Wakako Sato, Refinitiv LPC: As a frontrunner in the market that completed the first deal, I think you have done a great job. Speaking of being the first, this summer Mr Ito of Marubeni also procured Japan’s first green loan for hydroelectric power generation. Could you tell us about the background to this project, and what were the strengths and challenges?

Naoki Ito, Marubeni: To tell you a bit about the background of Tottori hydroelectric power generation, which we call Tottori PFI, local governments in each prefecture in Japan have corporate bureaus that have been engaged in the hydroelectric power generation businesses. Therefore, each prefecture has a history of generating hydroelectric power long before commercial electric power companies entered the business. Some of these hydroelectric power generation facilities have been there for more than 50 years but they have not been effectively utilised. Against this background, Tottori prefecture listed four of the hydroelectric power generation facilities in an auction for upgrades and replacement, and transfer of operating rights for 20 years. The Tottori PFI is the first concession-type of hydroelectric power generation business in Japan.

Since it is a PFI deal, it was not a matter of simply determining the winning bidder in terms of price and quantity; it was a comprehensive evaluation. In particular, with regard to renewable energy, coexistence with the local community and contribution to the community are major themes regardless of the open call for participants. Also in the case of Tottori, it was clearly stated that contribution to the community and revitalisation of the community would be the key for the evaluation. We applied for this project forming a consortium with Mibugawa Electric Power, Chubu Electric Power, and local companies, but the difficulty was differentiating ourselves from others.

Thanks to our financial adviser Sumitomo Mitsui Banking Corp, we learned that the green loan is a product that can include renewable energy. Even in Tottori prefecture, the momentum of SDGs [Sustainable Development Goals] is increasing, and a place called Nichinan town in Tottori where the power plant was located was selected as an SDG future city. While such momentum is increasing, SMBC recommended that we use a green loan for this finance, which was incorporated into the content of the open call for participants.

We successfully received an order for the project as a consortium. On top of being a public offering project of the prefecture, the first hydropower concession in Japan, we were under the influence of coronavirus pandemic, and the schedule for closing the finance was very tight. It was particularly challenging as we promised to use green finance in the public offering. But we managed to close all contracts, conclude financial documents, and get a green loan certification with the cooperation of SMBC. We managed to close it, and construction is underway.

It was the first time for us to use the green loan and use it for a project, so it was honestly difficult to compare what was difficult, but we requested to push it through in a short period of time. The people of the prefecture who selected us have highly evaluated us. Even from this perspective of finance, they were very happy that we came up with the first green and sustainable deal for such a project.

This was the background of the Tottori hydropower deal, and as our unit is developing and promoting hydropower, offshore wind power, and biomass as renewable energy, we think this type of public offering will increase. Again, coexistence with the community is key, and regardless of whether it becomes a requirement or not, green loans will also be key. I think that it will be difficult to participate in the open call without green loans.

Wakako Sato, Refinitiv LPC: What is the appeal, significance and challenges of ESG finance for lenders? As discussed earlier, loans can be more attractive to borrowers than bonds, but is it the same for lenders?

Yasushi Goto, Mizuho Bank: From the perspective of lenders, financial institutions, the idea of emphasising sustainability in lending is spreading. Mr Hamano said that the movements on the lender side are very important, but the number of financial institutions making SDG declarations has increased significantly in the last few years, and last year only two of the 47 prefectures were missing banks that made SDG declarations.

In addition, the financial environment will change drastically in response to growing awareness of sustainability, so investors with a high degree of awareness of the significance of ESG/SDGs are becoming more important. Therefore, I think tendency of investors choosing sustainability finance will be more significant.

The management policies of financial institutions are formulated in consideration of ESG and SDG factors. On the other hand, to what extent management policy has permeated the field side in finance, the actual operation emphasises interest rates in a low interest rate environment, and the priority of sustainability is subordinated to economic rationality. We recognise that full-scale ESG/SDG initiatives are at the stage of shifting to financial operations. As an arranger, Mizuho Bank has been focusing on ESG/SDG finance for the past few years and has been collaborating with investors in syndicated loans. The number of enquiries regarding sustainability finance has increased since last year, and we believe that the market will develop.

From a borrower’s perspective, I feel that there is an increasing number of cases in which proposals for procurement based on the company’s “sustainability story” are being requested.

Mizuho recognises that it is important for us to consider the materiality and sustainability story of the company, run in parallel with the company to achieve it, and support sustainability management as a group. We would like to contribute to the realisation of a sustainable society and the development of ESG-related finance markets by providing finance that truly meets the needs of the company and supporting the company’s overall efforts.

