When Atletico Madrid were crowned Spanish champions at the end of May, it was a bittersweet moment for the club. On the pitch, the triumph was certainly a major feat: for only the second time since 2002, the Colchoneros had broken the stranglehold that bigger rivals Real Madrid and Barcelona had held over Spain’s top league. Supporters started to dream that the triumph might even herald a new golden age for the club.

But success had come at a heavy price. While big-name signings such as Diego Costa, Joao Felix and Antoine Griezmann had undoubtedly transformed Atletico’s game, they also left the club with a wage bill that had quadrupled over the course of just seven seasons. A new stadium on the outskirts of the Spanish capital, which lay empty during the whole of last season due to coronavirus restrictions, had also become a huge drain on Atletico's finances.

As well as being Spanish champions, the club lays claims to another, more ignominious title: being one of the most indebted football clubs in the world, with liabilities fast approaching €1bn. At the same time the team was enjoying success on the pitch last season, its chief executive Miguel Angel Gil was locked in talks with the private equity arm of US asset manager Ares Management to secure a lifeline for the club. Just days after sealing the title, Atletico announced a deal with the investor group to raise more than €180m.

For Gil, whose father bought the club in the 1990s in a controversial leveraged buyout that was later investigated for fraud and misappropriation, bringing in outside money to get the club out of a tricky financial spot was nothing new. Chinese real estate tycoon Wang Jianlin bought a 20% stake in the club as part of a capital raise in 2015. Three years later, Wang sold out to Israeli shipping magnate Idan Ofer, who increased his stake to one-third as part of another capital raise.

But the deal with Ares is different and reflects a big shift in European football, as the age of the billionaire club-owner gives way to a wave of private equity money rushing into the sport.

Over the past year or so, around a dozen clubs – including Manchester City, Genoa, Inter Milan and Club Brugge – have struck deals with predominantly US investors. Dozens more have borrowed from private debt funds.

For the PE shops, the appeal is clear. “We are attracted by the demand for content that we’re seeing across football – particularly the value of that content – as well as the sport’s secular growth, which has continued to increase over the last 10–15 years, pretty much unabated,” said Mark Affolter, a partner at Ares who helped negotiate the Atletico deal. “Atletico valued the fact that we could bring flexible, scalable capital into the equation to help drive some of their growth initiatives.”

Position of weakness

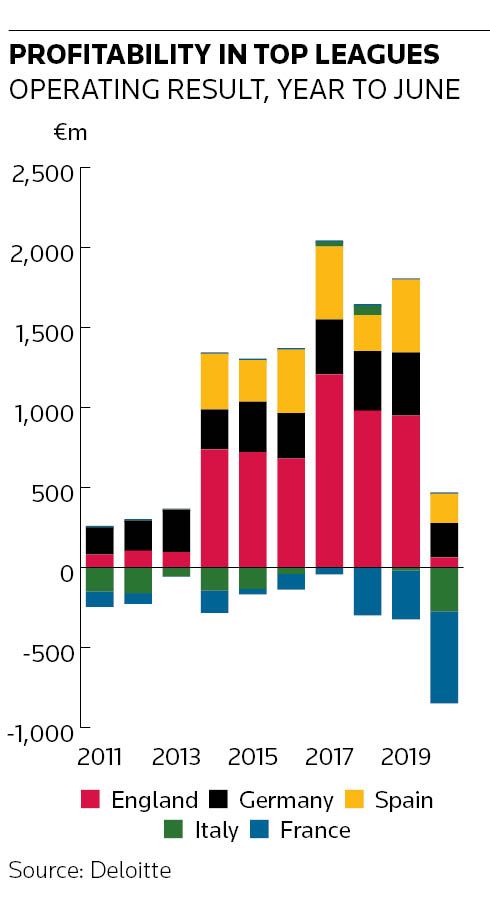

While the arrival of new money could unlock potential, one thing that almost all these deals have in common is that they were negotiated with the clubs in a position of weakness. The pandemic has ravaged football finances – European governing body UEFA estimates lost revenue at around €9bn last season. That in turn has left many heavily indebted clubs in actual or potential breach of covenants to their lenders, forcing them to hunt for fresh capital to keep their banks and bondholders at bay.

That weakness was the main reason why earlier this year so many of Europe's biggest clubs were so keen to join the European Super League, a JP Morgan-funded proposed breakaway competition that promised hundreds of millions of euros of extra revenues to the continent’s top clubs, but was predicated on ditching promotion and relegation, a long-standing tradition central to the European game. After a backlash from fans, the competition was abandoned. But some clubs haven't entirely given up on the idea.

“Two things have happened as a result of the pandemic,” said Greg Carey, who oversees sports financing at Goldman Sachs and helped put together a €595m private debt deal for Barcelona that restructured old debts after the club breached covenants.

