IFR Asia: India’s debt markets have weathered their fair share of challenges over the past few years. Long before the coronavirus began spreading, a string of defaults from non-bank lenders had sapped confidence in the financial sector. In the past year, the Reserve Bank of India has announced unprecedented measures amid the pandemic to ensure smooth flow of capital to corporates.

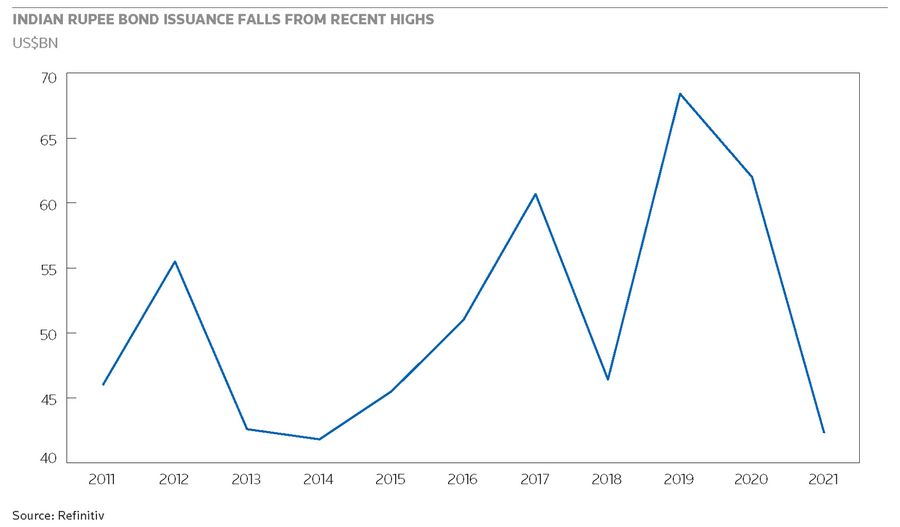

While a strong policy response to the pandemic protected India from a full-blown financial crisis, it also delayed further reforms designed to reduce the economy’s dependence on its creaking state banks. The domestic bond market has seen muted growth as lower-rated corporates are still unable to access the debt capital market to raise funds. Although there is a national push towards green and renewable energy, we have hardly seen any ESG issuance in the domestic bond market.

Rates are also expected to rise globally. Prasanna, how will rising rates affect the Indian market?

Prasanna Balachander, ICICI Bank: As most investors will know, the global scenario is at an inflection point where growth is peaking out, and inflation is persistently high.

Globally, the market has been repricing interest rate expectations. There’s been a lot of talk about taper tantrum and its implications for the market, but we have crossed the taper announcement without much tantrum – and credit is due to the central banks for telegraphing it properly.

What is happening now is a repricing of interest rate expectations post the taper. In addition, emerging market currencies are at risk of underperformance as more people realise that strength in the dollar will make the carry trade less profitable, and so money is moving back to the US. That’s a global scenario very quickly.

In India, the outlook for growth is positive, as the multi-year revival of many industries has started. For inflation, we are looking at something around 5% for this year and very close to 6% for the next 12 months. Broadly, the macro outlook is getting a little bit weaker. Growth will be very good for India, but the current account deficit is worsening, and the balance of payments is also getting incrementally weaker. This all has implications on policy rates.

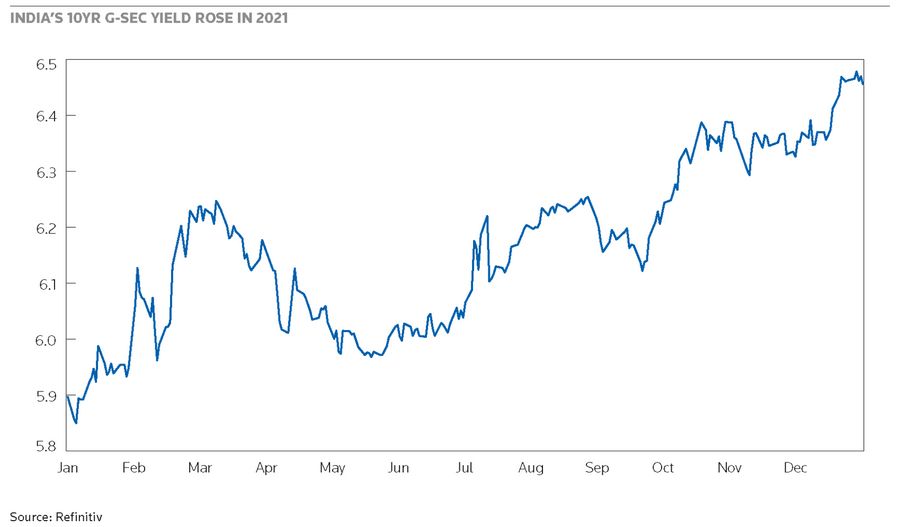

We feel that the interest rate cycle has clearly bottomed out and we are set for a gradual rise in rates.

