Hitting it for six:

Best-in-class return on equity, best share price performance of its peers, record revenues across a now balanced institution – and a deal roster to be proud of. Given the tragic circumstances of 2020, a victory lap for those who have been along for the journey might be unseemly. But a quiet moment of satisfaction is surely in order. Morgan Stanley is IFR’s Bank of the Year.

For Morgan Stanley, 2020 was both a culmination of a decade-long journey to a balanced business model and a stress test of whether the bank was in the right shape to thrive when times were tough but opportunity knocked.

“Our strategy revolves around demonstrating stability in times of serious stress and delivering strong results when markets are active,” said James Gorman, the bank’s chairman and CEO.

“2020 tested this thesis,” he added, in what might just be the understatement of the year.

It was a test that Morgan Stanley passed with flying colours.

But before we address the tragedies and triumphs of 2020 it is necessary to go back to the period that followed the financial crisis – a crisis that provided a near-death experience for Morgan Stanley.

It was clear to everyone after 2008 that the bank’s pre-crisis model was no longer fit for purpose.

No one saw this more clearly than Gorman: before the crisis, when he was chief operating officer for Morgan Stanley’s wealth management business, he had been telling anyone who would listen that the annuity-like revenues from wealth and investment management were the perfect complement to offset the volatility inherent in sell-side activities.

Gorman’s reputation as a straight-talking Aussie can be bit overdone – he’s not exactly your average ocker – but it is fair to say that he was explicit about what he planned to do when he took over from John Mack (as CEO in 2010 and chairman in 2012) and he’s pretty much done it, with minimum fuss and maximum focus.

He got the CEO job largely as a result of his successful advocacy of a deal that saw Morgan Stanley buy 65% of Smith Barney, Citigroup’s wealth management venture, in the aftermath of the financial crisis and in 2012 consolidated the push by buying the remaining 35% stake to create Morgan Stanley Wealth Management.

The effort to ramp up that side of the shop culminated in 2020 with the October acquisition of online brokerage E*Trade (in a US$13bn all-stock deal) and an agreement announced at much the same time to buy asset manager Eaton Vance for US$7bn.

The combined businesses will oversee US$4.4trn of assets – and bring in about US$26bn of annual revenue. And those are dependable revenues (“annuitised” in the jargon) that use relatively little of that most precious commodity in modern finance – capital. Vitally, their predictability is also something to which investors and analysts assign high values.

That Gorman and his lieutenants are on the right track was confirmed when JP Morgan’s Jamie Dimon (who Gorman outbid for Eaton Vance) told an investor conference that Morgan Stanley had “done a good job” with the E*Trade and Eaton Vance transactions. Dimon added that he still hoped to add scale in asset management.

A grudging compliment from Dimon is not something to sniffed at. But the effective compliment that arch-rival Goldman Sachs is also following in Morgan Stanley’s footsteps will be even more enjoyable for Morgan Stanley lifers. How else to think about Goldman’s push into annuity-style good-for-your-multiple businesses like retail banking and wealth management?

No lesser an authority than Wells Fargo’s Mike Mayo, the outspoken doyen of bank analysts (and not known for singing the praises of big bank CEOs), certainly thinks Gorman has got the big calls right.

“Morgan Stanley was more effective than any bank in the last decade at transforming its business model and they are reaping the rewards of that business mix transformation today,” Mayo said.

He sums it up succinctly. “There was very little confidence in Gorman [when he took over]; now he’s viewed as the king of Wall Street,” he said.

Synergy on display

On the full-year results call, Gorman said that in 2020 the trading and investment banking operation (called the institutional securities group) generated more than US$300m of revenue through wealth management referrals, while wealth management gained US$20bn of client assets and investment management gained US$6bn of net flows and commitments from ISG referrals.

That’s your synergy right there.

The new Morgan Stanley is one where “revenues are more recurring, more efficient and more durable”, Gorman told IFR.

Who you gonna call?

But all of this is the story of the past decade, not the past year. And, let’s be honest, as a capital markets publication all this making nice with the buyside is not the most important thing for IFR. What really matters to us is deals.

And Morgan Stanley had a deal roster of extraordinary breadth in 2020.

We’ll have to gallop through the big themes as space doesn’t allow us to go into the thousands of deals (millions if we include trading).

Of course, the biggest of themes in 2020 was the pandemic. When times were tough and companies were making figurative life-or-death fundraising decisions, more often than not they called Morgan Stanley.

“We like to think we are viewed as the trusted adviser, and one who's going to give rock-solid advice,” said Mark Eichorn, one of two global co-heads of investment banking. “I feel like the vector we’ve been on as an organisation and the ability to deliver the integrated investment bank that we've been working so hard to create crystallised just at the precise moment that our clients needed us most.”

