With increased attention on the ESG sector, the second-party opinion providers have come under greater scrutiny from regulators and the maturing of the sector should lead to greater transparency and harmonisation.

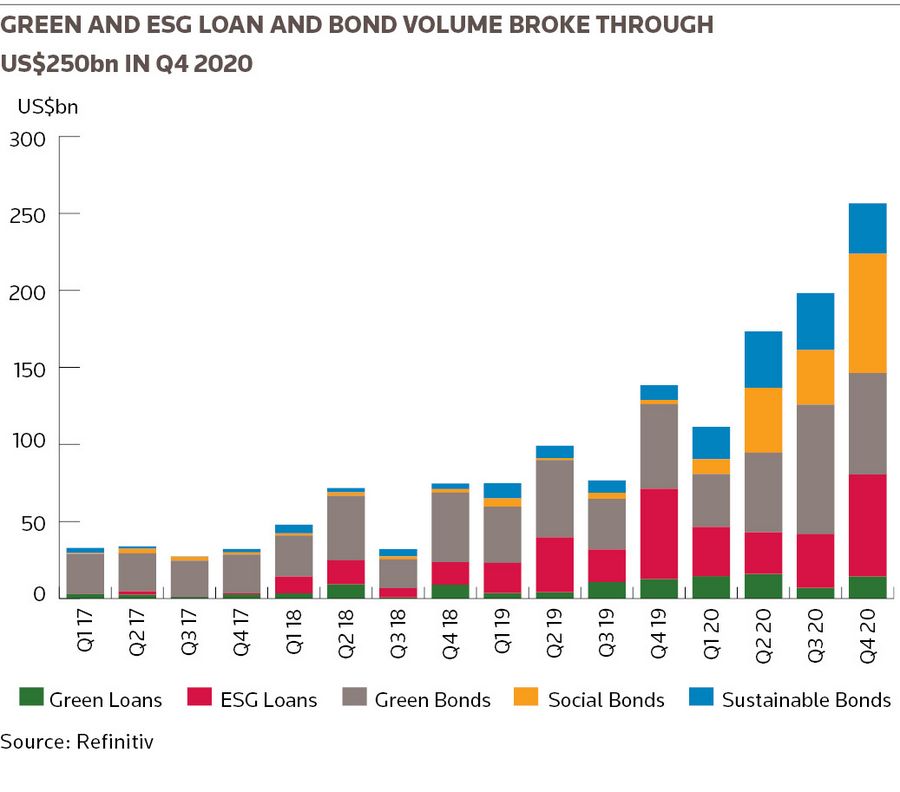

Environmental, social and governance financing became mainstream in 2020. Any attempt to parody it as a niche asset class for do-gooders and tree-huggers became even more unsustainable than it already was.

But with greater awareness of ESG issues comes greater attention on the asset class’s gatekeepers: the second-party opinion providers that determine (like some kind of ESG Santa Claus) who has been naughty and who has been nice – and hand out certifications to that effect in the form of ESG ratings.

It is a very young industry – just over a decade old – that is still in considerable flux and questions have understandably arisen about how providers come to the decisions they do, and, in the case of those companies that certify actual deals (as opposed to hand out general ESG scores) the moral hazard of rating a company that is paying you.

The problematic example that has become a cause celebre in the sector was highlighted in a 2018 report from US think-tank the American Council for Capital Formation called “Ratings that don’t rate: the subjective world of ESG rating agencies”. Looking at the automotive sector, it pointed out that while Germany’s BMW has a positive rating – indeed it is in the 93rd percentile (where a rating closer to 100 is better) – electric car major Tesla is not only below every single European auto manufacturer, it is even ranked below Volkswagen, which became the epitome of ESG naughtiness when it was caught cheating emissions tests.

“The stark contrast between Tesla’s score and the scores of European manufacturers typifies the lack of objectivity in these scores,” concluded author Tim Doyle.

The second-party opinion providers are aware of what appears to be a significant disconnect. But, as ever, things aren’t as simple as they first appear.