From an issuer perspective, we expect rates to rise quicker at the short end of the curve in India as this is where they fell most when Covid started – we saw interest rates falling by as much as 400 basis points. The trend is going to reverse, and short-term rates have already reacted quite a bit.

A bear-flattening theme will play out with short-term yields going up further than at the long end. Yields are going to be higher and liquidity is getting tighter under the influence of RBI activity and so corporates are looking at longer-dated tenors at this point of the bond market cycle. And when liquidity gets sucked out, credit spreads also increase.

Borrowers obviously want to lock in low interest rates for as long a period as possible, so they are looking to issue in the five to 10-year segment of the curve. On the other hand, as interest rates begin to rise, investors are putting more money into floating-rate issuance or floating-rate schemes of mutual funds. They are attracting substantial amounts of money.

In terms of the type of issuance, the financial sector has dominated for the last decade and I think that will continue, particularly given the impact of the non-banking financial company (NBFC) crisis of 2017/18, which saw investors turn towards safer, top-rated issues.

Nevertheless, in the last year we have seen more and more sectors open up for issuers. We have seen supply coming from areas like telecom, renewable energy, and autos.

I think one of the most important recent developments is the appearance of Infrastructure Investment Trusts (InvIT) and Real Estate Investment Trusts (REIT), in national infrastructure pipeline, and the government has the also set very aggressive targets for the national monetisation pipeline of almost Rs5trn over the next three or four years and Rs800bn in the first year.

I think it’s going to be a very different market next year to the one we saw last year but nevertheless a very active one. Corporate India will have to grapple with rising interest rates and adapt balance sheets and cashflow requirements accordingly. We’ll see new and different issuance structures come to the market – floating-rate bonds linked to external benchmarks, for instance, have been increasing.

IFR Asia: We see Indian corporates finding it easier to access the offshore dollar bond market. What are the constraints for large borrowers in accessing the domestic capital market? Are foreign portfolio investment rules for investing in rupee debt favourable?

Seshagiri Rao, JSW Steel: Post-Covid, due to the policies pursued by the RBI, enough liquidity has been created in the market and interest rates have gone down. At the same time, when we wanted to achieve GDP growth of 8% to 9% in the past, then we’ve needed credit growth of up to two and a half times those numbers.

So, in the current year, if we estimate 9% as our GDP growth then credit growth will be in the range of 17% to 20%. That is not happening in the market, so corporates are looking at alternative sources of raising funds.

Lending by local domestic banks is sluggish. There is a disconnect. Banks say that corporates are not approaching the banks for funding, whereas the corporates are saying they’re not getting funding from the banking sector.

If we look at the domestic bond market, then it is open for highly rated companies, either AA and above or the financial sector, and particularly at the long end of the curve.

There’s only a limited opportunity for lower-rated corporates to source domestic bonds for funding, so the good corporates are turning to the international markets for bond issuance.

There are limitations to sourcing funding overseas, however. There are restrictions on the use of funds, the total cost of funding, and from whom you can borrow. There is a list of lenders from whom you can borrow.

Over and above that, is the 5% to 10% tax collected at source, which must be grossed up and which the borrower must pay. That increases the cost of borrowing for Indian corporates.

Unless corporates are willing to raise money over 10 years-plus then the Indian restriction is there. If borrowing is less than 10 years, then funds can only be used for capital expansion. You can’t use them for any other purpose, including refinancing.

These restrictions limit the ability of Indian corporates raise money overseas, where funding is available.

As I mentioned, lending from domestic banks that used to fund 60% to 65% of Indian corporates is subdued. There should be somebody else to fill the gap, but foreign portfolio investors (FPI) only look at three-year funding. More than three years is not possible. There are other restrictions as well. For instance, if an Indian corporate wants to borrow offshore then there should be at least two FPIs, with only 50% of each issue held by one investor and only 30% of their portfolios can be held in bonds.

These are some of the issues that Indian corporates are facing when accessing new sources of funding. At the same time InvITs, which have become popular for, particularly, renewable energy companies and infrastructure companies, present a new source of funding.

But for other sectors, capital-intensive sectors like steel, for instance, these companies must raise funds from any available sources overseas through a bond, subject again to the constraints. Likewise the constraints on FPIs remain.

These constraints need to be looked at to ensure Indian corporates have access to funds at a competitive cost.

IFR Asia: What initiatives can be taken to develop the domestic debt capital markets and make it easier for corporates across the credit spectrum to access bonds?