No sector had it tougher – or needed more infusions of cash – than travel and tourism. Morgan Stanley was there with a calming word of strategic advice, a reasonably priced loan (well, reasonably priced in the circumstances), or a gutsy underwrite.

Take the airlines. Morgan Stanley was the equity underwriter of choice for the industry, leading a US$6.6bn financing for Southwest (including the largest ever US airline equity offering and largest equity and convert concurrent), United’s US$1.1bn block trade (the largest ever US airline block trade), IAG’s €2.74bn rights issue, Cathay Pacific’s US$5bn recapitalisation and Singapore Airlines’ US$10bn capital raise.

It was also there to help steer cruise line Royal Caribbean away from the rocks. Morgan Stanley played its part in providing a US$2.2bn bridge loan and then helped the company put in place longer-term financing with a US$1bn bond, a US$1.2bn convertible and a US$575m equity trade.

“As their adviser we're there thinking things through. How should we best facilitate you weathering this scare? And what are the products and services we can deliver? What are your shareholders looking for? What are the other creditors, constituents, customers looking for and so on?”, Eichorn said.

Those deals were part of a banner year for the ECM team. Other highlights included the US$1.9bn Warner Music Group IPO; Royalty Pharma’s US$2.5bn IPO; a sole books role on a US$1.1bn 100% secondary block trade for Keurig Dr Pepper which priced amid historic market volatility as the Covid-19 crisis bit in March. The bank was also sole books on a crucial US$1.3bn block trade for Moderna and global coordinator for XP’s US$2.25bn IPO that was the largest US listing of a fintech in 2019.

The Warner Music trade was perhaps particularly notable as it reopened the IPO market in the US. There was, it is safe to say, a host of voices in the industry and elsewhere wondering whether such a deal was wise – or even possible.

“We said let's go ahead and do it – even in the middle of the social unrest in the country and ongoing Covid concerns,” said Evan Damast, global head of equity and fixed income syndicate. “For us it was about our ability to lean in and look forward.”

Morgan Stanley was also a leader in the development of direct listings. It led both Palantir and Asana debuts in 2020 – after direct listing deals for Spotify in 2018 and Slack in 2019. The bank also played a major – and sensible – part in 2020’s SPAC boom.

The bank’s leading presence in both those areas of innovation makes another useful point: while Morgan Stanley bankers might have been expected to be on the back foot as a result of the health crisis and the consequent economic turmoil – and there were certainly moments when the appropriate response was to help clients batten down the hatches – that wasn’t the whole story.

“We could have easily seen a year of defence; defence for clients and defence for the banking sector,” said Mo Assomull, the bank’s head of global capital markets. “In fact, for all the destruction and carnage we've seen, it's been a year of helping clients in an offensive capacity as well. We have helped our clients think strategically with lots of innovation.”

While those were the highlights, there was one notable lowlight – and one offering that could be seen either way. The latter encompasses the bank’s role on the US$29.4bn IPO of Saudi Aramco in December 2019. On the one hand, Morgan Stanley is officially a joint global coordinator on the world’s largest ever IPO. On the other, after years of work, the deal ended up entirely as a domestic affair and Morgan Stanley’s fees reflected that disappointing reality.

The bank did better on other Aramco-related deals, though, advising the company on its US$69bn acquisition of a 70% stake in Sabic and acting as one of just two JGCs on its US$12bn debt IPO.

The lowlight, meanwhile, came in November 2020 when the IPO of Ant Group fell at the final hurdle. The Chinese government stopped the deal because … well, because it’s the Chinese government. As a result, a US$34bn deal that had been priced and fully allocated had to be abandoned just days before trading was due to begin and fees of the best part of US$400m (between all the banks involved) evaporated.

It's got to hurt to be JGC on what should have been both of the world’s biggest IPOs in less than a year only for one to be a damp squib and the other to be abandoned through no fault of your own.

It certainly hurt Morgan Stanley’s 2020 league table position. It still finished in a more than credible second spot in the 2020 Refinitiv rankings with US$81.8bn of common stock underwriting credit – just over US$3bn behind Goldman Sachs. A successful Ant deal would have made all the difference.

Debt powerhouse

Morgan Stanley’s approach to the debt markets is less of a league table game than with ECM. But pound for pound it more than punches its weight.

Again, the response to Covid-19 was a theme, as the bank helped those in the most troubled sectors of aviation/travel, autos and retailers.

Morgan Stanley drove deals for Southwest, Delta, AerCap and Boeing and placed US$2bn in first and second-lien term loans for Airbnb.

