Banks’ credit trading desks are reaping the rewards of a surge in portfolio and algorithmic trading activity, the latest sign of how technology is revolutionising the way corporate bond markets are traded to the benefit of a handful of mainly US banks.

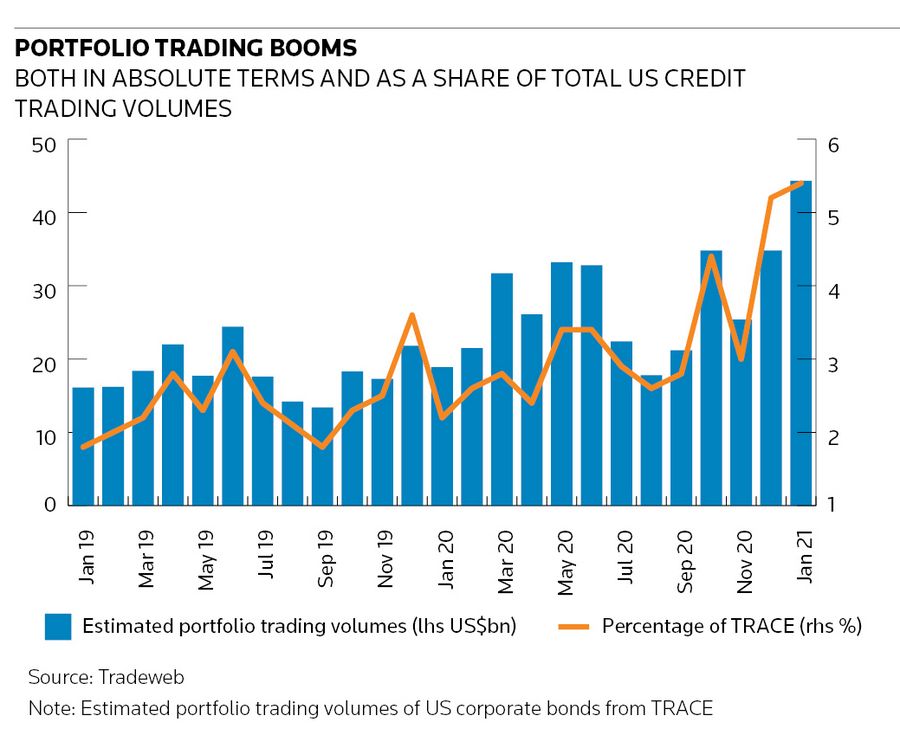

Portfolio trades in US corporate bond markets increased by nearly 50% last year to US$321bn, according to estimates from Tradeweb, as a growing number of investors are buying and selling large blocks of bonds in one go.

The growth forms part of a broader shift towards electronic trading of corporate debt – a corner of finance that has been slower to adopt the kind of automated trading practices common in equity and currency markets.

So far that is proving particularly lucrative for banks such as Citigroup, Goldman Sachs, JP Morgan and Morgan Stanley that have invested heavily in the infrastructure and technology needed to handle this kind of high-volume business in recent years.

The top 12 investment banks made about US$2bn from portfolio and algorithmic trading last year, according to analytics firm Coalition Greenwich. That came amid an already bumper year for overall flow credit trading where industry revenues hit a decade high of around US$12bn, Coalition Greenwich data show.

Many believe the trend only has further to run, with banks now extending portfolio trading practices to other asset classes including loans, municipal bonds and mortgage-backed securities.

“Credit is in the throes of some considerable structural changes,” said Austin Garrison, head of North American credit trading at JP Morgan. “We view [portfolio trading] as part of a broader ecosystem of electronic trading – including create-and-redeem baskets for ETFs and systematic market-making – that allows us ultimately to price risk more accurately and efficiently.”

The portfolio trading boom is a result of a quiet revolution on corporate bond desks in recent years, with banks using algorithms to price bonds far quicker than any human trader could. In a portfolio trade, fund managers can offload hundreds of securities sometimes totaling over US$2bn in the space of an hour – and at a cheaper price than executing a series of individual trades over a day or so. That has made rotating from one sector to another or extending the duration of an entire portfolio far more efficient.