Prasanna Balachander, ICICI Bank: The RBI’s response to the emergency Covid situation was mind-blowing and it played its part beautifully as, at the time, the markets were almost breaking down. The credit market was breaking down. Trust among the banks and corporates was falling.

Its actions really helped a lot of AA and AA-plus corporates raise substantial funds. The schemes employed are well past their sell-by date and I don’t think we’ll see such steps in the future.

However, a developed corporate bond market is essential. If GDP is going to reach US$5trn any time soon, it cannot happen without the corporate sector’s contribution and that cannot be achieved without a functioning corporate bond market.

We can quibble about the pace at which bond market development is happening, but the fixed income investor base has been growing quite substantially – especially mutual funds and insurance companies. They are a very important part of the development.

We have also introduced new investor classes over the last few years, like the National Pension Scheme, which have also helped in attracting long term savings.

Prior to Covid, due to a number of credit events, risk aversion had built up amongst investors. Regulators were also monitoring more carefully the types of investments run by market participants, and that also contributed to a reduced appetite for lower-rated corporates.

The role of regulators is of particular significance as we go forward. There are credit ratings issues for various investor segments, whether it is insurance companies or mutual funds or for employee provident fund organisations or for NPS schemes. The Pension Fund Regulatory and Development Authority (PFRDA), the regulator for the NPS, recently allowed NPS to invest in securities issued by REITs and InvITs.

There are various levels of ratings thresholds that a fund manager must meet before investing in any of these instruments so what I would like to see is the regulators being a little bit more large-hearted, giving more flexibility to investors to choose between ratings. If their own board approvals are well documented and they have a proper framework, they should be allowed to choose what ratings they want to invest in.

The second is a change in investor behaviour themselves. When we have seen the regulators giving investors flexibility, the investors themselves have chosen not to use that freedom. They are still hesitant to invest in anything which is below AAA.

For example, the Employees’ Provident Fund Organisation (EPFO) has recently discontinued investing in private corporate paper post-2018, even though they are allowed to buy up to 60% of their corpus up to the Double A rating.

EPFO is the biggest provident fund manager in the country and what it does has a lot of influence on the rest of the exempted PFs who look towards EPFO for guidance in terms of what they are doing. Anything the EPFO does has a multiplier effect on the rest of the provident fund investing community.

I would personally like to see investors take much more credit risk voluntarily, based on their own investment philosophies and principles, and see more money flowing towards the lower-rated corporates as well.

Development of a functioning credit default swap (CDS) market has been a personal dream of mine. We need to see the development of CDS and the interest rate futures market. These two instruments, together, will enable bundling and unbundling of interest rate risk and credit risk depending on what the investor wants. You could transfer the underlying risk of a security to an entity more willing to accept the credit or interest rate risk using the appropriate products.

The other thing which the RBI and the government could promote is retail participation. That would lead to a more active secondary market for retail and corporate bonds thereby giving issuers access to another viable source of consistent funding.

Some of the announcements the government has made, for example, in the budget, have far reaching consequences. They have set up the National Bank for Infrastructure Development, which is going to raise equity, leverage themselves up multiple times, give guarantees to road and other projects or even directly lend to them. Then you have the Credit Guarantee Enhancement Corporation which will help in lifting standalone ratings.

One problem is that investors are not going down the rating spectrum, so why not have an entity offering guarantees that helps bring ratings up. Guaranteed credits can then approach the market for funding.

The other thing that the budget talked about is the backstop facility, which is a direct consequence of the way corporate bonds initially behaved post-Covid when absolutely nobody was willing to lend to each other – people were really selling bonds at throwaway prices. A backstop facility would improve confidence in the long-term sustainability of a corporate bond market.

IFR Asia: Are Indian banks reaching their lending limits to big corporates? And will this lead to more corporate bond issuance in the domestic market?

Karthik Srinivasan, ICRA: If you look at the overall capitalisation levels of Indian banks, they are large. Are they hitting limits for group exposures? Possibly not. Over the last couple of years, there has been a sizeable infusion of capital into public sector banks and private sector banks have undertaken capital raising exercises. On top of that, corporates have been deleveraging.

Putting things into perspective, the reported net worth of the overall Indian banking sector is about Rs15 lakh crores (Rs15trn). The banking sector can take over Rs3 lakh crores (Rs3trn) towards a single group. That is a fairly large number.

We did have some issues a couple of years back when, as part of routine annual report disclosures, we saw some banks saying exposure to a particular entity or a particular group was very close to the regulated permissible limits. Nowadays, we don’t see that.

Nevertheless, risk appetite has changed. It’s not a question of ‘do I have the limit or not?’, but one of ‘am I willing to increase my exposure or not?’.

When you look at large group exposures, one also must bear in mind that they have access to diverse set of lenders. They’re not only dependent on banks. Insurance companies, pension funds, and mutual funds have all grown in scale and size and a lot of the top corporates have access to funds from these pockets.