High-yield highlights include Netflix’s US$1bn multi‐tranche offering (Morgan Stanley’s 11th lead‐left financing for Netflix out of 11 transactions – a 100% market share); and multiple financings for Uber, including a US$1bn deal in May and another US$500m trade in September (the seventh and eighth Morgan Stanley-led deals for Uber – again for a 100% market share).

In acquisition financing Morgan Stanley was there on many of the year’s most high-profile transactions, including AbbVie’s US$38bn acquisition financing package and US$30bn bond offering to acquire Allergan. Morgan Stanley and its partner MUFG underwrote the US$38bn bridge facility and concurrently syndicated a US$6bn term loan and a US$4bn revolving credit facility before the bank helped arrange the take-outs and related exchange offers. The deals were one of the largest bridges and corporate bond raises of all time.

The AbbVie/Allergan engagement – the actual acquisition totalled US$83.9bn – was a highlight in a barnstorming year in M&A. To give a brief flavour, these were the biggest three deals Morgan Stanley advised on in the awards period apart from the deals for AbbVie and Aramco: Bristol‐Myers Squibb’s acquisition of Celgene – US$93.4bn; United Technologies merger with Raytheon – US$89.8bn; and T‐Mobile US’s merger with Sprint – US$58.7bn.

Notable moments in emerging markets DCM, meanwhile, include a bookrunner slot on Santander Mexico’s US$1.75bn debt raise – the first Mexican issuer after the coronavirus crisis began – and acting as a bookrunner on the first ever sustainability-linked bond from the emerging markets – a US$750m trade for Brazilian paper outfit Suzano.

That last deal also highlights the bank’s efforts in ESG. In terms of transactions, standout moments included Alphabet’s US$10bn sustainability bond, the largest ESG offering ever and Alphabet’s largest debt offering; PepsiCo’s inaugural US$1bn green bond; MUFG’s €500m sustainability bond to address the impact of Covid‐19; Pfizer’s US$1.25bn sustainability bond, the first ever healthcare sustainability bond; and EDF’s €2.4bn green convertible, the largest green bond and largest equity‐linked issuance in 2020. Another significant deal was Ford Foundation’s US$1bn social bond, the first ever by a US non-profit foundation, raising money to aid vulnerable communities hard hit by the pandemic.

It also made a contribution to ESG issues directly, with a US$1bn social bond to support affordable housing projects and a pledge to reach net‐zero “financed emissions” by 2050 (a term that refers to greenhouse gases emitted by entities that receive financial services, loans or investments from Morgan Stanley).

Trading going places

Of course all this out-performance in capital markets is made possible by the equivalent trading businesses. Those blew out the lights in 2020, helped by the fact that in late February and early March as the corona crisis took hold, the bank saw the 10 busiest days in cash volume terms in its history.

Space is limited, so we will have to rush past the extraordinary success of Morgan Stanley’s equities business, pausing only to note that it led the industry once again in 2020 in terms of revenues and was top of the tree for the seventh year on the trot. Its full-year revenues were US$9.8bn – up 22% from 2019.

It is worth focusing briefly, though, on the remarkable performance of the fixed-income sales and trading operation. Remarkable not just because of the money it brought in – though that was US$8.8bn, up an impressive 59% year on year – but because Morgan Stanley has rebuilt the business after downsizing it in 2015.

The main reason for the bounce-back is Morgan Stanley’s top quality execution – a result in part of electronification and massive IT spend (itself cross-fertilised from the equities franchise).

Wells Fargo’s Mayo sums up the results nicely. “FICC execution at Morgan Stanley is amazing. They downsized fixed income, re-segmented it and the business still shows outstanding results.”

Life sentence

Ask Morgan Stanley people for the secret of this success and the most frequent answer is longevity. Most of the senior people are lifers and for many that term has been 20-plus years without remission.

“What is the special sauce? The special sauce is that we’ve got a group of senior managers who’ve been together for 25 years who’ve been through everything together,” said Ted Pick, the head of ISG.

And that of course was tested when the coronacrisis hit and people were suddenly making franchise (and career)-defining underwriting and capital-commitment decisions while working from spare rooms and basements.

“Many of us have been at the firm a long time. That means we know each other, we trust each other, we know what the ethical compass is for everybody. So that enabled us to make very good decisions, but also to communicate very efficiently and very openly,” said Susie Huang, the bank’s other global co-head of IB.

“And I think that was also part and parcel of why our clients came to us. Because you don't have a lot of time to listen to the presentations in the middle of Covid-19.”

Cashing in

The financial results of all this frantic activity are suitably spectacular.