Tadahiro Kaneko, SMBC: Regarding the attractiveness to lenders, we are certainly aware that it is led by capital markets. I think the biggest driver is the United Nations PRI. For institutional investors, as one of the requirements of PRI, more than half of the balance must be covered by ESG investment, so I think this has driven things to a great extent.

In the world of indirect financing or among commercial banks, the United Nations Principles of Responsible Banking, which is the bank version of the PRI, started in September last year and megabanks including ourselves signed up to it. There are also similar requirements such as sustainable finance lending balance that have to be disclosed after a certain number of years. I think banks, despite being indirect financiers, are getting into a momentum where they will have to set their goals and hit the accelerator.

SMBC announced in April a 10-year sustainability-related plan called GREEN×GLOBE 2030. One of the KPIs is that we have set a target of ¥10trn in green finance in the 10 years up to 2030. All global banks are announcing the amount of this kind of sustainable finance and these target values, and when you look at foreign banks, they are taking a position where they are raising their original goals by evaluating the actual situation. In this respect, the bond market has recently seen momentum in demand from institutional investors. Even among banks providing indirect finance, KPIs will increase the incentive to preferentially allocate funds to such green finance or to sustainable finance.

With a mechanism like this, we feel that we should provide indirect finance based on the customer’s ESG efforts, sustainability improvement efforts, and I think that is the greatest role for banks providing ESG finance. In terms of the micro world, the phenomenon that we see at the moment is that young employees in front offices who participate in internal ESG and sustainability seminars and workshops have a strong desire and motivation for this kind of business.

Tomoki Muto, MUFG: I was very interested in hearing about the points that Mr Hamano mentioned. I was very impressed by the fact that the people in charge of finance carefully considered and created the message from top management in the first place. The appeal of ESG finance for lenders is that you can gain customers’ trust by discussing their vision, values, and management strategy. On the other hand, after all, how much the top management is engaged in ESG and how much the people in charge are involved depends on the companies. Some companies like NYK are progressive, while the others are not. We are trying to fill the gaps and differences in that area. It would be a great pleasure as a financial institution if we can connect from the management level to the person in charge at the customer’s company, and if we may, we can support by discussing the importance of ESG and engagement with stakeholders over the long term. As Mr Kaneko said, many of the people who work for financial institutions have the aim of contributing to society, and I think bankers including young people find it very rewarding.

Given that financial institutions have various perspectives such as internal ratings, profitability, and loan collection standards when lending, I think that the movement to reflect corporate ESG initiatives will increase. Furthermore, where financial regulators are involved, for example, there are capital adequacy requirements for financial regulation. I am hearing that the possibility of adjusting capital requirements for green and ESG-related assets is being discussed, especially in Europe. As such efforts progress, the capital adequacy requirements for loans provided to customers will be adjusted according to the degree of ESG financing efforts, so I think that the movement of financial institutions will accelerate.

What we are concerned about is whether we are providing SLLs that truly contribute to the sustainability of our customers, while ESG and sustainability have been so popular. In recent years, financial institutions are increasingly setting goals for their own sustainability. We have issued a sustainability report so it would be great if you can have a look, but I wonder if the purpose is to increase the loan amount to meet such sustainability goals. I think we have to keep in mind whether we can truly contribute to our customers’ transition and sustainability management. For example, ESG finance efforts have been criticised for “greenwashing” and “sustainability-washing”, where the increase in finance simply has a product named sustainability-linked loan and does not involve substantial content. I think financial institutions must be careful about actions that are perceived as such.

Wakako Sato, Refinitiv LPC: As we heard from Mr Muto, the question is whether this kind of finance really is beneficial for the borrower or if pricing is the only appeal. With that in mind, what do you think are the issues Japan’s ESG market needs to overcome for further development?

Atsuko Kajiwara, JCR: Depending on the company, some work on ESG finance has been quickly driven by strong initiative from top management, while there are some whose finance and CSR departments have their first discussions upon issuing green bonds.

However, customers that didn’t have a sustainability strategy put together a very good integrated report the following year they experienced ESG finance, or in some cases, they organise and maintain their departments well and make great progress the year after. I think that it’s loans, rather than bonds that have made this possible.

SLLs are still in their infancy, and people tend to think that the first company that comes out must be the top level or must be number one in the industry. But in reality, when you work on the SLL individually, they do not have to have perfect sustainability strategies yet, but banks should work together to improve, for example, by having a regular and stable relationship through a commitment line. It would be interesting if the company evolves significantly in the next year by doing so. I think that showcases the power of banks. It would be interesting to have young people who are interested in ESG communicate with companies and work together.

