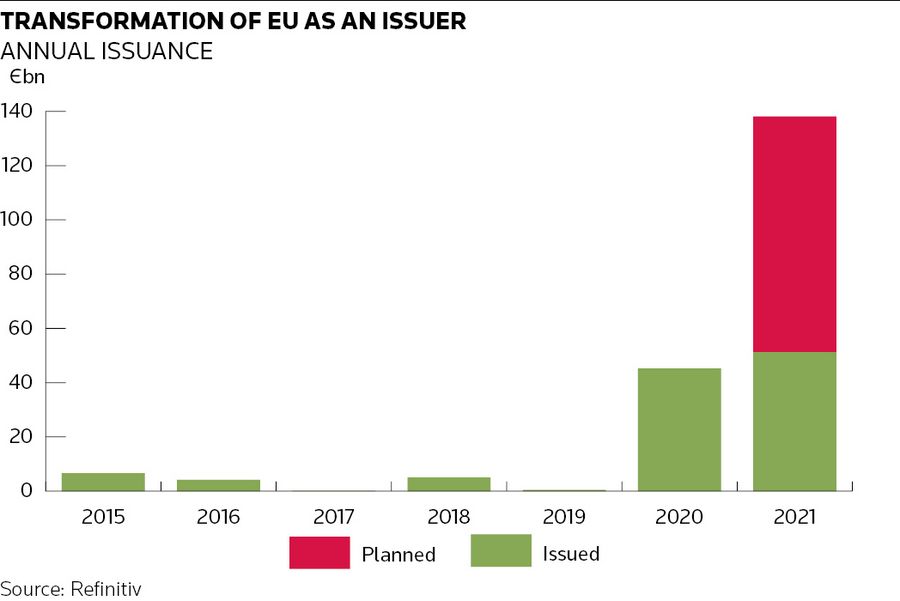

Little more than a year ago, the European Union was nothing more than a bit-part player in the global capital markets. The two or three bond deals that it would typically bring to market in a normal year were often small and would pass by with scant attention from the markets.

It took its first step into the big league with the launch of its €90bn SURE programme in October. But this week the EU will change gear entirely with the launch of NextGenerationEU, which will see the EU raise more than €800bn over five years, transforming it into one of the world’s biggest bond issuers.

Everything changed last April at a summit to put together a pandemic stimulus plan, when the people in the funding team were asked how far they might expand the programme. They thought that, at a push, they might raise a maximum of €80bn a year in the markets. But when the summit ended, they were told they would need to raise double that.

“We were crossing the Rubicon,” said one official. “What we were doing previously was very plain vanilla stuff and suddenly it was a very different ball game . . . it was just a question of throwing overboard everything we've done before and starting to say, ‘okay, if we're going to do this, this is completely different. How do we build it? How do we build a machine that's going to do it?’.”

The team spent the first few months figuring out what resources it would need and bringing the right people in to build a new, bigger funding body. It seconded individuals from the bloc’s other big funding vehicle – the European Stability Mechanism, which finances eurozone crisis-era loans to Greece, Ireland, Portugal, Cyprus and Spain – who had experience of big bond programmes.

Balancing act

Given that the team was essentially building a debt management office within the European Commission (which borrows on behalf of the EU), it was natural for it to turn to the national DMOs. It has been a delicate balancing act of seeking help – including hiring staff – from member states without upsetting them by poaching too many people. Member states, after all, also have much higher borrowing needs as a result of the pandemic.

“We’re a kind of giant new kid in class, stomping around the playground in clogs,” said the official. “We have to be mindful of that and work with the DMOs and communicate with them. We were very careful to do that. They, on the other hand, have understood that we're funding our member state economies and public administration, and they want us to succeed.”

The team has had something of a dress rehearsal for NextGenerationEU with the SURE – support to mitigate unemployment risks in an emergency – programme. Since the first SURE deal in October, the funding team has raised €90bn through seven transactions, allowing it to test its processes, create a liquid secondary curve and establish itself as a large and frequent issuer.

But NextGenerationEU will be markedly different, not least because issuance volumes will almost double. All of the SURE transactions have been syndicated by banks and strict conditions were placed on maturities and size. And while syndication will remain an important component in funding, with one deal every month planned, the team has also put together an auction platform that should be up and running from September.

Indeed, the creation of an auction facility has been the single biggest piece of work for the team. While auctions are a cheaper way to sell debt than bank syndication, they require more set-up work. To save time and avoid lengthy private procurement processes, the team has instead sought help from public-sector institutions such as the European Central Bank.

Flexibility

The plan is to have a monthly auction alongside a monthly syndication, with bonds as well as short-term bills – something new that was not previously used for the SURE programme – being sold. The auctions will give the funding team additional flexibility, allowing them to raise more or less funds depending on the needs of recipient countries.

“Finding a fit-for-purpose auction platform was another big thing that has gone very well,” said the official, adding that they plan to onboard banks over the summer. “We have been looking to find a good public sector partner who was willing to make that available – of course on a compensation basis – for us. We are now working on the last few points on that dealer contract with them.”

An impressive 39 banks made the list of primary dealers for the EU, although not all of them will be hired as lead managers for syndicated deals, with those fined for colluding on trading of government bonds excluded from that role – at least for the moment.

Just over €720bn of the money raised over the next five years will fund the EU’s post-pandemic recovery and resilience facility. Of that, around 55% of that will take the form of loans to be paid back by member states. The rest – as well as a further €80bn via other programmes – will be grants, to be paid back by the Commission through budget increases and new carbon and digital taxes.

Once the auction is up and running in September, the team will – on top of managing monthly issuance – turn to the final pieces needed to make the Commission a fully operational DMO. Swaps facilities could be added to allow it to fix the rate at which it lends on money to member states. Futures contracts may also follow to help liquidity.

For now, there seems to be no shortage of demand for bonds. The first SURE deal attracted more than €233bn of orders for the €17bn of bonds on sale. Central banks including the ECB continue to hoover up bonds to support the economy, and indeed about a fifth of SURE bonds went to such institutions. But fund managers and banks were even bigger buyers.

No risks

But given the volume of issuance – expected to be around €150bn a year when everything is up and running – the team is taking no risks. While a lot of work has happened over the past year, the funding team is under no illusions that it has also benefited from the huge changes that the bloc has seen in the past decade – many enacted to prevent the eurozone crisis from spiralling out of control.

“We have benefited from a lot of tailwinds – from member states, from our partners at the ESM, the EIB, and the ECB,” said the official. “I think you really get the sense that this is a project that everybody needs to succeed. The member states are very much supportive. They clearly need to see that everything is properly accounted for and have confidence in this machinery.”

“So far we've been able to do that.”