“First of all, a lot of big stadium projects have been pushed back and delayed, and that’s meant increased costs and delayed revenues for clubs that are basically fully leveraged. At the same time, you’ve seen a breakdown in some of the traditional funding mechanisms that many of these clubs have relied on," he said.

Just over a year ago, for example, 23 Capital – a prominent lender to clubs in Europe – suddenly stopped lending and began winding down its US$1bn loan book. “Some of the niche providers have pulled back, and the commercial banks have largely stopped lending. That has created a gap for the private capital guys to fill,” Carey said.

UEFA president Aleksander Ceferin has warned that the sport is facing “a new financial reality” as a result of the pandemic. And it isn’t just clubs that are turning to private capital to bail them out: entire leagues are striking deals. CVC Capital Partners struck a €2.2bn deal in August to invest in Spain's La Liga, a year after it tried to do a similar deal with the Serie A league in Italy that was ultimately rejected by clubs who feared losing control to US investors.

TPG Capital tried to do a similar deal with the English Football League linked to the Championship division, only for talks to fail. Germany has also been a target: authorities there explored selling a minority interest in new companies linked to the country’s top two Bundesliga divisions, only to dump the idea after an outcry.

“Covid-19 was probably a bit of a catalyst to a trend that was already underway and was likely to take hold anyway,” said Affolter at Ares. “Unlocking potential requires more creative thinking in terms of capital structures. And so I think it was somewhat inevitable that you would see flexible, scalable, creative capital coming into European football and sports generally.”

Misplaced comfort

While some of the deals linked to the leagues have been met with considerable resistance, what is perhaps remarkable about the club deals is how private equity has been welcomed with little debate. Fans often have an ability to look the other way when it comes to new investors promising money to spend on star players. Fans and administrators have also taken comfort from the seemingly small share of individual clubs being sold to PE shops.

But that comfort may be misplaced. Hidden in the terms of many of these deals are conditions that give minority investors huge power over clubs. When Silver Lake bought US$500m of preferred shares in 2019 in City Football Group – the owner of Manchester City – auditors concluded that the deal should have been classified as debt because the terms allowed the PE firm to sell back the 10% stake if certain conditions weren’t met by 2030.

Carey believes such protections are understandable, given the unpredictable nature of European football, where relegation is always a possibility – unlike the closed leagues in the US. Teams can easily enter a downward spiral, where relegation begets financial troubles that in turn beget further difficulties on the pitch. While parachute payments help a relegated team, going down even one division can mean losing a huge proportion of a club's income.

“Every deal is different, but for sure there are protections in place,” he said. “If certain things don't happen, they have certain rights to play in the capital structure. Most of these investments are minority investments. In the US, you can rely on the league to make sure obligations are paid. But in Europe, you can't, so I'm sure they have certain financial covenants that have to be met. Otherwise they get more rights.”

The deal struck by Barcelona in summer is a case in point. The €595m debt deal provides the club with much-needed cash but has also cast a sword of Damocles over the club: if it doesn’t manage to reduce debt to four times Ebitda by mid-2025 (it expects to make a loss again this season), the debt will be downgraded, giving its 12 lenders control over the club’s TV rights money, which makes up a third of its income.

Meeting that target will require deep cost cuts and the abandonment of a deep-pockets strategy that has made the club one of the best in the world. The long-term interests of lenders are protected, but what about those of the club?

Upside potential

Some investors were certainly inspired by the turnaround at AC Milan, where a recipe of financial discipline and fresh capital seems to be working well. Elliott Management took control of the club three years ago after Chinese owner Li Yonghong defaulted on a loan. Since then, the US distressed debt-cum-PE house has cut costs and embarked on a long-term growth plan. Last season, the club had its best performance in a decade, finishing second in Serie A.

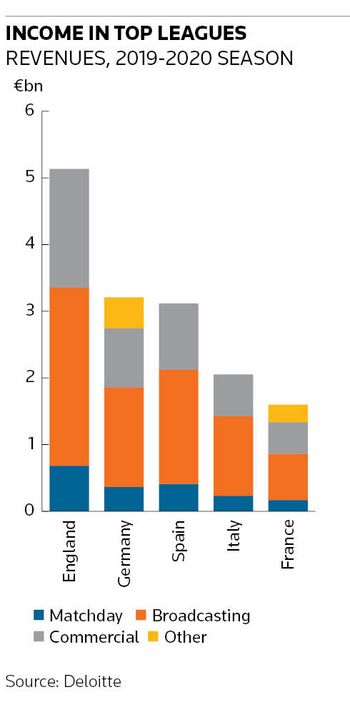

Like Elliott, recent PE entrants see huge upside in European football clubs, which they say are dramatically undervalued compared to US sports franchises. Part of that is down to financial mismanagement: revenues in the top five European leagues roughly doubled in the decade to the end of the 2019 season, as a result of ever-growing TV rights and sponsorship deals. But in most cases as fast as the extra money came in, it was spent on surging player wages and transfer fees.

