Opening new markets

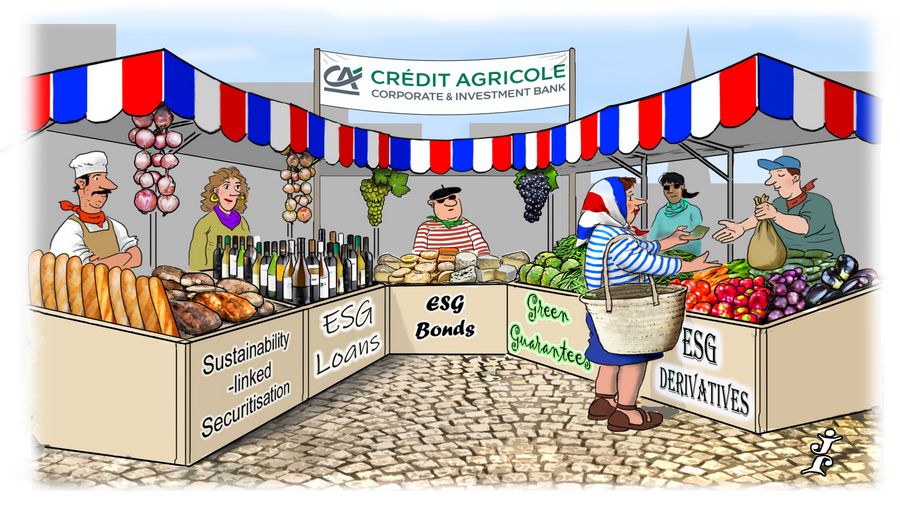

A top-tier global player and innovator in labelled bonds and loans, as well as a pioneer in emerging fields like ESG derivatives and sustainability-linked securitisation, Credit Agricole is IFR’s ESG Financing House of the Year.

Credit Agricole is a European bank but it has a much wider presence when it comes to ESG financing.

Its global reach is underscored by its two key transactions of 2021. One – Ford Motor’s US$15.5bn revolving credit facility, the largest sustainability-linked financing ever and IFR’s North America Loan of the Year – came in the US. The other – the European Union’s €12bn 15-year and IFR's Sustainable Bond of the Year – came closer to home. But the bank was also responsible for landmark loan and derivatives deals in Latin America and Asia.

Among the latter was the first sovereign sustainable Formosa bond. The bond – for Chile, IFR’s Sustainable Issuer of the Year – was among a raft of CA innovations over the year. Others included the first bank sustainability-linked bond, the first SLB from the oil and gas sector and the first corporate social hybrid bond.

CA also helped accelerate new products such as sustainability-linked securitisation and green guarantees, as well as contributing strongly to the emergence of ESG derivatives.

“The angle that we want to keep on pushing is to make sure that all products within the investment bank – not only financing, but swaps and any type of transaction that we can offer – can be available in sustainable finance format,” said Tanguy Claquin, the bank's global head of sustainability.

In tandem with strong underlying growth in ESG markets, this effort to extend the market enabled the bank to more than double its sustainable finance revenues in 2021, according to Claquin.

Besides its league table leadership (third in labelled bonds by 2021 volume and first for green and sustainability-linked loans), another important measure of CA’s standing in ESG financing could be termed the credibility ratio. It is unique among leading banks in having arranged more green funding (US$61bn) than fossil fuel funding (US$51bn) since the Paris Agreement on climate change in 2016.

Sovereign adviser

In what some called “the year of the sovereign” in green bonds, with Germany’s arrival the previous September galvanising Italy, Spain and the UK, plus the EU, into the market, CA’s leadership in SSA ESG was at a premium.

It was structuring adviser to both Mediterranean sovereigns, as well as informal adviser on the EU framework under which the super-sovereign will issue an unprecedented €250bn of green bonds (Brussels appointed no formal advisers). It was also a bookrunner on inaugural green benchmarks from all three.

In addition, CA was the only lead manager that Italy retained from its original €8.5bn green BTP when the issuer added another €5bn to the 2045 issue in October.

The bank was also joint bookrunner on France’s second OAT verte, a €7bn 23-year; joint bookrunner of Andorra’s debut €500m 10-year sustainable bond; and sole sustainability adviser on Slovenia’s inaugural €1bn 10-year sustainability bond.

“We've basically been involved in almost all European sovereign issues,” said Laurent Adoult, head of sustainable banking for SSA and FIG in Europe.