A wide variety of financial products such as green bonds, green loans, and SLLs have come out one after another in the last few years, and we, as an evaluation company, find it hard to follow. It takes more than 30 minutes to explain what these products are; companies are also very confused. Before showing this variety of finance tools, you must understand what the company needs first, and whether it’s summarised in a sustainability strategy. In the next step, you must understand whether companies have integrated sustainability strategies into their medium to long-term management plans.

At this point, improving corporate values and sustainability are exactly linked. For those in the process of getting there it is now very important to finance a green asset for a certain company and doing so will lead to the next business opportunity and the company can build a sustainability strategy from there. There are some companies that want to talk about policy-based stories rather than specific use of funds because they have firmly established strategies. In this case, you should propose finance with unspecified use of funds. You should make an effort to raise needs in dialogue with companies and if you can do that, it will be a good relationship with each other in a win-win situation.

Wakako Sato, Refinitiv LPC: Mr Hamano of NYK, what do you expect from the financial institutions as a borrower for further development of the ESG loan market?

Yoshiaki Hamano, NYK Line: Our president emphasises the promotion of ESG management both internally and externally, and we would be really grateful if banks could support us in terms of finance. It is easy to understand a green loan restricts use of funds for green investment targets, or an SLL does not restrict uses of funds and terms are linked to KPIs. But I think that the main job of our financing department is to procure the cheapest possible funds in a stable manner. I’m a little confused when the company sets a target for the ESG finance ratio and makes efforts to increase the balance, influenced by the company promoting ESG management and making a lot of ESG investments. I wonder if there is any incentive for us as a fundraising department to compromise and increase ESG finance. I understand the PR effect, but it would be very helpful if financial institutions could give meaning to other things or think together.

Wakako Sato, Refinitiv LPC: Mr Ito of Marubeni, what do you expect from financial institutions?

Naoki Ito, Marubeni: Within Marubeni Group, how much green funds we can raise for many renewable energy projects available in the market is important to my development unit and from the perspectives of the deal sponsor, the local government that manages the business and the lenders. I feel that green loans and related loans will gradually become a must.

It’s not just that the number of projects is increasing year by year, but also the scale of each project is becoming very large. I’m concerned how much liquidity can be secured. I think that it is a very good thing that the loan market develops accordingly.

We had a little trouble recently because it was the first time for us. We had to follow various procedures for the accreditation body. Although it was unavoidable, we were discouraged from a borrower’s selfish point of view as we had to prepare another chunk of a report while working on a huge amount of documents in project finance near the closing time. I hope there will be a way to simplify the procedures in some way.

As ESG loans evolve, I expect that there will be differentiation in various terms of conditions, like better terms that are offered if certain certifications are obtained. I think this would help expand the market quickly.

Wakako Sato, Refinitiv LPC: Could you please explain to us what kind of things you can do as an arranger in response to Mr Hamano and Mr Ito?

Tomoki Muto, MUFG: From the perspective of how to make the introduction of ESG finance meaningful, it doesn’t apply to companies that are making progress in sustainability, such as NYK and Marubeni, but the impact will be bigger for companies that are not making progress when ESG finance becomes more widespread. Some customers are already saying, for example, that companies with assets that emit a lot of carbon dioxide will have trouble raising funds either directly or indirectly from banks as the ESG market matures. I hear some of them feel a sense of crisis. How to evaluate sustainability in management is what we must tackle as a bank in the future.

As Ms Kajiwara said, it will be important that the customer and the financial institution work together to think about how to raise funds that can contribute to the sustainability management of the customer, and how to achieve that KPI. It will be important to work together to improve corporate value by expanding the scope. From the perspective of so-called financial inclusion, there is a concern that some customers may be left behind. Not all companies are engaged in green business, and I think we must consider how to provide financial services to the rest so that those companies are not left behind.

Wakako Sato, Refinitiv LPC: How much growth do you expect in the ESG loan market? What is the outlook of the market?

Yasushi Goto, Mizuho Bank: It is far from a mature market, but according to our investor survey, 10 companies said that they have a track record in 2018 and the number increased to 30 in 2019. As you can see, with the track record of more than 60 companies, the borrower base is expanding. However, economic rationality is very important. As you pointed out, we are striving to develop the ESG/SDG market while chasing economic rationality.

Tadahiro Kaneko, SMBC: I think it was about a year ago, but according to an analyst report from a securities company, global climate change-related investment needs alone was estimated to be worth US$1trn. The estimation is based on the UN Climate Change Panel, the IPCC analysis report, etc., but I think that financing needs through indirect finance will naturally emerge among such climate change-related investment needs. A large amount of investment needs is embodied in the category of climate variability alone. In addition, various aspects such as the circular economy and the social part will emerge, and ESG-related finance needs will grow significantly. I’m wondering if it will come. It’s a phase that has just begun and the potential is very large.