“Tesla typically gets relatively poor ESG scores,” said Leon Saunders Calvert, head of sustainable investing and fund ratings at Refinitiv, which owns IFR.

“You’ve got problems with governance because you essentially have a charismatic CEO who runs the business on Twitter,” he said, going on to cite problems with Tesla’s supply chain and those surrounding mining for the lithium in its batteries, which is quite carbon-intensive.

“But at the same time, you’ve also got the organisation at the vanguard of decarbonising the automobile industry.”

And it’s not just the auto industry that causes methodological confusion.

In early December a report from Ping An Insurance Group of China in conjunction with the Brevan Howard Centre at Imperial College London used artificial intelligence to look at companies’ climate-risk disclosures. It concluded that opaqueness may implicitly be rewarded by unsophisticated rating tools.

“This gives perverse incentives for selective non-disclosure, leading to greenwashing,” the report said, pointing at the opinion providers.

Another troubling example comes from Ulf Erlandsson, founder and executive chair of the Anthropocene Fixed Income Institute, which takes a market-based approach to positive climate impact in fixed income markets. He points to research he has done into Adani Power, India’s largest publicly traded coal-fired power generator.

Thanks to a recent move into a solar energy project in Gujarat, the company has, he said, achieved a 94th percentile ESG metric score from some providers and is included in an important emerging market ESG index.

“With 99.7% coal-based generation capacity, we believe the company should be affected by coal-investment exclusion criteria rather than a candidate for best-in-class ESG inclusion,” Erlandsson said.

Case for the defence

Three perhaps isolated examples, but are they symptomatic of wider problems and do they together make a pretty damning case for the prosecution?

Not according to second-party opinion providers, who say that such complaints are not comparing apples with apples.

“The first thing to mention is that ESG is not one thing. The point is that all those issues are actually quite different from each other,” said one industry insider, adding that such problems come from a lack of standardisation within the industry.

“One of the issues at the moment is that the range of methodologies and approaches is just too diverse,” said Andrew Steel, global head of sustainable finance at Fitch.

Benjamin Cliquet, head of sustainable finance services at V.E (Vigeo Eiris) in Paris, agreed. “Increasing diversity comes with an increasing number of benchmarks all over the world by different organisations to be sure that all the market players are aligned to work with these new sectors,” he said.

And, as Saunders Calvert points out, there’s no ESG-equivalent of a balance sheet, cashflow statement or P&L that would make assessments easier.

All gone wrong

Hand in hand with methodological issues and those of metrics is that the sector is still trying to work out what happens when things go wrong.

Steel points to the case of the new airport in Mexico City, which still gives many in the industry sleepless nights. Mexico City Airport Trust sold US$6bn of green bonds in 2016 and 2017 to finance the New Mexico City International Airport.

But the project went off the rails after President Andres Manuel Lopez Obrador took office in January 2018. He cancelled the project, leaving investors in limbo. “The airport authority has drawn down the funding but the project for which it’s supposed to be drawn down is no longer happening,” said Steel. Although a solution has been cobbled together, it raises more questions than it answers and no one remains especially happy.

Those in the industry would characterise those problems as teething trouble and there is something to be said for this interpretation given the clear direction of travel.

Michael Wilkins, managing director for sustainable finance at S&P, points out that credit ratings have been around for more than a century (S&P goes back to 1860, Moody’s to 1900, while Fitch, the youngster, was founded in 1914) and in that time there has been a convergence in what ratings means, how they are constructed and what the methodologies are.

“Clearly there are differences between the major ratings agencies in their criteria and methodology, but ultimately, a rating from S&P or one of the big other ratings agencies means pretty much the same thing,” he said.

It is unlikely to take long for second-party opinion providers to align with each other and most estimates suggest that it will take less than a decade.

See through

When talking to second-party opinion providers, it is easy to dismiss such views as defensiveness. But what gives them some credibility is the notable shift towards transparency.

Sustainalytics’ ratings, for example, used only to be available to clients and institutional investors. They are now available on its website.

“We are seeing different types of global standards and the consolidation of some of those standards,” said Heather Lang, executive director of sustainable finance solutions at Sustainalytics.