Now, portfolio trading is expanding – and fast. Bankers say the client base for such trades tripled last year. It accounted for a record 5.4% of all corporate bond transactions in the US in January, Tradeweb estimates, up from 2.2% in January 2020.

In a sign of its growing significance, Goldman’s Stephen Scherr took the unprecedented step for a bank’s chief financial officer of singling out portfolio trading on a fourth-quarter earnings call for driving market share gains in credit trading.

“The electronification of the corporate bond market has been turbocharged in the last two years,” said Vikram Prasad, global head of credit trading at Citigroup. “Clients want this liquidity – their assets have grown, mandates have evolved and they need greater ease of execution, whether that’s for odd-lots trading, ETFs or portfolio trading.”

Lightbulb moment

The development of bond trading at Morgan Stanley, one of the banks at the forefront of this trend, provides a vivid illustration of how credit markets have evolved. Back in 2015, Morgan Stanley’s corporate-bond traders were receiving 15,000 or so client enquiries each day, but were only able to respond to a fraction of them.

The answer, it decided, was to invest heavily in technology. It switched on its new algorithmic corporate bond pricing engine in 2017 and went from being able to price electronically about 500 different bonds to now more than 10,000 bonds.

"It was like a lightbulb went off,” said Ed Bayliss, Morgan Stanley’s head of US investment grade and macro credit trading. “It would allow our traders to focus on meaningful, larger risk and lets the algo handle trades we aren’t able to respond to.”

The following year Morgan Stanley created its portfolio trading desk and volumes have been growing ever since. Today, its algo and portfolio trading account for about 80% of its corporate bond tickets and 20% of volumes.

“What started off as a solution to efficiently provide clients with electronic liquidity for odd lots, quickly expanded to become a key component in portfolio trading and fixed income ETFs,” said Bayliss.

Risk recycling

If algos have supplied the necessary technology, the growing prominence of exchange-traded funds in credit markets has also played a vital role in this expansion by providing another outlet for banks to recycle their wide-ranging positions. One way traders can do that is through the "create-and-redeem" process for ETF shares, as money flows in and out of these products.

Trading volumes across US fixed-income ETFs rose 52% last year to US$4.2trn according to BlackRock. The coronavirus sell-off last March, in particular, showed how more investors are using broad-based benchmarks to do something once thought barely possible in modern credit markets: trade quickly and in large size when markets get rough.

Average daily volumes for US fixed-income ETF trading reached US$34bn in March, a 207% increase on the previous year’s average for these products. Portfolio trading volumes also jumped at about this time as investors reshuffled exposures.

"There were a lot of natural things happening in credit markets – ETF create-redeem, transition trades – that led to the advent of portfolio trading," said Chris Bruner, head of US institutional fixed income at Tradeweb. "But how quickly it has become a necessary part of the market has surprised us."

Better price

It's not just the ease and speed of trading that’s attracting more investors – there’s also the prospect of securing a better price. Traders estimate portfolio trades can reduce the overall bid-offer spread by up to a quarter – and potentially even more if the client is willing to incorporate some suggested tweaks to the portfolio in question.

Traders say that is because they have a clearer picture of what clients are doing compared with a drip-feed of trades over the course of a day or so.

Many believe these technologies will encourage more trading activity altogether, as investors realise they can now discard small, unwanted positions with greater ease. Portfolio trading is also being applied to other markets, such as helping collateralised loan obligation managers rejig positions.

"We see portfolio trading growing outside corporate bonds: for the loan business, munis, mortgage-backed securities and emerging markets. This is going to expand the market and go cross-asset for a lot of clients,” said Derek Hafer, global head of spread products portfolio trading at Citigroup.

The numbers in paragraphs 18 and 19 have been updated to reflect US fixed-income ETF trading volumes. A previous version of this article cited fixed-income UCITS ETF volumes.