Banks also invest in corporate bonds but exposure to corporate bonds is lower than other sectors. We could see more corporate bond issuance in the future, driven by regulatory measures at the RBI and Sebi. They understand that for the development of the economy, you need a vibrant debt market, not just a reliance on equity markets. As such, they are prodding banks and corporates to raise a certain proportion of their borrowings through the bond market.

IFR Asia: Do you think the tax regime for India makes it expensive for corporates to raise debt effectively?

Seshagiri Rao, JSW Steel: Tax on foreign borrowings is undoubtedly increasing the costs for corporates. You must look at in which country the lender is located. Then you need to see if there is a double-taxation treaty or not and what is the applicable rate. There are so many other conditions to consider. But no lender, whether he gets the tax credit or not, is willing to pass on that benefit to Indian corporates. Automatically the cost gets grossed up.

There is a need to create a level playing field in terms of the tax deduction at source. Then it will be competitive because, if we add the cost of foreign exchange hedging, then the cost of borrowing overseas is almost equal to, if not more than, the local market.

There is a need to remove it for projects where corporates are raising money overseas, at least until India becomes a developed economy. Over the next 10 years, the capital requirements are so large. India talks about a national infrastructure pipeline of Rs11 lakh crores (Rs11trn) and if you exclude what is being invested by state and central government, then corporate India is expected to invest 30% of that requirement.

To set up large infrastructure projects, Indian corporates need patient capital. One lakh crore rupees (Rs1trn) for a 60-year tenure. That is the kind of capital required for large infrastructure projects.

With credit enhancement during the project or implementation phase, when corporates are setting up large, capital-intensive infrastructure or core sector projects, they would be able to raise money during the period when the project is implemented. Thereafter, they could conduct a take-out financing, as generally happens in many other countries.

These types of things must happen to develop bond markets in India.

There’s enough demand from corporates but, unfortunately, there are not enough suppliers of long-term funding in the bond markets for corporates rated below AA or for projects in the development phase. Money is available in the bond market for well-rated corporates that have completed projects, such as logistics companies. They can raise money but, otherwise, it’s very difficult.

If we take out the money raised by the financial sector and the government, then what is left for corporates to raise in the bond market is very limited. Also, 95% of the total bond market today is privately placed. There are hardly any publicly listed instruments. There is a deep need to develop the bond market, to attract more money from investors, through credit enhancements, for instance, so that corporates can raise money. That’s in addition to the taxation-related simplification that needs to be done.

IFR Asia: Do you think regulators are doing enough in developing the domestic fixed income investor base?

Lakshmi Iyer, Kotak Mahindra AM: The investment landscape for corporate bonds is institutionally driven – banks, mutual funds, insurance companies, provident funds. Then there is the high-net-worth investor (HNI) segment which is also buying corporate bonds directly. The regulatory enablers want to encourage a more seamless and gratifying experience for institutional investors in the corporate bond market. That in turn opens the market to the underlying owners of the mutual funds, a combination of retail and HNI investors.

I think there has been a sea change as far as the regulatory push is concerned.

The precursor to the changes was the anonymous trading platform for government bonds. The over-the-counter market morphed itself into an exchange-traded market and that got extended to corporate bonds in the form of RFQs (request for quote) or request for hold. That system is expected to facilitate more screen-based trading of corporate bonds and that will enhance liquidity. The most common grouse, however, is that the two-way spreads for corporate bonds, in comparison to government bonds, is still very high.

We’ve also seen the development of the electronic bidding platform (EBP) where prices are determined based on demand and supply, thereby increasing transparency for issuers and investors to transact.

Likewise, there are proposals for the number of ISINs a corporate can have to be reduced. The idea here being that if the size of an issue is increased then that might enhance liquidity.

Finally, repos. Corporate bond repos have already been facilitated and there is also the Limited Purpose Clearing Corporation which facilitates corporate bonds being used as collateral. Again this should enhance liquidity.

These measures will promote a deeper and broader corporate bond market and entice more investors.

I would also love to see a deeper CDS market. To my mind this is the key to developing a large domestic corporate bond market on a par to the rest of the world.

These measures have certainly helped in broadening the investor base. We can always make more progress, but we have come a long way.

IFR Asia: Offshore, there has been talk that Indian government bonds will be included in the global bond indices. When will that happen, and will it really help Indian corporates access cheaper money at home?

Prasanna Balachander, ICICI Bank: I really think it’s a big deal for India.

With equity indices, whether it’s emerging markets or otherwise, we get a lot of inflow from passive management – ETFs and index-based funds, irrespective of the macroeconomic situation. Unfortunately, bonds have never been part of such an index so investment by foreign portfolio investors into Indian fixed income is deemed as active management, meaning they have to outperform an index.

