other.

"Banks and other financial institutions are understandably concerned about whether they will be able to comply with the foreign sanctions that apply to them," said Turner.

"As with the US sanctions, everybody is waiting for clarification from the relevant Chinese and Hong Kong enforcement authorities to understand whether complying with those sanctions risks violating the national security law.”

The impact of the sanctions will likely hinge on how narrow a view the US government takes of the persons responsible for what it construes as undermining Hong Kong's autonomy and what constitutes a "significant transaction" carried out by any foreign banks they deal with.

Market observers expressed concerns about what the implications would be if the government took a more expansive interpretation of the law: for example, if the first list were to include all state-owned enterprises or any company with a Chinese Communist Party official as a board member, although most think that this is unlikely.

"One example that would be fairly remote is taking action against an entity merely because a designated person just sits on its board," said Tamer Soliman, global head of law firm Mayer Brown's export control and sanctions practice.

"The US will want to be selective and thoughtful about the deployment of this law. There’s going to be thought given about what the consequences of a designation are, whether the designation is proportionate to the conduct, and what signal it sends."

CHINESE RETALIATION

One major concern is how China will retaliate, especially given that the provision on foreign financial institutions is most likely to impact some of the country's largest banks.

Reuters reported last Thursday that Chinese state lenders, including Bank of China and Industrial and Commercial Bank of China are drawing up contingency plans in case they lose access to US dollar settlements, underscoring the concern in Beijing.

On the other hand, China has continued to open up its financial markets to foreign firms despite ongoing trade tensions with the US and several banks IFR spoke with said they do not anticipate any backsliding, although Beijing has in the past taken a firm stance on particular issues.

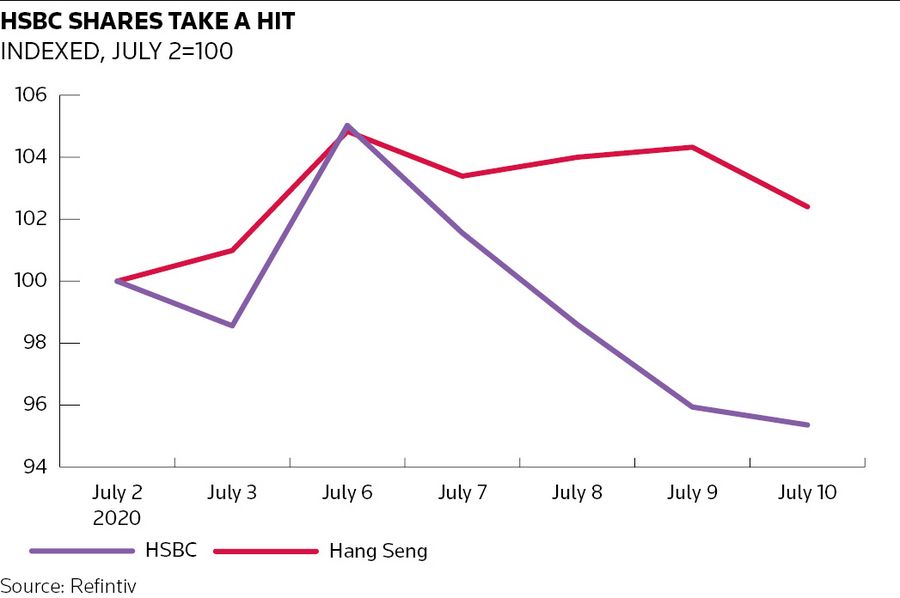

Last year, HSBC was left off an expanded panel of banks to determine China's new benchmark loan prime rate in an apparent snub for its role in the US investigation into Chinese telecoms firm Huawei.

Last month, both HSBC and Standard Chartered issued statements supporting the imposition of China's new security law in Hong Kong in response to suspected pressure from Beijing.

The two Anglo-Asian lenders are seen as most exposed to regulatory action given the size of their businesses in Hong Kong. Other sources pointed to Credit Suisse and UBS as facing similar problems because of the number of wealthy Chinese they bank.

The Swiss banks would face a miserable if relatively straightforward decision if they were forced to choose between their Hong Kong/China operations and unrestricted access to the US dollar system. But it would be a much more unpleasant dilemma for HSBC – one of the world's largest clearers of US dollars – and to a slightly lesser extent StanChart.

HSBC made US$33.2bn in profits in Hong Kong in the last three years (two-thirds of its profits). StanChart made US$3.3bn in Hong Kong in the last two years, or 42% of its profits.

HSBC insiders point out that that the damage to the global banking system (including to US banks), to Hong Kong, to the UK (HSBC and StanChart are headquartered in – and pay taxes – in London) and to US-China relations would be so severe that that maximalist approach from both sides is unlikely. But they acknowledge that it is far from impossible – especially if relations between the US and China take a further turn for the worse.