This year’s deal-making frenzy has led to a marked uptick in a bespoke and risky type of derivative that private equity firms, SPAC issuers and other companies use to hedge their currency exposures on cross-border acquisitions.

Barclays, Deutsche Bank and Goldman Sachs are among the banks at the forefront of the boom in deal-contingent options, contracts designed to protect acquirers against adverse currency moves between the date an acquisition is announced and when it closes. The most valuable feature for acquirers (and the diciest part for the banks selling these derivatives) is that if the M&A deal fails, the acquirer walks away without paying.

The global pandemic showed how perilous this business can be after a number of M&A transactions collapsed unexpectedly, leaving banks that had sold these contracts vulnerable. But that experience hasn’t deterred many from competing aggressively to win these trades in recent months amid a flurry of cross-border acquisitions.

“We’ve seen a lot of deal-contingent trades coming through the market driven by M&A activity and SPAC activity,” said Russell Lascala, head of FX trading at Deutsche Bank, who estimated volumes of these options are running at roughly double their 2019 levels this year.

“Spread compression is happening for sure as there seem to be more participants taking on deal-contingent risk. It’s a risky business, but it fits right into our sleeve of expertise in derivatives," he added.

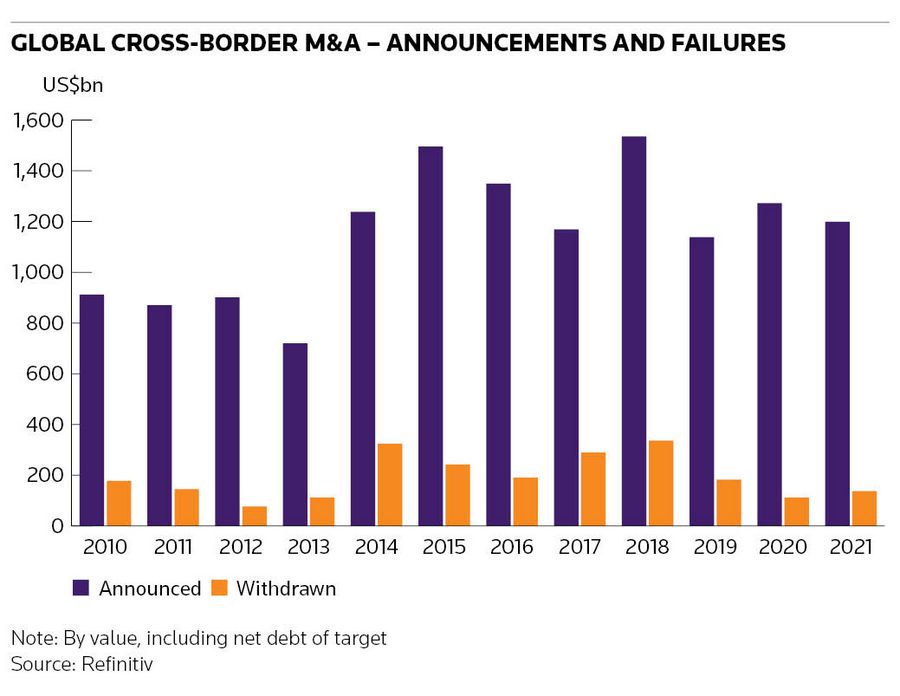

Cross-border deal-making has risen sharply in 2021 as acquirers and companies have looked to deploy cash piles amid greater certainty over the path of the pandemic. Nearly 10,000 such transactions worth US$1.2trn had been announced by mid-August, according to Refinitiv data, already surpassing 2019’s full-year total by value. That includes a record-breaking year for PE deals, the most frequent users of deal-contingent options.

The consequent upswing in deal-contingent hedging is providing a welcome bright spot for banks’ FX desks, which have otherwise had a quiet year due to low volatility and depressed trading volumes. A number of banks, including Barclays, Citigroup and Jefferies have ramped up their presence in deal contingents this year, sources say.

That contrasts starkly with the middle of last year, when the pandemic sent shockwaves through these markets. Covid-19 presented the ultimate wildcard for deal-contingent trades: an unprecedented and fast-moving situation that had the potential to disrupt almost any cross-border merger.

PE firms ditched acquisitions, leaving banks that had sold contingent options surveying their positions nervously.

“Certain sponsors pulled out of transactions and that made banks very nervous,” said Mark Beaumont, head of risk management for Europe at consultancy PMC Treasury. “Most banks paused as they’d suddenly encountered this tail risk in the global pandemic and wanted to understand more about how it affected M&A. We definitely saw a retrenchment in risk appetite."