So, the amount of money we can attract, even with a positive macroeconomic situation, is not that large. There are many passive funds tracking global emerging market indices as well as global fixed income bond indices, so if India was part of that index, it would be a big game-changer for us.

The government has done fabulous work, along with the Reserve Bank, in finding ways by which we can be part of the index. And it looks like we have taken most of the steps required, such as issuing various bonds without limits, that will ensure that we get into a part of the index.

The last estimates shows that it’s quite possible that India will get around US$20bn to US$30bn in the first year in which index inclusion takes place and the possibility of around another US$8bn to US$10bn every year after that. Of course, that assumes that the assets under management targeting bond indices keep growing.

Index inclusion will push our balance of payments into structural surplus, resulting in currency appreciation as there will be more demand for rupees.

Foreign inflows will also lead to lower borrowing costs as government bond yields will be lower. Foreign investors are always thought of as being bad but active foreign investors think very much the same way as the domestic investor in terms of relative attractiveness across the various asset classes. Passive foreign investors, on the other hand, with a lot of money at their disposal, who must buy an index, who will buy bonds irrespective of the macroeconomic situation. It is not to say that our macros will be worse off, but it means the bar has been set high for the government in terms of financial discipline. It will provide a check on the government’s balance sheet, external debt to GDP ratio and all the other relevant ratios.

The trend in the balance of payments and government bond yields will be very positive from India’s inclusion in an index and that is good news for corporate issuers as well – as was the case with China’s index inclusion.

As money begins to flow into government bond markets and investors get more comfortable with the sustainability of long-term yields in the government bond curve, then money will start to flow into the Indian corporate sector as well. First it will flow into the AAA credits but then, gradually, it will also benefit the rest of the corporate curve.

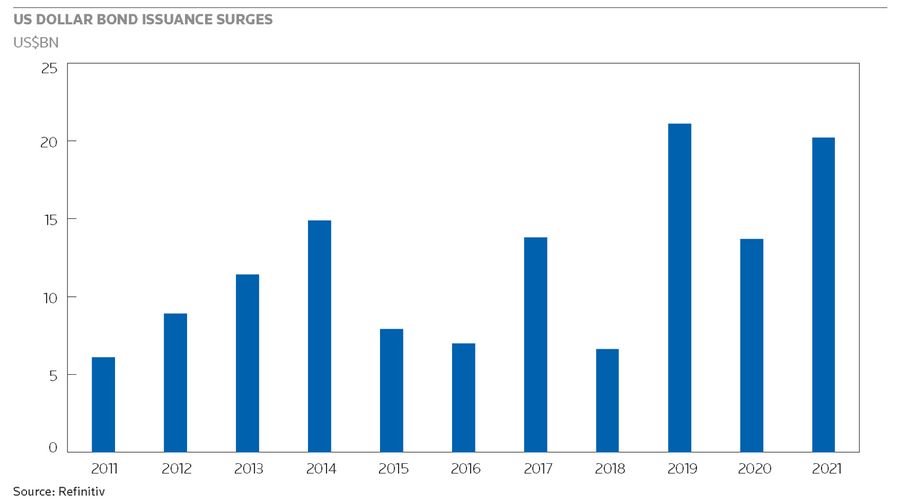

IFR Asia: This year, offshore dollar bond issuance from India reached a new high, with around US$20bn issued by all kinds of borrowers in all kinds of structures.

In the offshore market, infrastructure and renewable energy companies use a special purpose vehicle structure to raise dollar bonds. What is the primary reason for that and do the external commercial borrowings (ECB) guidelines also play an important role in this?

Abhishek Tyagi, Moody’s: The key reason for the SPV structure of forming a bigger group or restricted group is that offshore debt capital markets are more receptive to fully operational projects with no construction or execution risk. So most issuers form a restricted group of operational assets, and the cashflows from these assets are used to service the debt.

There is typically an SPV, which is just an issuing vehicle that sits on top of this restricted group. There have been few direct issuances from the operating companies, directly issuing a bond either on a standalone basis or as co-issuers.

Renewable energy issuances from India in the offshore market typically have project finance features: a static pool of assets, a full security package, cashflow waterfalls, restrictions on debt incurrence, restrictions on distributions. There are also various reserves built into the cashflow waterflow. These features protect the debt holder’s interest and ringfence the obligor group from the rest of the corporate entity, which might be engaged in capacity addition plans, it might be exposed to other risks as well: say, exposure to a very weak off-taker, for example.

ECB guidelines also put some restrictions, such as an all in-price ceiling, restrictions on the tenure and size of an issue, which also plays a role in the way some of these transactions are structured.

