January saw the worst start to a year for US credit in at least half a decade, as concerns about the impact of higher interest rates cascaded through financial markets. It was also exactly the kind of environment favoured by systematic credit strategies, a small but growing part of these markets that has the potential to revolutionise the staid world of corporate bond investing.

“We actually look forward to volatility,” said Robert Lam, co-head of credit at systematic investment manager Man Numeric. “We tend to have a crisis 'alpha' behaviour – that’s when these strategies have historically done well. If you’re long and you’re short something, you need bonds to move in different directions and that increased dispersion tends to really help these types of strategies.”

The vulnerability of corporate bond markets in the face of the US Federal Reserve winding down its extraordinary stimulus measures certainly does no harm to the sales pitch for quantitative credit, where investors use financial models to identify price discrepancies in corporate bonds and related markets.

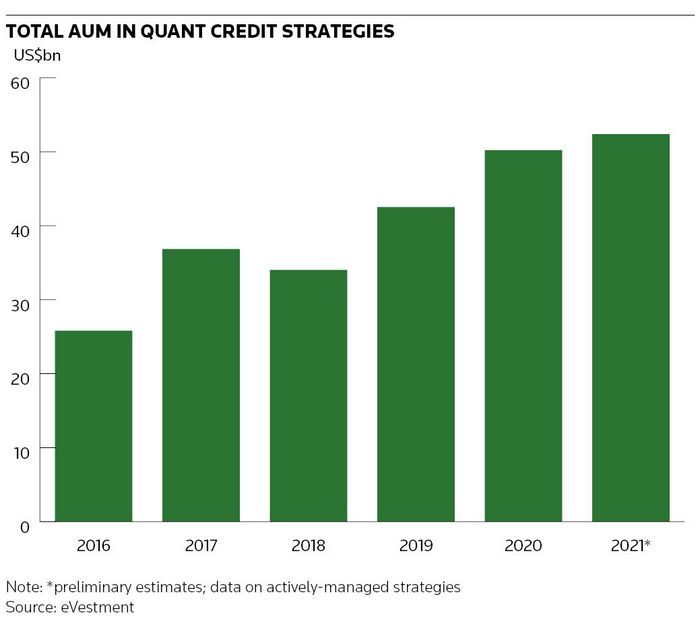

But the drumbeat around systematic credit investing has been building for some time now amid a structural shift in the way corporate bond markets are traded and organised towards a more equity-like model. That upheaval is opening the door to a new breed of investors intent on shaking up corporate credit with the kind of model-driven strategies that are now prevalent in equity markets. Assets under management in actively managed quant credit strategies have more than doubled over the past five years to US$52bn in 2021, according to preliminary estimates from data firm eVestment.

That is still small in the context of the broader market: these strategies account for about 0.4% of the roughly US$66trn investable fixed-income universe, according to BlueCove, a London-based investment manager. But many believe greater use of systematic investing in credit is inevitable and note its effects are being felt already, in the form of trend-following funds known as commodity trading advisers fuelling swings in ultra-liquid credit-default swap indices, or market-neutral strategies creating sudden ripples in the corporate bond market.

“Systematic CTAs have become a huge part of the market in [major US CDS indices] and play an important role in driving price action,” said Yoni Gorelov, co-head of US credit trading at Barclays. “Last year we really started to see an acceleration on the corporate bond side too. That has impacted market technicals at times – some of the quant-driven moves in individual bonds have been fairly significant."

Decades-old

Quant investing traces its origins to the equity markets several decades ago, where hedge funds like Renaissance Technologies and DE Shaw pioneered the use of computers and technology to identify and profit from inefficiencies in stock prices. Such strategies have mushroomed since then and now occupy a prominent position in stock markets, accounting for around US$10trn – or about 15% of investable equities, according to BlueCove.

Many doubted whether the human-dominated world of corporate bonds – where the majority of trading still takes place over the phone – could ever make the leap to systematic investing. The markets were thought to be too illiquid, expensive to trade, opaque and lacking in technological innovation to make this methodological style of investment a realistic goal. Much of that was down to the inherent complexity of the asset class: companies can have hundreds of bonds with different maturities and coupons; they typically only have one stock price.

Paradoxically, it's these same nuances – as well as the fact that the vast majority of credit managers follow traditional investment approaches – that makes these markets so ripe for disruption, quant firms say.

