A sharp increase in margin calls during this year’s market turmoil has triggered a fierce debate between banks and derivatives clearinghouses over the extent to which the clearing industry needs to reform and standardise margining practices to avoid destabilising the wider financial system in future crises.

Central counterparties weathered their sternest test since the great financial crisis of 2008 after markets nosedived in March, demonstrating that a crucial pillar in the regulatory framework developed in response to that time was up to the task.

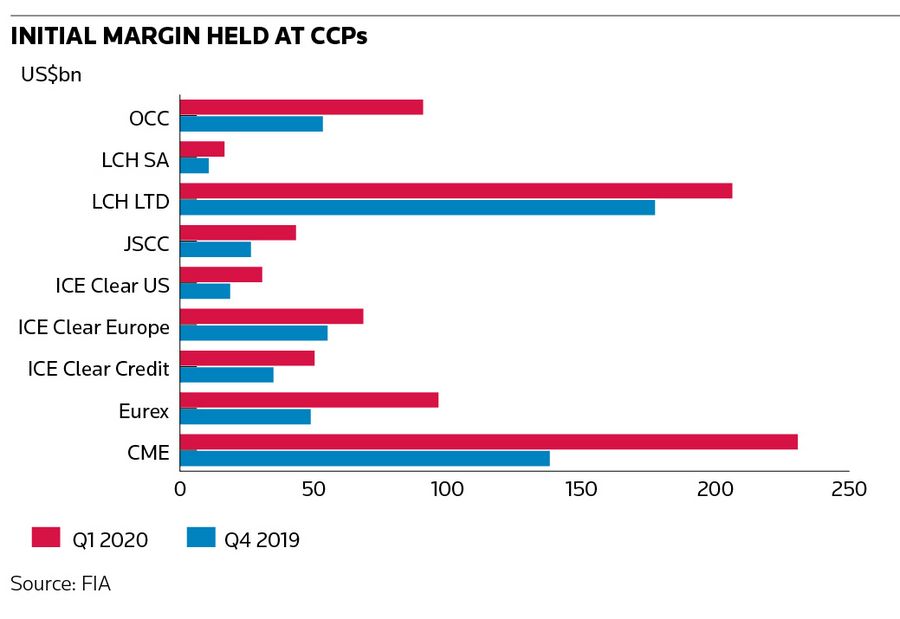

But a recent paper from the the Futures Industry Association, a trade body, said a nearly 50% rise in initial margin levels at derivatives clearinghouses in the first quarter – to US$834bn – contributed to “an abrupt and disorderly ‘dash for cash’”, which ultimately abated only after central banks stepped in to calm markets.

Clearinghouses mounted a robust defence of their actions during the crisis. A series of unprecedented moves across markets – along with an increase in trading positions – warranted higher initial margin, they say, while highlighting their efforts to minimise market disruption.

Even so, at least one CCP has revised its margin methodologies in the wake of this year’s events and others acknowledge the pressure to bring greater harmonisation across the industry.

“Everything flowed as it was supposed to flow despite stresses in the system from significant margin calls. The margin moves were very large and definitely contributed to market illiquidity," said Nick Rustad, global head of derivatives clearing at JP Morgan and chairman of the FIA. "We would like greater transparency around why margin changes and how likely that will occur under different scenarios."

Clearinghouses act as middlemen in derivatives trades, preventing losses from cascading through the system if one of the counterparties defaults. Clearing has grown in importance since the 2008 financial crisis as regulators have forced great swathes of the over-the-counter derivatives market through CCPs.

Executives across the financial industry agree the system held up well during the March market turmoil as the Covid-19 pandemic spread. But banks that funnel trillions of dollars-worth of derivatives trades through CCPs, along with regulators, have said this overall success masked some underlying issues.

System strain

The scale and speed of some initial margin calls in the listed derivatives space was a principal point of concern – something banks argue can cause considerable strain on the financial system at an already tumultuous time.

The amount of client margin held in clearing accounts in the US rose by US$136bn in March – a jump over six times larger than any previous single-month increase on record, the FIA said. Initial margin requirements on several equity index futures rose 90% or more over the first quarter, while margin on 10-year Treasury and Bund futures, the most important benchmarks for long-term US and euro area interest rates, increased 61% and 92% respectively.

“During the crisis, we saw procyclicality in margin calls from CCPs, whether in OTC or in futures markets, that needs to be addressed ,” said Christopher Perkins, co-head of futures and OTC Clearing at Citigroup.

Clearinghouses say two factors drove the rise in initial margin: increases in client positioning and – perhaps most significantly – extraordinary moves across financial markets in the first few months of the year. CBOE’s Volatility Index – the VIX, tracking S&P 500 volatility – rose more than six-fold, Treasury yields whipsawed and oil futures contracts plunged below zero.

“We do have anti-procyclical measures in our margin models, but because of the extreme shift in the volatility regime, we did respond,” said Lee Betsill, chief risk officer at CME Clearing. “Seven of the top 10 largest variation margin cycles since the 2008 crisis happened in March. That underlines the unprecedented nature of the markets that we were seeing.”

Margin call

Executives at clearinghouses, including CME, Eurex, LCH and OCC note initial margin levels increased gradually to minimise stress on the system.

“Our margins started increasing in February incrementally,” said Dale Michaels, chief financial risk officer at OCC. “By the middle of March our margins were already higher so there wasn’t a liquidity crunch – we were much more protected.”

Sunil Cutinho, president of CME Clearing, said that the changes in margin at his firm were very modest by comparison to the scale of the market moves. "Our margin models are transparent: we talk to our members about what drives them. We also give 24 hours' notice of changes in margin. We give them predictably," he said.

Industry executives also note that initial margin increases were generally managed well in the OTC derivatives space. “We received feedback that OTC swaps handled the volatility well,” said Susi de Verdelon, head of SwapClear and listed rates at LCH.

Even so, at least one clearinghouse has reviewed its margining practices following this year’s events, with the Japan Securities Clearing Corporation revising its margin calculation methodology for listed derivatives in July. “JSCC recognises the necessity to repress procyclicality and has implemented relevant measures,” a spokesperson said.

And some prominent clearers acknowledge the need for greater standardisation across the industry.

“We understand some of the criticism, especially that CCPs reacted very differently during the market crisis, with some CCPs doubling margin levels from one day to another,” said Dmitrij Senko, chief risk officer at Eurex. “We have been advocating greater harmonisation around margin levels and transparency for many years. Hopefully these events will help to get closer to this.”