The electronification of corporate bond trading has increased significantly this year despite a decline in turnover across the wider market, in the latest sign of a structural shift in credit trading towards a more equity-like world where technological prowess dominates.

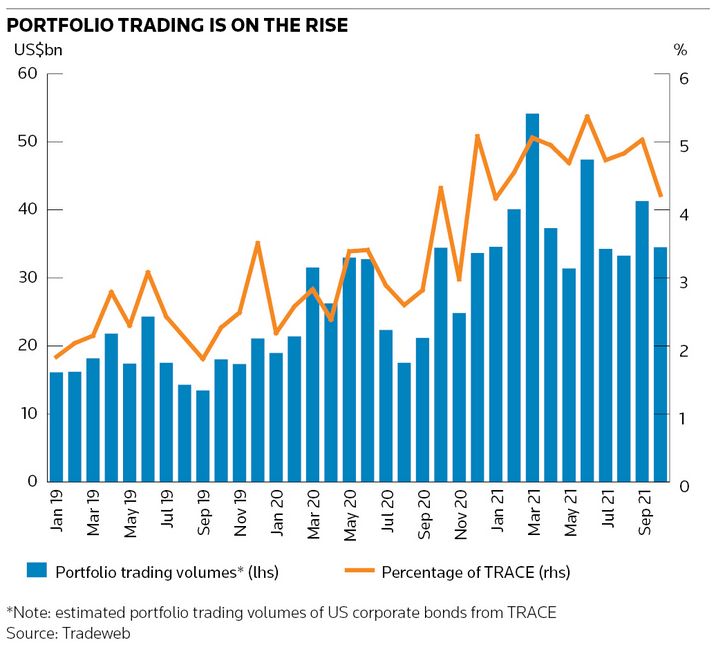

Portfolio trades in US corporate bond markets rose 50% in the first 10 months of the year to US$388bn, according to estimates from Tradeweb, in one prominent example of how algorithm-driven activity has jumped. Portfolio trades represented almost 5% of total volumes during that period compared to 3% in 2020, despite a roughly 8% drop in overall bond trading volumes this year.

The growing use of algorithms to price securities at lightning speed is sparking a technological arms race among the top traders – mainly banks – competing in this space as they battle to secure an edge in the emerging environment. Executives believe the face of credit markets is changing for good with the adoption of the greater automation seen in equities trading – a move that ultimately served to compress profit margins in that market and concentrate activity among the biggest players.

"The evolution of the credit business continues apace with the shift towards electronification," said Rehan Latif, head of credit trading and sales for EMEA and global emerging markets trading at Morgan Stanley, who said about 70% of the firm's investment-grade tickets now go through its algo.

Latif drew parallels to banks’ equity trading units, where flow businesses typically produce lower returns compared to more profitable activities such as selling structured products and providing financing, but are necessary to keep in touch with clients.

“It’s not a high margin business, but it gives you relevance in front of clients and enables you to become a one-stop shop for CIOs. If you’re one of the top players in flow, it allows you to percolate through to less liquid credit where clients are increasingly going to get yield," he added.

Equity mentality

The electronification of corporate bond markets has picked up pace over the past two years with portfolio trading becoming a particular buzzword. That is where trading desks use algorithms to price hundreds of bonds in the space of an hour, sometimes totalling over US$1bn, and at a cheaper price than executing a series of individual trades over a day or so.

The related activity of algo trading, where computers price odd lots of bonds almost instantaneously, is also allowing banks to trade greater volumes of small-ticket transactions. Meanwhile, some bankers believe bringing fixed-income exchange-traded funds onto credit desks (from equity units where many were originally housed) is another important part of the puzzle allowing traders to recycle odd-lot positions in the "create and redeem" process by which ETFs accurately reflect the markets they are tracking.

Institutions at the forefront of these trends, such as Goldman Sachs and Morgan Stanley, were able to reap the rewards of their investments when credit markets whipsawed in 2020 following the outbreak of the pandemic. Trading volumes soared and credit markets stood up to the challenge, with electronic trading helping record amounts of turnover pass through these markets.

"Four to five years ago it was a completely foreign concept to say: ask me anything and I'll put a price on it for you," said Chris Bruner, head of US institutional fixed income at Tradeweb. "These new protocols like portfolio trading and all-to-all [where traders transact anonymously across markets] have increased the capacity of the market and have performed well during volatile environments."

Fierce competition

Competition for know-how in this space has become fierce. One bank had the traders overseeing its algo execution poached on four consecutive occasions last year.

Deutsche Bank is among those investing heavily to make up ground. Citigroup said it had made a number of “dramatic changes” to how its flow credit trading desk is set up, as well as to personnel, with the idea of becoming one of the top houses in algos, portfolio trading as well as the creation and redemption of credit ETFs.

“You can't just be one of the top banks in portfolio trading on a standalone basis. It’s a three-legged stool: you also need to be one of the top players in algorithmic trading and ETFs to close out the loop,” said Vikram Prasad, global head of flow credit trading Citigroup.

Tradeweb has said about 100 companies are now doing portfolio trades on its platform, over triple the number from a year ago. Bruner said a broader set of clients, such as large hedge funds, are getting involved, while the interdealer market is also developing.

Even so, this year’s decline in volatility and compression in bid-offer spreads has presented a more challenging backdrop for banks trading these markets. Ultra-thin margins have even led some traders to pore through publicly available records of bonds sales to establish whether rivals consistently undercutting them on price were able to make money on the portfolio trades.

Many believe these businesses will only get squeezed further as electronification becomes more prevalent.

"Fixed income is evolving and electronification is gathering pace," said Manav Gupta, head of credit flow trading at Deutsche Bank. "The investment you need is substantial. Technology is now your edge and the focus has to be on building an underlying platform that makes the business sustainable in the medium term."