IFR Asia: India’s ECB rules are quite constraining. What would you like to see to help borrowers access the dollar bond market?

Seshagiri Rao, JSW Steel: There are different sets of investors with different risk appetites in the global bond markets. There’s enough money available. Now the issue here is, under automatic route, the total amount that can be raised by each corporate in a financial year is restricted to US$750m. If you want to raise more than US$750m, you need official clearance.

Working capital requirements are also very large for Indian corporates.

Money is available in the overseas market, but we need changes to the end use requirements. That will enable corporates to raise money and use it for different purposes.

IFR Asia: India’s infrastructure financing requirements are sizeable. Can bond markets provide a viable means of funding India’s infrastructure?

Prasanna Balachander, ICICI Bank: We can’t over emphasise the importance of infrastructure and the financing needed if the government is to meet its ambitious targets.

Infrastructure financing through the bond markets takes place directly and indirectly. Most of the financing in India takes place indirectly. You have companies like India Railway Financing Corp (IRFC) issuing bonds, infrastructure bond issuance from banks, like ICICI Bank, and you have bonds issued by financial institutions, like the Small Industries Development Bank of India (SIDBI), National Housing Bank (NHB), Housing and Urban Development Corp (HUDCO), which all on-lend to the infrastructure sector. Then you have the infrastructure debt funds. These issuers are rated AAA by the credit rating agencies and hence have been the preferred route by which infrastructure financing happens in India.

There has been less volume in the direct route, but that is starting to change. We are seeing more deals from the likes of the road sector, the renewables sector, and from airports. They have all received a lot of interest from investors.

If you look at the regulatory push for infrastructure financing, there are a few things which the regulators have done, like, InvITs and REITs, and I think that’s going to be a great help.

They have also enabled banks to classify infrastructure investments of more than seven years as HTM (held to maturity), which is positive for the banking sector. Insurers are also required to invest 15% of their investment assets in infrastructure, especially housing.

What else? Regulators could increase investment limits for end investors so that more and more infrastructure financing becomes accessible through bond markets. I think there should be a higher limit for each of these bond categories. Guidelines for banks to lend to REITs have still not come through. So, hopefully that will happen. And then project bonds could be a way forward. A lot still needs to be done.

IFR Asia: Could we see more international bonds with different kinds of infrastructure assets underlying them?

Abhishek Tyagi, Moody’s: We have seen offshore issuance from several sub segments of infrastructure over the last 12 to 18 months, including toll roads, transmission and distribution companies, airports, ports and container terminals. Most of the issues have been in the renewable energy sector.

The government of India has announced the national asset monetisation plans where it wants to lease around Rs5trn–Rs6trn worth of assets spread across various infrastructure asset classes.

These will be fully operational assets, typically with long-term purchase agreements or concession agreements, which will make them attractive not only for equity investors but also for international bond investors.

The key challenge remains the stability of the policy framework – no cancellation or changes in past agreements that make projects unviable. We are seeing some of that in Punjab, for example, for the renewable power projects.

Another challenge for some segments is the credit quality of the off-takers and there could be other operational challenges as well, like, the ECB guidelines.

IFR Asia: How has the credit quality of offshore bonds from airport operators been affected during Covid?

Abhishek Tyagi, Moody’s: Airports were the most impacted sector globally during the pandemic due to travel restrictions and health concerns. It was no different in India. Performance of most rated infrastructure issuers was quite stable, but airports suffered.

We downgraded Delhi Airport twice between March 2020 and June 2021 and it is still on a negative outlook. We downgraded GMR Hyderabad Airport by one notch in June 2020 and that too is on a negative outlook. Both these airports were negatively impacted by the sharp decline in traffic, but volumes are slowly picking up with the acceptance of the Indian vaccination programme. International traffic should also pick up gradually.

What compounded the problem for these two airports, however, was that they were undergoing a massive debt funded expansion when the pandemic struck. They were not able to postpone these expansion projects, which compounded their financial problems. Interestingly, both airports were still able to raise capital, which provided some liquidity buffers.

So while things are looking better for the airports today, our base case is that it will take one to two years for domestic traffic, and two to three years for international traffic, to revert to 2019 levels.

IFR Asia: Moving on to instruments supporting bank capital, after Yes Bank’s Additional Tier 1 write-down, we saw the regulator step in and bar retail investors from buying AT1s. How have funds coped with such onerous rules for investing in the AT1 bonds of Indian banks? And what options are available for investors with an appetite for such instruments?

Lakshmi Iyer, Kotak Mahindra AM: Mutual funds were clearly an integral part of the Tier 1 and Tier 2 bond markets, given their comfort with most of the underlying issuing entities – a combination of large public sector banks and prominent private sector banks.