The other driver is increased regulation. The UK has already announced that it will make its Task Force on Climate-related Financial Disclosures compulsory from 2022, and the European Union is expected to follow suit. In December, French and Dutch regulators called on the EU’s European Securities and Markets Authority to become the regulator for ESG rating firms in the same way that it already supervises the credit ratings agencies.

This, say the second-party opinion providers unanimously, is going to bring further consistency to the sector and raise the bar across the industry.

What happens next?

As the industry matures, there is likely to be a slowdown in the level of M&A, which has been intense over the past 10 years.

But the main players will try to expand their offerings and standardise what is quickly becoming a global market.

“I don’t know that there’s much scope left for consolidation within the ESG space,” said Lang.

Saunders Calvert believes that the desire to consolidate remains, but it is unlikely to happen among the more mature players. It will be more about identifying the smaller players in the market and the fintech outfits with specialist analytics technology. “When they reach certain levels of maturity, I think you can expect them to be gobbled up relatively quickly,” he said.

The pressure, said Keeran Gwilliam-Beeharee, executive director for market access at V.E, is to expand the offerings of the providers while continuing to standardise. Increased scrutiny means that labelling matters more than ever.

“For everyone in the industry, the devil now really is in the details,” he said.

Main runners and riders and how they differ

Moody’s affiliate VE, formerly Vigeo Eiris, uses a framework of 38 sustainability criteria based on international standards that are grouped into six domains of analysis. These are segmented into 41 sector sub-frameworks selecting and weighting the most relevant objectives. They are assessed through 330 indicators applied to principles of action.

Previously, ESG relevance scores used to be available only individually in rating action commentaries and as PDFs. ESG scores are now available as a data feed and the company claims more than 140,000 data points that cover almost 10,000 issuers and transactions.

A company’s ESG risk rating comprises a quantitative score and a risk category. The quantitative score represents units of unmanaged ESG risk with lower scores representing less unmanaged risk. Unmanaged risk is measured on an open-ended scale starting at zero (no risk) and, for 95% of cases, a maximum score below 50. Based on their quantitative scores, companies are grouped into one of five risk categories: negligible, low, medium, high, or severe.

The company uses data points across 35 ESG issues to identify industry leaders and laggards according to their exposure to ESG risks and how well they manage those risks relative to peers. The issues are weighted according to impact and time horizon of the risk or opportunity. All companies are assessed for corporate governance and corporate behaviour. Its ESG ratings range from leader (AAA, AA), average (A, BBB, BB) to low (B, CCC). MSCI also rates equity and fixed income securities, loans, mutual funds, ETFs and countries.

Refinitiv covers more than 80% of global market capitalisation, across more than 450 different ESG metrics. It measures a company’s relative ESG performance, commitment and effectiveness across 10 main themes such as emissions, environmental product innovation, and human rights, based on publicly reported data. It also provides an overall ESG score that is discounted for significant ESG controversies.

Cicero was first to provide a second opinion on a green bond framework, for the World Bank in 2008. A “shades of green” methodology is used to assess climate risk in the green finance market. It focuses on avoiding lock-in of greenhouse gas emissions over assets’ lifetime and on promoting transparency in resiliency planning and strategy. Cicero allocates a shade of green (or brown) to revenues and investments depending on how well they are aligned with what it calls “a low-carbon, climate resilient future”.

In August, Bloomberg launched ESG scores for 252 companies in the oil and gas sector, and board composition scores for more than 4,300 companies. ESG scores began with the oil and gas sector because it said that there is typically stronger data disclosure from these companies. The governance scores start with board composition and rank the relative performance of companies across the four areas of diversity, tenure, overboarding and independence.

S&P’s ESG profile reflects an entity’s activities and starts by applying the outputs from the S&P Global Ratings ESG Risk Atlas to the entity’s sector and regional footprint. Following the acquisition of SAM ESG Ratings and Benchmarking business from RobecoSAM in January 2020, S&P reports include the SAM Corporate Sustainability Assessment, an annual evaluation of a company’s sustainability practices.

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@lseg.com