Financial services firms are growing their ESG advice businesses at a fast clip, as a surge in deal flow strains the nascent market for sustainable debt. Having more second-party opinion providers may ease the bottleneck for some new issuers. Yet that will not be the end of the growing pains for this evolving industry.

MSCI, a frontrunner in green bond indices, is planning to begin providing second-party opinions, while industry rivals are ramping up existing advisory operations to meet overwhelming demand for an increasing variety of deals. ISS ESG aims to quadruple its opinion-provider staff this year, and Sustainalytics has already tripled the size of its team in 2021, with more expansion expected.

They are all aiming at a swelling target. The market for new ESG bond and loan issuance in the first half of this year, at US$850bn, already exceeds 2020’s full-year total of US$766bn, according to Refinitiv data.

Yet market participants said that the challenge of opinion-provider capacity might take a long time to get better – even as these firms up their game. The market is growing too fast and unpredictably.

Top arranging banks said that the time taken to get a second-party opinion from top providers has doubled recently to around four weeks, which could curb borrowers' ability to issue quickfire opportunistic deals.

“SPO providers will tell you that they’re very aggressively hiring, but it’s not turn-key – the bottleneck won’t ease overnight,” said Scott Roose, head of ESG debt capital markets for the Americas at Credit Suisse. “This is a problem, and it’s probably going to get worse. But we will have to proactively manage upcoming supply.”

SLBs drain resources

The problem is not just one of blunt capacity. The market has become more sophisticated with more companies, in the race to show improvements in their emissions records, seeking to issue ESG debt beyond traditional green bonds. Since Italian energy utility Enel in 2019 became the first to price a sustainability-linked bond, issuers have grown more comfortable with deals that tie coupons to company-wide ESG performance targets.

SLBs often require more time and resources from issuers, banks and opinion providers. And these demands and timelines do not always match the imperatives of the capital markets, where issuers are keen to take advantage of the current boom in ESG financing and want to be able to fund in the opportunistic way they are used to.

“What we’re seeing is that the timelines for issuers tend to be shorter with SLBs, compared with green bonds,” said Heather Lang, Sustainalytics’ executive director of corporate solutions. “And SLBs tend to be more complex than a straightforward use of proceeds deal, which can be turned around pretty quickly.”

The benefits of sustainability-linked securities are not only financial. A successful SLB can also communicate beyond the bond market what a particular company’s ESG aspirations are, an increasingly important marketing tool in all industries.

“Conceptually, SLBs open the door more widely to certain sectors in industries that need to transition,” said Viola Lutz, head of climate solutions for ISS ESG. “Where the company is on a pathway to greening and that pathway is credible, it’s good to show where you want to be headed.”

Top firms expanding

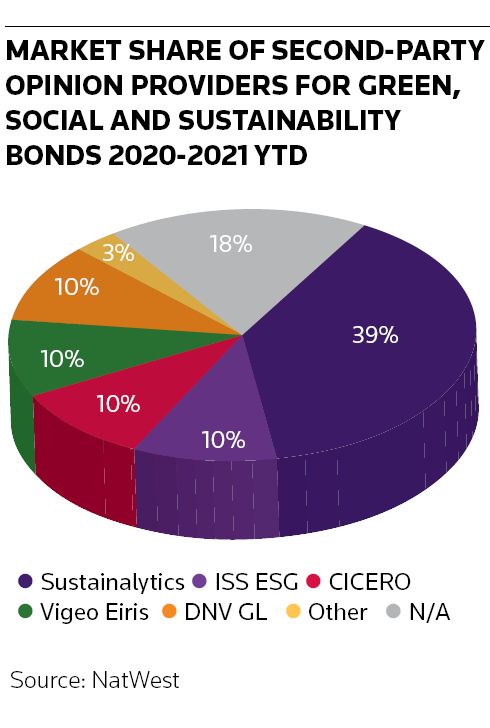

While there are already a number of established opinion providers (see chart), market participants say that there is plenty of room for more as the industry continues to evolve.

MSCI, which already provides ESG ratings and research on top of its popular related debt indices, is preparing to enter the market for second-party opinions and will bring its ESG index expertise to bear when it begins evaluating green and social bonds and loans initially.

"There is increased demand for [second-party opinions], and it's in line with what we're doing on our green bond eligibility work. So we think it's relatively natural for us to do that," said Remy Briand, head of ESG at MSCI.

S&P launched second-party opinions in 2017 with its Green Evaluation service and added framework alignment opinions for green and sustainable bonds at the end of 2020. In September, it is planning to start providing framework alignment opinions for sustainability-linked loans and bonds, which will include assessing the relevance and ambition of KPI targets and the quality of companies' disclosure and reporting.

"We are extending the alignment opinion to sustainability-linked and are further building out our offering across sustainable finance," said Hans Wright, head of analytical innovation at S&P.

Sustainalytics, meanwhile, has almost tripled the size of its second-party opinion team this year, from about 25 to 70 people, to meet increased demands.

“We’ve been in this space since late 2014, and of the roughly 750 SPOs we’ve done since then, about 400 have been done since 2020 alone,” Lang said.

None of this means that opinion providers have the final word on the viability of social or environmental targets in a bond or a loan. All market participants have to do the work for the industry to function, bankers said.

“Investors still have a responsibility to do their own research, and one of the important parts of this market is disclosure and transparency,” said Anne van Riel, head of sustainable finance capital markets at BNP Paribas. “I don’t think SPOs are the only thing investors rely on to make decisions. They provide another opinion, but not the only one.”

Additional reporting by Tessa Walsh