Then we had a couple of back-to-back instances which led to basic questions being asked with respect to the suitability of Tier 1 bonds in mutual fund portfolios and there has been an organic loss of appetite in the mutual fund segment for such assets.

I think going forward, the way for investors to take part in this sector is to buy paper from the savvier banks, where credit risk is less of a concern. Retail investors can directly own these bonds, but mutual funds will have constraints. Within those constraints you will have some funds having anywhere between 5% to 15% allocated to these bonds, depending on the underlying nature of the funds. But, yes, there is a vibrant secondary market today for Tier 1 bonds that can be explored by the retail investor.

IFR Asia: What are the options for Indian banks unable to raise Tier 1 bonds through the domestic market?

Karthik Srinivasan, ICRA: The answer is quite simple, if you don’t have an option or ability to raise AT1 from the domestic market, then either you raise equity or you look overseas. So that apart, one also needs to factor in a couple of things.

While some entities had challenges to raise AT1s in the not so distant past, over the last couple of quarters, we have seen some come back to the market. SBI did a large issue, but not every bank would be able to get that kind of a response.

Unlike in the last couple of years, when even public sector banks were not able to raise equity from non-government sources, we have seen several public sector banks tap the equity markets in small to medium-sized issuances with some success.

We believe these smaller banks may also be able to raise smaller-sized AT1 issues, depending on timing, investor appetite and market conditions.

IFR Asia: We’re seeing a few agency loan banks coming back to the domestic market to raise AT1 capital. This line-up is quite huge, at Rs110bn, or around US$1.5bn. What is the demand outlook for the Indian banks who want to raise onshore AT1s and where is it coming from?

Prasanna Balachander, ICICI Bank: So I think issuance over the year has been substantial and AT1 bonds has been popular source of financing for the banks in India. Overall issuance last year stood in the region of around Rs180bn–Rs190bn; there was no offshore issuance. But this year we have seen that number coming down to something like Rs110bn or so in the onshore market whereas there has been around close to Rs120bn issued in the offshore market.

There have been some challenges, which has left the market with a very limited set of investors. For example, the changed regulations on valuations allowed for mutual funds has meant that mutual funds, as an investor category, have been completely absent in the onshore AT1 market. Insurance companies also had a two-year cool-off period as far as dividend paying scheduled commercial banks are concerned. That resulted in secondary market liquidity falling and the entire size of the AT1 onshore market reducing.

Lower-rated banks will continue to face difficulty in raising capital because, as demand wanes for these credits and interest rates go up. But I think the well-run, large-sized banks will be able to diversify their sources by going offshore.

Rates are quite expensive right now and, unless a bank really needs capital, they won’t want to use the AT1 route.

So, it’s not very clear-cut as to the demand for AT1 capital, especially in the onshore market.

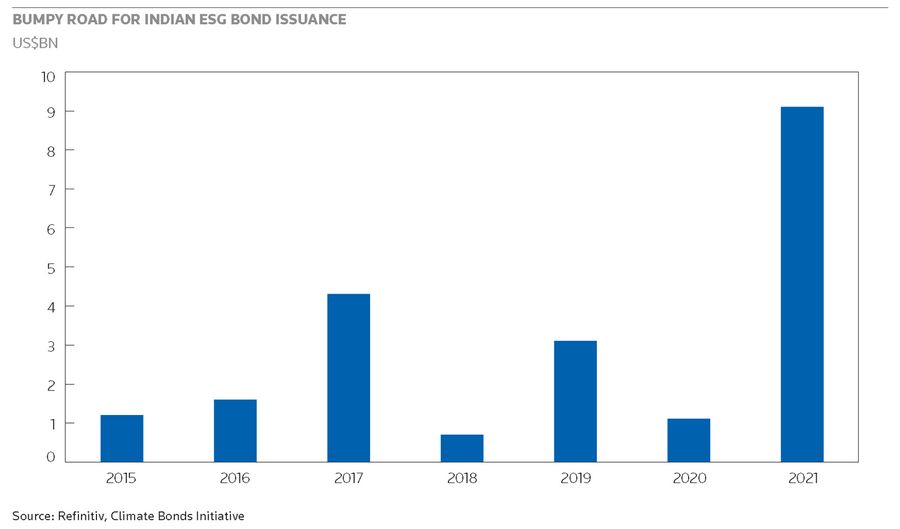

IFR Asia: ESG has finally caught on in India with market regulators pushing companies to report their ESG credentials from April 2022 onwards. This year we have seen PLENTY OF ESG bond issuance from India, including JSW Steel’s sustainability-linked bond.

Are the regulators doing enough to push corporates to raise capital based on ESG principles?

Seshagiri Rao, JSW Steel: It is a good initiative to report ESG-related parameters in a transparent manner. This gives Indian corporates a huge opportunity to tap capital in the international and local markets. More and more funds and investors are committing money to corporates that uphold sustainability reporting and sustainability standards.