And while private equity is notorious for cutting costs and selling out, with football the strategy seems to be around extracting more revenue from the fans. Many see huge potential in the way that content is delivered to fans – from streaming services to artificial reality experiences and even new competitions with lucrative TV contracts. Over time, they hope to see a revaluation in European football clubs – just as has happened in the US over the last two decades.

Investors are also keenly aware that sport in general – and football in particular – retains an "appointment to view" (and therefore to consume advertising) status that has all but disappeared elsewhere as streaming entertainment has taken over. Clubs also attract a loyalty that is unmatched by any other form of mass entertainment.

“Why are these teams [in the US] worth 10 or 20 times what they were worth back in the 2000s?” asked Jesse Du Bey, a partner at Orkila Capital, which bought a minority stake in Belgium's Club Brugge earlier this year. “Yes, they're scarce assets. But the real reason is because of the very rapid monetisation of their intellectual property. There’s been a lot of commercialisation – of streaming, of near-live, brand rights across merchandising, in-stadium and out-of-stadium.”

“Why are these teams [in the US] worth 10 or 20 times what they were worth back in the 2000s?” asked Jesse Du Bey, a partner at Orkila Capital, which bought a minority stake in Belgium's Club Brugge earlier this year. “Yes, they're scarce assets. But the real reason is because of the very rapid monetisation of their intellectual property. There’s been a lot of commercialisation – of streaming, of near-live, brand rights across merchandising, in-stadium and out-of-stadium.”

Orkila bought a 23% stake in the Belgian champions in July for €30m, following a failed attempt by its owners to list the club, and agreed to inject another €20m to strengthen the club and invest in new business initiatives. The deal came a year after Orkila bought a stake in the global Ironman franchise. Du Bey said that his pitch to the Brugge owners was the potential to expand the business side in a way that elevated the brand as well, just as they had with Ironman.

“The forcing function of institutional capital more than anything else is to align stakeholder incentives,” he said. “One of the most important lessons from the pandemic is that, if you don't have that kind of alignment, it's really bad for everybody in the long term. It might feel good to say that sport is the most important thing, but you can put yourself into a situation where very quickly you're in a crisis and then you need to turn to others for help and you risk losing the real soul.

“I think alignment and understanding that economic sustainability – which doesn't mean maximising profit – must be the highest goal if you are going to be successful on the pitch.”

Financial discipline

Instilling a bit of financial discipline is long overdue, some believe, in a sport that has for too long been allowed to operate in a financially unsustainable way. Successive waves of club owners – from the local businessmen looking to secure glory for the clubs they grew up with, to the foreign owners looking for trophy assets, and then to those wanting to sports-wash their source of wealth – have imbued a culture of financial profligacy.

“If we take a look at the Championship, in seven years out of the last eight, wages have exceeded revenues – and in the one year that they didn’t, they were 99% of revenues,” said Kieran Maguire, a football finance lecturer at the University of Liverpool. “That’s no way to run a business. It's effectively casino-style management whereby you are putting all of your money onto the shoulders of a 23-year-old professional athlete. It’s a spectacularly dumb model.

“If you are private equity, and you come in, the only way that you're going to do it is if you can extract value-added from the playing side of the club. Now we've seen Liverpool who are using a data-driven recruitment-and-retention [aka "Moneyball"] model. We've seen that at [recently promoted to the Premier League club] Brentford. The smart people – and there's plenty of smart people in private equity – are saying: ‘we are up against old-school cultures on an operational level in football, we need to look at a more Moneyball approach’.”

Local communities

The question that follows, though, is how the presence of that "smart money" might change the entire culture of clubs steeped in more than a century of history and tradition.

The debacle over the European Super League is a reminder of the politics of European football, which for all its global appeal and commercial success, remains deeply attached to the local communities where those teams were founded many years ago.

“Football in [England] in particular is welded into the fabric of society,” said Maguire, adding that the game may soon be close to a tipping point, where clubs backed by private capital or professional investors may soon have the majority they need to start changing rules to make the sport even more lucrative. “From a financial point of view, it's going to come because of the pressure from investors,” he said.

In England, the government – mindful of the outcry over the European Super League – is considering how to balance the commercial success and pull of the Premier League, one of the country’s greatest exports, and the communities that have grown up with teams in that league. Tracey Crouch, the MP overseeing the review, has warned that football clubs are not ordinary businesses, highlighting their critical social, civic and cultural role.

Atletico shareholder Ares believes that the private capital push into the sport can generate positive returns for all stakeholders. Putting these clubs on a stronger financial footing will mean they are here for another century or more.

“I think this can be a good thing for all constituents – including fans – because driving commercial revenue can provide greater liquidity and capital to the clubs that they can invest on the pitch, in operations or the stadium experience,” said Affolter.