War stories

Most banks active in deal contingents have war stories to tell about deals failing, leaving them exposed on the derivative they had agreed (but ultimately weren't paid for). But details rarely come to light publicly given that these contracts are struck in private and those stories stay off the record.

Disentangling exactly what happened is complex given the scale of a bank’s losses (or gains) will depend on how currencies have moved over the timeframe involved and how active the bank's traders were in hedging the risk on the option.

But The Carlyle Group’s proposed takeover of Vectura, the UK inhaler maker, provides a recent example of the potential risk-management headaches these derivatives can pose – particularly in more public deals. Barclays provided a deal contingent hedge for Carlyle’s initial offer in May to purchase Vectura for 136p a share, according to sources familiar with the matter.

The US PE group subsequently became embroiled in a bidding war with cigarette maker Philip Morris, leading Carlyle to up its offer to 155p a share. It is not clear whether Barclays was obliged to cover any counter bids from Carlyle, but such terms are not uncommon in deal contingents, bankers say. In the end, Vectura's board recommended the company's shareholders accept a higher counteroffer from Philip Morris, valuing Vectura at over £1bn. Barclays declined to comment.

Certainly, bankers involved in deal contingents make no bones about the perils of this business.

“This is a tail-risk product and we are always conscious of that risk,” said a senior banker. “We continue to participate in this market because we like this risk when we understand the transactions.”

Lingering caution

PMC’s Beaumont points to some signs of lingering caution among banks in the deal-contingent space following the events of the past year. His firm has seen more pushback on deal terms from banks when brokering these options on behalf of PE clients.

Larger M&A deals have also proved a challenge, as average transaction sizes have increased to US$123m this year versus US$92m in the prior five years. Parcelling the risk out to more than one bank has become more commonplace as a result.

"Deals getting larger presents challenges in the deal-contingent space. You need more banking capacity. There's a higher volume to get done," said Beaumont.

But none of that has stopped prices of these derivatives returning near to pre-pandemic levels. Deal contingent premiums – which are typically quoted as a percentage of the cost of a regular FX option – have decreased to between 20% and 25% of the equivalent option (or even below that range in some cases) in the fiercely competitive market for PE-led deals.

In the most widely used type of structure, the deal contingent premium gets added on top of the forward FX rate to account for the extra leeway the client has to walk away from the hedge if the deal collapses. So the lower the premium, the cheaper the hedge. (The premium is only a fraction of the cost of a regular FX option because the acquirer can only drop out of the contract if the underlying deal falls through.)

For instance, if the euro-US dollar three-month forward is currently trading at US$1.1700 and the deal-contingent premium equates to 20bp, a US entity buying a European company would buy the requisite amount of euros at a rate of US$1.1720 when the deal closes.

The compression in prices is all the more noteworthy for coming against the backdrop of so much deal supply – and not just from regular users of these derivatives.

The deluge of special purpose acquisition companies issuance in the first half of the year has spawned another source of demand for these hedges, bankers say. SPACs have announced US$142bn of cross-border transactions already this year, nearly 20 times more than across the whole of 2019.

Cov-lite

Despite reports of some banks becoming more discerning, others warn that deal-contingent contracts are getting done with fewer protections. That generally means giving acquirers greater leeway to change the terms of their proposed acquisitions, while still being able to keep their deal-contingent hedge in place.

“The deal-contingent market has become very cov-lite,” said the senior banker. “The protections that banks have around any unforeseen amendments to a transaction are very weak. That is a concern for us.”

Historically, banks have taken comfort from the fact that PE firms are professional investors that are heavily incentivised to get deals over the line, explaining why this part of the market is generally far more competitive than contingent options on corporate M&A.

Failure rates for PE deals averaged about 10% in the decade leading up to the pandemic, compared with 19% for corporate cross-border deals. Despite the headlines, Refinitiv data show only 4% of PE-led deals fell through last year, while the failure rate so far in 2021 is 13%.

Still, industry insiders see challenges ahead for bank underwriters – and not just in the form of too much money chasing too few assets. Many express concern about signs of creeping protectionism from Western governments in more sectors of the economy.

“In the current regulatory environment we're seeing governments take a more active role in the M&A process. That makes the deal-contingent space more challenging for banks to navigate,” said Amol Dhargalkar, global head of corporates at consultancy Chatham Financial.

“Banks really need to take a ‘portfolio effect’ approach, which can weather the ups and downs of this market. They can’t just go in and do one or two of these transactions," he added.