Tomoki Muto, MUFG: From the data provided, I think that green and ESG bonds are about 10% of the overall bond market, but green and ESG loans are still about 1% of the overall loan market. ESG finance will definitely continue to grow and transition finance will expand. Currently, the guidelines are being discussed, and it’s a-chicken-or-egg scenario, but there is no doubt that the market will grow after the guidelines are established.

It is easy to compare Japan with Europe and the United States, but as Ms Kajiwara said, pursuing a financial form featuring Japan’s characteristics will contribute to sustainability in Japan. We would like to extend the business in that manner effectively. I think this is one of the important points when thinking about the future of Japan, and I would like to work with all of you - customers, mega banks, other investors, and financial institutions - to contribute to the development of this market.

Wakako Sato, Refinitiv LPC: We have several questions from the audience. Ms Kajiwara, taxonomy regulations were adopted in June in the EU, and these will be applied to future operations. How do you think Japan should approach this?

Atsuko Kajiwara, JCR: JCR is involved with positive impact finance task force at the Ministry of the Environment, and the environmental innovation finance study group that includes transitions to decarbonisation initiatives at the Ministry of Economy, Trade and Industry. As for the current discussion, of course, we are referring to the EU taxonomy as a leading example, but we don’t recognise it as it a global standard.

As has already been made clear in today’s discussion, we have a unique industrial structure in Japan with an energy mix policy, and there are also the different roles of direct and indirect finance. Japan’s unique movement based on this will accelerate. This doesn’t mean that we will be completely different from the EU, as I think many things are common, but in particular the target of zero emissions in 2050, on which Japan’s prime minister has just made an announcement, will take a path to achieve. We have green bonds at the moment, and I think you will see many things as well as environmental improvement projects along the long path. As Mr Muto said, how we will move toward decarbonisation and low carbon while supporting the high-emission industries is important not only for the companies, but it is something that we cannot avoid if Japan seriously tries to achieve zero emissions.

What we need is engagement, rather than divestment. Financial inclusion has been mentioned but how the whole of society can make efforts to reduce fossil fuel use is the key to the future.

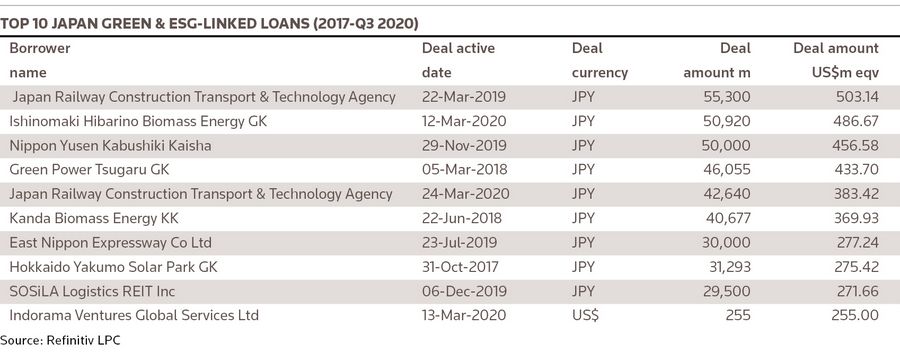

Wakako Sato, Refinitiv LPC: I have received a question related to a chart. What is the background of the contraction in green loan volume from 2017 to 2019?

Tadahiro Kaneko, SMBC: I think this was because of the slight decrease in number of renewable energy project finance such as mega solar projects due to the impact of the reduced FIT [feed-in tariff] prices.

Wakako Sato, Refinitiv LPC: Another question is about SLLs, whether there have been any difficulties in the discussions on setting ESG KPIs and target values as well as adjustment of margins in sustainability-linked loans.

Yasushi Goto, Mizuho Bank: A major feature of SLLs is that pricing fluctuates. Then, the most important point is that it is quite difficult to find the level of pricing that is in line with KPI goals set by companies and is accepted in the market.

Last year, NYK executed the first SLL and the market has gained a lot of momentum. Based on this, I think the market will expand further, and we would like to be involved there as well.

Wakako Sato, Refinitiv LPC: Thank you very much for your time today. I would like to thank the sponsors, Mizuho Bank, MUFG, and Sumitomo Mitsui Banking Corp, and the panellists. I hope you find today’s discussion meaningful.

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@refinitiv.com