Some dedicated green bond funds may expand their mandates to invest in increasingly popular sustainability-linked bonds as the European Central Bank’s decision last week to accept some SLBs as eligible assets for its bond purchase programme raises the prospect of a boom in issuance.

SLBs tie companies’ funding costs to their achievement of ESG targets and are being hailed as a more effective weapon to decarbonise "brown" companies than green bonds, which tend to reward already virtuous firms. Many think that the market for SLBs will grow to dwarf that for traditional green bonds.

Some green bond funds, particularly "dark green" investors who prefer deals tied to specific projects, have been unconvinced by SLBs, which have a more general use of proceeds, but may now be more amenable to buying the instruments to broaden their pool of securities and assets under management.

"Green bond fund managers are adapting. Some are trying to change mandates. That's just the way the market is developing," said Frazer Ross, head of investment-grade debt syndicate for EMEA at Deutsche Bank.

Arthur Krebbers, head of sustainable finance for corporates at NatWest Markets, said: “I think it is likely that many green bond-focused funds will expand their mandates.”

And it is not just banks pushing that line. Alastair Sewell, regional head of Fitch's fund and asset manager group for EMEA and APAC, is seeing the same trend.

"We can certainly see an adaptation of the green bond fund universe to increase exposure to sustainability-linked bonds," he said.

Many of the larger global fund managers – including Lombard Odier Investment Managers, one of the top 25 green bond investors with more than US$1bn in green AUM – are already buying both instruments.

"We can invest in anything in the sustainability sphere. Most pension funds and asset managers have a great deal of flexibility in this space,” said Ashton Parker, head of credit research and a senior portfolio manager at Lombard Odier.

Not everyone is buying into the current excitement around SLBs, however.

Dutch manager NN Investment Partners can buy such bonds but chooses not to.

“We have no plans to do that soon. I feel there’s a very strong push from a lot of banks to make [SLBs] a successful product, but if you go to asset managers, there’s a lot more question marks and uncertainty,” said Bram Bos, lead portfolio manager, green bonds at NN IP.

How that debate plays out remains to be seen. Ultimately, it will be end-investors’ call how many green bond funds are able to stick to dark green purity or move into broader sustainability or sustainable finance assets.

GREEN GROWTH

Dedicated green fund assets under management reached €13.8bn at the end of the first half of the year, Fitch estimates, and grew by 30% in the same period (compared with 0.6% growth in total bond funds globally, albeit from a smaller base).

Green bond fund AUM are just 0.14% of total bond fund AUM, but the number of green bond funds is increasing rapidly, with 61 green funds globally at the end of the first half, Fitch says, many of which have converted from conventional bond funds.

Strikingly, green bond funds, most of which are based in Europe, currently only hold 2% of total outstanding green bonds.

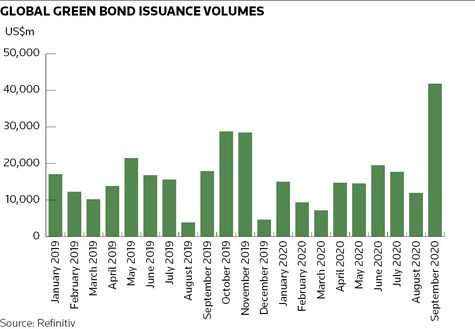

GREEN SEPTEMBER

According to Refinitiv data, September has already seen US$43bn of green bond issuance, comfortably outstripping the previous record month of US$29bn in October 2019. Green bond issuance for the year to-date is US$153bn, meaning 2020 is on track to exceed the US$191bn seen last year.

The EU's pledge to issue up to 30% of its €750bn Next Generation recovery package in green bonds all but guarantees that 2021 will be another record year for green bond issuance and that there will be more than enough supply for pure green investors – and everyone else.