Revenues across the bank in 2020 were US$48bn (including the contribution from E*Trade). That is up 16% from last year – and 41% up on 2014. In ISG, full-year revenues were US$26bn – 27% higher than last year. Of that, IB revenues were US$7.2bn – 26% up on 2019.

That resulted in an industry-leading return on tangible common equity of 15.2% for 2020. For comparison, JP Morgan’s ROTE was 14%, Goldman’s was 11.8%, Bank of America’s was 9.5% and Citigroup’s 6.9%.

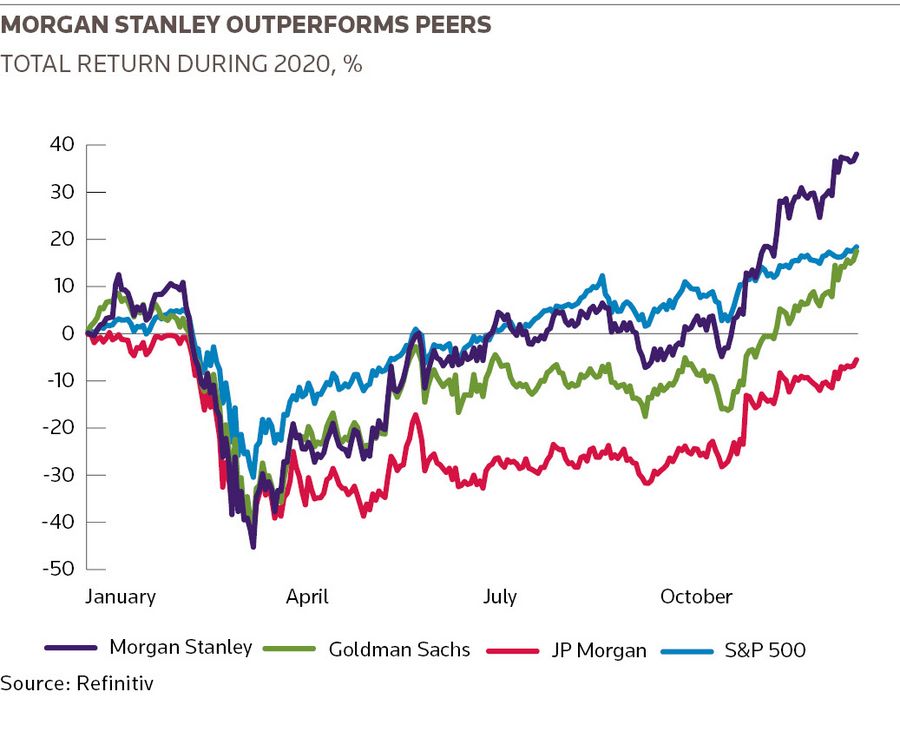

Another result of all the money pouring in was a share price that put the rest of the industry to shame. Morgan Stanley’s shares were up 38% over 2020 (in part thanks to the value investors put on all those lovely annuitised earnings). Of the other big banks, only Goldman was in positive territory (up 17%).

There’s a final way to measure that progress: credit ratings. This is instructive because it tells the story of the bank’s turnaround. Everyone who worked at Morgan Stanley in June 2012 (and that seems to be nearly all of them), remembers with a shudder the moment when Moody’s nearly downgraded the bank by three notches at once. Such a move would have been close to disastrous, but in the end the bank got away with a two-notch hit (to Baa1).

So it was quite a moment when, shortly after the close of the E*Trade acquisition, Moody’s upgraded Morgan Stanley to A1 – the joint highest ratings of the big US banks (alongside JP Morgan, Bank of America and Wells Fargo) – and left it on review for a further upgrade. Moody’s said: “The acquisition of E*Trade is another deliberative step in MS's clear and consistent strategy to shift its business mix towards generating recurring, profitable revenue streams in wealth and investment management.” *

And if that isn’t an endorsement of the progress Morgan Stanley has made in the last decade under the stewardship of Gorman, it’s hard to imagine what is.

The fact that all this has taken place for the best part of the past year against an unprecedented health and economic crisis makes that achievement all the more impressive.

Said Gorman: “Unlike over a decade ago, banks in this crisis have had the capital and liquidity to help their clients and, through that, the real economy. At Morgan Stanley, we’ve continued to focus on clients, our employees, and our communities, and have been able to do so while generating strong returns for our shareholders by delivering record financial performance. I couldn’t be prouder of my colleagues for their commitment and their resilience during this very difficult year.”

Additional reporting by Philip Scipio

* This paragraph was amended to correct the credit rating of Morgan Stanley

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@lseg.com