Sharp market swings and rising bankruptcies have failed to dampen activity in a complex breed of credit derivatives that enable investors to take leveraged bets on company defaults.

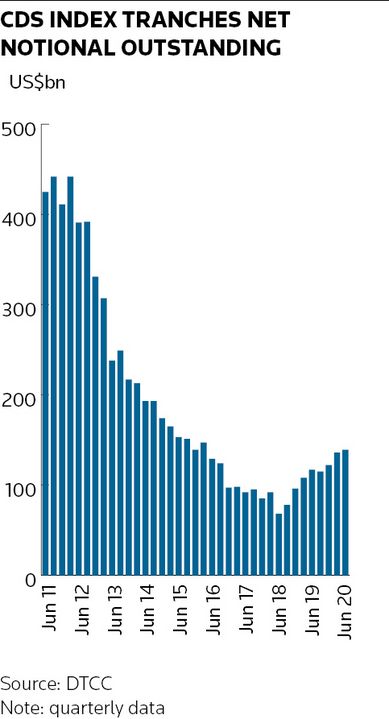

The net size of the market for tranches of synthetic collateralised debt obligations linked to credit indices has increased to a four-year high of US$141bn, according to the DTCC. That comes amid a flurry of trading, with volumes of tranched credit-default swap indices rising 45% annually in the first half of the year to US$96bn, according to IHS Markit.

Credit markets nose-dived in March amid fears that the spread of the novel coronavirus would trigger a wave of corporate bankruptcies. Those moves reportedly inflicted heavy losses on some firms prominent in this complex corner of finance, including hedge fund CQS.

But that challenging backdrop, which has improved notably since central banks intervened to prop up corporate bond markets, has done little to dent demand for this controversial breed of structured credit investment.

"We've seen people re-engage with the market and we're seeing new people looking to get involved," said Olivier Renart, global head of credit trading at BNP Paribas.

"When you have a bit of spread and a clear dispersion between sectors – the haves and the have-nots of the crisis – tranches become an interesting product."

DARKENING OUTLOOK

Trading in synthetic CDOs plummeted after the 2008 financial crisis, not least because of the role some types of this product played in spreading sub-prime mortgage losses throughout the system.

But activity has surged in recent years in synthetic CDOs that carve up pools of credit-default swaps linked to corporate debt, as low interest rates have encouraged investors to consider more complex investments.

Investors in the riskiest tranches of these structures earn the highest returns, but are on the hook first for losses resulting from any companies in the CDS portfolio going bust.

When a darkening default outlook in March wreaked havoc in credit markets, those that had effectively sold insurance against rising defaults suffered heavy losses.

Fitch said in a July report that 28 non-financial companies it rates defaulted in the first five months of the year. That is already more than 2019's total and puts defaults on track to surpass the yearly record set following the 2008 financial crisis.

"During the peak of the [recent] crisis there was a lot of leverage that came into question across different pockets of the market,” said Jasdeep Singh Aneja, head of European macro credit trading at Goldman Sachs.

“In Europe, we’ve seen most of the stress go away given the rally – we didn’t really see any defaults. We saw more stress in US high-yield, where there were a lot of defaults that actually had an erosion of capital, some even after the rally."

STRONG RALLY

The US Federal Reserve’s unprecedented commitment in March to buy corporate debt – along with increases in similar schemes from the European Central Bank and the Bank of England – underpinned credit markets and helped fuel a strong rally. New debt issuance surged in the US along with corporate bond trading volumes.

Trading in the more complex CDS tranche market also rocketed in the first half of the year, particularly at the height of the turmoil. Volumes in CDS index tranches increased 93% to US$71bn in the first quarter compared with the same period a year ago, according to IHS Markit.

Over US$16bn of tranches linked to an old version of the iTraxx Europe Main index traded in one week alone at the height of the turmoil, according to the DTCC, suggesting a significant reshuffling or closing out of positions.

The CDS index tranche market has continued to expand in the second quarter, albeit at a slower pace.

Kokou Agbo-Bloua, head of flow strategy and solutions at Societe Generale, said there is a divergence of views among investors over defaults, with central bank action encouraging some to take more risk, while others are concerned about a second wave of Covid-19 inflicting more damage on the economy.

“Investors are favouring shorter-term products, as well as investment-grade over high-yield,” he said. “Clearly, people are looking more for super-senior [exposure] and less at the riskier tranches.”