“We’re not seeking to remove humans from the process. Rather, the scientific process moves humans and technology into the roles for which they are best suited. Humans are great at designing processes; they tend to be generally poor at outright forecasting,” said Alex Khein, co-founder and chief executive of BlueCove.

“To run a scientific process you need data, a sophisticated market structure, sufficient market breadth, and research innovation. All these aspects were present in equity markets at the turn of the century. We’ve seen all of these key inputs become evident in fixed income over the past few decades, heralding what we believe is a parallel rise in scientific fixed-income opportunities,” he said.

Electronic leap

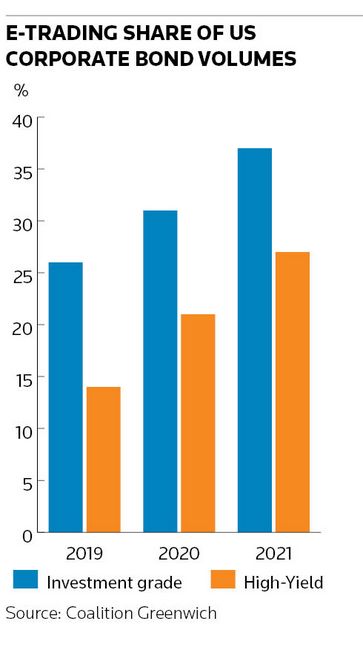

There is no doubt that credit markets have made significant leaps forward in recent years, with developments in algorithmic and electronic trading making it far easier for investors to switch corporate bond positions at the click of a button. The proportion of US corporate bonds traded electronically increased 11 percentage points over the past two years to 37% for investment-grade securities in 2021, according to data provider Coalition Greenwich, while high-yield volumes nearly doubled to 27%.

“The growth in electronic trading globally has been pretty dramatic. That has brought in more participants and created a virtuous cycle, where the data generated from e-trading makes systematic strategies easier to research and to implement, which in turn generates more data,” said Kevin McPartland, head of market structure and technology research at Coalition Greenwich.

Still, it would be wrong to suggest these credit funds closely resemble their peers in the highly computerised world of systematic equity investing. Quant credit specialists note that while their approach is primarily data and research driven, humans still play a pivotal role in reviewing the output of any models and then trying to put the results into practice as systematically as possible. That may still involve picking up the phone to place a trade, particularly when markets get choppier.

It’s “not a black box where there’s some computer finding non-linear relationships that are unseen to the human mind, nor is it a computer doing auto-execution,” said BlueCove’s Khein.

Industry-level data on the US high-yield market show a steady performance for quant credit strategies versus traditional approaches over the past few years, according to eVestment. That includes a 5.2% return on average for actively managed quant strategies last year compared to 5.5% for traditional managers. The quants achieved a very slight outperformance in 2020’s rockier markets with a 6.7% return, while traditional managers outpaced them by two percentage points in 2019 with 13.8%.

Growing interest

Interest among the investor community certainly appears to be growing. Twenty-eight percent of asset allocators recently said they were looking to increase their investments in systematic credit over the next 12 months, according to a BNP Paribas survey of 47 allocators that invest in or advise on hedge fund assets worth US$247bn.

Banks are already eyeing the potential opportunities to provide financing to these strategies given the amounts of leverage often needed to hit return targets. Quant equity funds are already an important source of revenue for banks’ prime brokerage units.

“We’re excited from a financing standpoint about the potential for growth. These strategies require leverage in line with or greater than quant equity portfolios, however, they have less data and may not be as liquid, which requires further margin analysis and development,” said Marlin Naidoo, global head of capital introduction at BNP Paribas, adding his firm had built such capabilities.

The speed at which systematic credit grows may well hinge on how fast corporate bond markets continue to evolve. For all the advances of the past few years, some note the tendency of fixed-income liquidity to deteriorate rapidly when volatility rises – and the potential that has to hurt investors, particularly those looking at cross-asset arbitrages. Barclays’ Gorelov said some funds have “de-emphasised single-name strategies” given the lack of liquidity in CDS versus other markets like equities.

But despite such bumps in the road, there’s little doubt about the direction of travel – or the opportunities investors spy in the still largely undiscovered realm of systematic fixed income.

“Quant equity is a very developed market,” said Giuliana Bordigoni, director of specialist strategies at systematic investment manager Man AHL. “Credit markets are far less efficient and transparent, which creates more opportunities and makes credit a natural move forward.”