CA was active for sovereigns beyond the eurozone. Besides Chile’s US$1.5bn 32-year, which marked the Taiwanese market’s lowest coupon on any sovereign offering (3.50%), it was joint green structuring bank and global coordinator on a raft of issues under Hong Kong SAR’s green global MTN programme, a sovereign first. These comprised US$2.5bn of five, 10 and 30-year bonds, €1.75bn of five and 20-year bonds, US$1bn of 10-year bonds, and Rmb5bn (US$786m) of three and five-year Dim Sum bonds.

It was also joint bookrunner on South Korea’s €700m five-year green bond.

FIG first

A key CA innovation during the year was structuring the first – and to date, only – sustainability-linked bond for a financial issuer. While regulators’ unwillingness to treat a credit-sensitive product like an SLB as eligible for meeting banks’ minimum requirement for own funds and eligible liabilities, issuer Berlin Hyp did not require MREL credit for the €500m senior preferred transaction.

The 10-year deal offers its 70-plus investors a step-up on its final coupon if Berlin Hyp fails to reduce its loan portfolio’s carbon intensity by 40% by December 2030. The target forms part of the mortgage bank’s goal of achieving carbon neutrality by 2050.

CA was sole SLB structuring adviser.

“It's quite an achievement to see a bank managing to come up with an SLB transaction, given the difficulties that you have to authenticate its carbon footprint,” said Adoult.

Germany was the source of a second FIG landmark when CA was sole green structurer for the first green Tier 2 bond from a German bank. The €500m 10.25-year non-call 5.25 subordinated deal, which funds solar and wind energy project loans, was for BayernLB.

The bank also brought Axa’s first green Tier 2 offering, serving as co-global coordinator and co-green structuring adviser.

In addition, it was sustainability structuring adviser to BTG Pactual, the first private Latin American bank to issue a cross-border green bond, and joint bookrunner on the US$500m five-year that inaugurated its framework.

Corporate triumphs

Across its bond and loan franchises, CA racked up a host of notable corporate transactions. Besides the Ford SLL, where it was lead sustainability structuring agent, its transport practice included working as green structuring agent and guarantee provider on China’s first internationally rated green asset-backed security – a Rmb1.73bn issue for BYD Group.

In another key sector, energy, its highlights were headed by the landmark first oil and gas SLB. The €1bn seven-year for Eni was linked to the company’s renewables capacity and emissions, including Scope 3. It also arranged a groundbreaking €615m sustainability-linked guarantee that extended Enel’s use of SL structures even further, as well as the first social hybrid – a €1.25bn perpetual non-call seven for EDF in May that supports the utility’s SME suppliers through sustainable procurement.

It was global coordinator and structuring adviser on a €750m green perpetual non-call 10-year hybrid for Engie.

Also in SLLs, it was sustainability structuring agent for US$3.6875bn of RCF and term loan A debt that placed Micron Technology among the five biggest US SLL issuers at launch.

It put significant emphasis on extending ESG financing beyond blue-chip names to SMEs. Mostly in France so far, highlights included an €85m ESG-linked securitisation for agri-food group Fleury Michon and a €165m sustainability-linked Schuldschein for cooperative Agrial, as well as sustainability-linked acquisition financing and other loans.

Finally, CA was ESG structurer for Edenred’s landmark €400m sustainability-linked convertible bond.

Derivatives thrust

One notable area of activity has been the bank’s strong push in the emerging field of ESG derivatives. “Clearly we are the benchmark,” said Claquin, who terms the area “a young market where we need to define what are the absolute best practices”.

CA's role was underscored by signing a unique agreement on sustainability-linked foreign exchange derivatives with Enel. At the start of the year the pioneering issuer of sustainability-linked bonds, loans and commercial paper put a landmark ISDA framework in place to link its short-term forex derivative transactions with CA to its long-term sustainability targets. A sustainability premium on options, forwards and swaps transfers to Enel if it achieves its KPIs.

Italy provided other ESG derivatives breakthroughs. CA traded the luxury goods sector’s first deal of this sort – a €40m sustainability-linked interest rate swap – as well as a green-labelled swap on a €500m inaugural green covered bond. It also provided a green-labelled cross-currency swap on a Norwegian bank’s green covered bond of the same size.

Having traded Asia’s first ESG derivative with a Hong Kong logistics corporate in October 2020, it followed up by tailoring the coupon on a Hong Kong company’s HK$375m (US$59m) sustainable financing. It also traded the first Singapore dollar ESG derivative – a S$24m (US$18m) three-year sustainability-linked interest rate swap.

Other highlights included an €85m charity-linked interest rate swap for a Spanish telecoms company with a donation to a nominated cause if KPIs are missed, and a hefty £147m green-labelled interest rate swap and cap for a UK real estate company.

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com