Goldman Sachs netted significant profits trading interest-rate options during the recent sell-off in US Treasuries, according to sources familiar with the matter, marking it out as one of the only investment banks to gain from wild swings in this corner of financial markets this year.

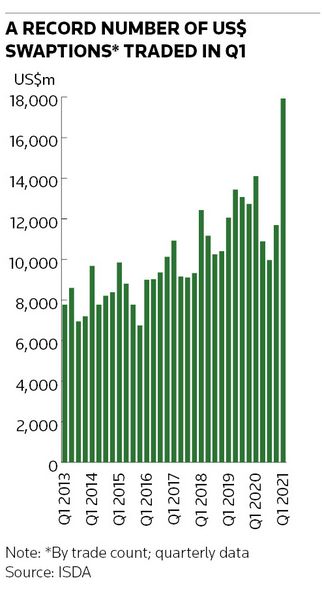

Bank trading desks had to contend with some of the most explosive moves in US interest-rate option markets since the 2008 financial crisis when Treasury yields jerked higher during the first quarter. A record of nearly 18,000 US dollar swaption trades changed hands over that period, according to data from ISDA, comfortably the most ever in a quarter.

Hedge funds had used these derivatives to bet on an upwards lurch in rates in anticipation of a re-emergence of inflationary pressures in the US. That largely one-way flow left many bank trading desks vulnerable, triggering a scramble to cover positions when rates started to rise.

Using swaptions to position for higher US rates proved to be a hugely lucrative strategy. Bill Ackman’s Pershing Square Holdings, for instance, reported it made hundreds of millions of dollars from such trades this year.

Goldman has extensive reach in the hedge fund community and so was well placed both to help some of these clients place swaptions bets ahead of the sell-off and to position itself to profit when interest-rate volatility surged, sources said.

Goldman was also the only major US investment bank to report "significantly higher" rates trading revenues in first-quarter results announcements. Rates trading contributed to a 31% yearly increase in fixed-income revenues at the bank.

“In rates, revenues rose amidst strong risk management and client engagement, particularly on the back of anticipated fiscal activity in the US and diverging central bank actions,” Stephen Scherr, Goldman’s chief financial officer said on a first-quarter earnings call. A Goldman spokesperson declined to comment.

Bank of America, Citigroup, JP Morgan and Morgan Stanley said trading revenues in their broader rates businesses were lower in the first quarter following a very strong period for these units at the start of 2020. There are no reports of US banks sustaining notable losses in swaptions books this year.

Most were wary of the lop-sided nature of hedge fund flows as well as the potential for Treasury yields to break higher and deliberately kept positioning light, sources said, while also looking to offset risks with other exposures.

“We saw huge amounts of buyside clients using deeply-out-the-money swaptions to short rates. That’s why some of the moves in the US were so dramatic because there were some strikes out there that were complicated for banks to risk manage,” said one senior rates trader at a global bank.

Leveraged rates bet

Swaptions provide a way for traders to place leveraged bets on the direction of interest rates, giving the buyer the right to enter an interest-rate swap contract in the future at a pre-agreed level.

Interest-rate volatility – a proxy for the cost of swaptions – was low by historical standards heading into 2021, increasing the appeal of these derivatives for those expecting Treasury yields to rise in anticipation of a build-up of inflationary pressures.

Reflation became a dominant theme in the first few months of the year as a result of the Biden administration’s plans to increase fiscal spending along with hopes that an acceleration in the US’s vaccination programme would bring the Covid-19 pandemic under control.

One popular trade was using swaptions to bet on a move higher in short-dated relative to long-dated rates – a strategy designed to profit from investors pricing in the Federal Reserve raising interest rates to combat inflation sooner than previously expected.

Anyone who timed it right made serious money. Pershing Square said in its annual report published in late March that it owned “very large notional hedges" in the form of swaptions that it started buying in December through to early February. That hedge initially cost US$157m, but subsequently more than tripled in value to US$493m.

“Our interest rate swaption position is highly asymmetric; it has a potential pay-off that is many multiples of our capital at risk,” the hedge fund wrote in the report.

Extreme volatility

The difference in volatility between at the-money and out-the-money US swaptions – a measure known as skew – reached all-time highs in March, according to Citigroup strategists, indicating there was record demand for swaptions as traders bet on a move higher in rates.

Short-dated swaptions contracts linked to five-year US interest rates registered their largest one-day increase in volatility since the 2008 financial crisis, the strategists said, in another sign of the stress these markets were under.

“February was a big shock – the repricings in rates volatility markets happened very quickly and were very extreme,” said Mike Chang, interest rate derivatives strategist at Citigroup. “That persisted for much longer than lots of people expected. There was definitely this need to position for the possibility of yields breaking higher.”

The moves in derivatives markets have since subsided as Treasury yields have stabilised in recent weeks. That has included one of the fastest declines in short-dated swaptions skew in history, according to Citigroup strategists.

“The volatility market and skew got so extreme it essentially made it worthwhile for investors or for dealers to take the other side of that position,” said Chang. “Fears over this yield break-out have now abated quite a bit and markets are more balanced."