Transparency in reporting will enable investors to understand the progress made in adhering to and improving sustainability.

IFR Asia: How can India benefit from this boom in sustainable financing?

Prasanna Balachander, ICICI Bank: The ESG development is great for the corporate sector, especially those that really want to be at the forefront of sustainability as far as climate change is concerned. It goes beyond the ability of the corporate to raise funds as the level of audit required, the transparency and disclosures for being ESG eligible is so high that it improves the overall brand image of the company.

Interestingly, the culture is far more prevalent in the global markets where investors are willing to take lower returns for an ESG eligible bond issue, because they are aware that the costs associated with issuing an ESG bond is quite high for a corporate and they will have to offset that cost with a lower coupon on the bond. There are investors – family offices, HNIs (high-net-worth investors) – that have publicly stated they will invest a particular proportion of their wealth in this kind of bond and they’re okay with the lower returns. That’s the culture, that’s the trend which we have seen globally.

India has still not come to that kind of level of comfort as far as investing is concerned.

I think that challenges on costs are there. Regulators could help overcome these challenges by giving incentives that help offset the extra cost incurred by corporates in undertaking audits and extra transparency procedures. That would encourage companies to issue this kind of security.

IFR Asia: What are the hurdles for the development for the ESG bond market in India?

Lakshmi Iyer, Kotak Mahindra AM: I don’t know whether you need to call them hurdles, it is more about awareness.

When we talk about ESG to fixed income investors, there has been a lukewarm response. Whereas if you talk about equities, the response is warmer.

If adherence to ESG for a corporate translates into a lower cost of borrowing then the investor could ask: if I hold a senior secured bond at a yield I am comfortable with, then what is the pressing need for an ESG or a green bond in the portfolio that might detract from its performance?

It’s about awareness.

There are things that could help promote greater participation. Regulators could offer some capital allowance for ESG fixed income investment funds, and there could be improved standardisation when it comes to ESG credit scores, for instance. And improved engagement between fund managers and issuers. It’s not about just divesting less-green companies from the portfolio but more a case of interacting with invested companies, trying to understand what they are doing from an ESG perspective and helping them improve their performance.

IFR Asia: Moving on to GIFT City (Gujarat International Finance Tec-City), it has a come up as a financial centre for corporates and Indian issuers raised a record amount of US$10.5bn through GIFT City this year.

What is the outlook for GIFT City?

Seshagiri Rao, JSW Steel: It is gaining attraction. Whether it is possible for Indian corporates to list their shares or securities in GIFT City is being studied. Once it gets traction, then maybe we’ll see corporates listing securities in that market.

IFR Asia: Will it become easier for banks to meet the funding capital needs of corporates from the GIFT City branch?

Prasanna Balachander, ICICI Bank: Yes. GIFT City is well positioned to emerge as a key financial centre connecting the two different time zones of Asia and London. I think the creation of IFSCA (International Financial Services Centre Authority) as a regulator speaks volumes about the policy focus when it comes to international financial services centres such as GIFT City. There are multiple incentives for companies operating there, such as a tax holiday for the first five years.

Over a period, there will be a lot of demand side developments. India-linked investors, large international investors or those situated in offshore jurisdictions that are investing into India can get situated in GIFT City. On the supply side, issuers are also listing bonds there. So, you can see demand and supply meeting in the GIFT City framework.

Along with that, instruments such as NDFs (non-deliverable forwards) have also been enabled at GIFT, helping in the onshoring of the offshore markets. With these instruments and foreign currency bonds, then the bond currency derivative nexus is complete. GIFT City is a necessary condition for future market development.

Banks, even those without international branches, can establish their GIFT City branch here as an offshore branch. They would be able to access international markets, able to access funding at low cost and on-lend this liquidity to corporates, not only for capital expenditure but for transaction requirements, such as trade finance.

We see GIFT City becoming a hub for US dollar liabilities. In the medium term, we feel positive about GIFT City and the focus of the regulatory framework.

IFR Asia: What is the view on the term curve? Has it priced in a hike in rates and what does it mean for the credit quality and the liquidity premium for corporate bonds?

Lakshmi Iyer, Kotak Mahindra AM: Yes, it has priced in a rate hike. Short-term yields are inching up faster, so the yield curve is flattening.

Alongside this has been a complete collapse of spread in the credit space. This is attributable to corporate India deleveraging. Working capital requirements have shortened, incremental credit uptake is not there, which means less issuance across the credit spectrum. Investors are chasing the same credit and terms spreads are collapsing.

We are seeing similar trends across the globe. India is not an exception.

To see the digital version of this roundtable, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@lseg.com