The Asian high-yield bond market is poised to recover from one of the most challenging years in history, presenting opportunities for investors and issuers alike.

Current secondary prices present value for investors who think the worst has passed, while the decline in issuance from the traditionally dominant Chinese property sector means different kinds of issuers could attract more attention.

Last year started with a lot of promise with issuance on track for an annual record. But when China Evergrande Group, the world’s most indebted developer, missed an interest payment in September it thrust the Asian high-yield market into a tailspin.

“The concept of too big to fail obviously has been proven wrong,” says Daniel Kim, managing director, head of high-yield capital markets and the commercial bank debt origination team at HSBC. “It’s had a very negative contagion effect for the whole sector. For some of these companies being impacted, a lot of it is purely just liquidity issues.”

Yields spiked for Asian high-yield bonds following the Evergrande news, and even China’s sovereign CDS spread blew out to 60bp from 34bp at the height of concerns in October.

“There might have been babies that were thrown out with the bathwater,” agrees Suanjin Tan, APAC fixed income portfolio manager at BlackRock. “The bottom in a way is somewhere behind us but the road to normalcy will continue to be bumpy. Even though there is volatility the valuations in this space really offer a lot of potential for excess returns over the next 12 months but investors will need to be able to stomach the volatility until relief measures from the Chinese government materialise.”

In fact, there are already signs that new money seems to be timing the market bottom after Evergrande’s incident, with almost half of the retail bond funds tracked by HSBC Research reporting fund inflows in the first 10 months of 2021 despite the negative total returns.

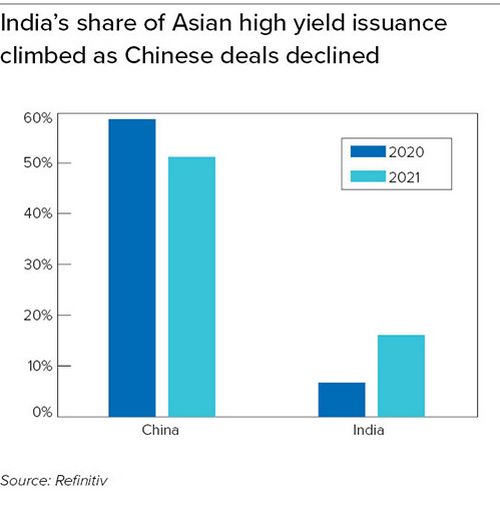

India as a shining light

The Asian high-yield primary market understandably slowed to a trickle as Evergrande’s woes increased.

In recent years, China real estate bonds have made up the largest chunk of Asia ex-Japan’s high-yield US dollar market, but their share fell in 2021. Bond issuance volume from the sector made up 72.8% of the Asian market in 2020, but that proportion dropped to 54.6% in the first 11 months of 2021.

Indian issuers have been quick to take advantage of the reduced Chinese supply.

The country saw an impressive 112% surge in high-yield G3 deal volumes to $12.1bn last year, from $5.7bn in 2020. This uptick in Indian deals means that Asian G3 high-yield issuance in terms of volume was down by just 12% on the previous year.

India is now the second-largest player in the Asian US dollar high-yield market with a 16.1% share, as companies diversify away from bank loans.

“The shining light definitely has been India and I think this will continue into 2022 with India making up a much larger portion of the market,” says Kim, mentioning specifically the renewable and tech sectors.

ReNew Power, one of the largest renewable energy independent power producers in India, was one of the companies that was quick to see this window of opportunity.

The company’s $400 million 4.5% green bond was the first high yield issuance out of South Asia in 2022.

“The recent events in China have led investors wanting to diversify away from China, and hence Indian issuers are attractively placed in that sense,” said Kailash Vaswani, ReNew Power’s President Finance.

BlackRock’s Tan said diversification has delivered stable returns for investors in Asia ex-China, but needs to be balanced against the lower yields on offer compared to Chinese high-yield.

“Asia ex-China definitely has outperformed and is trading very close to where the US high-yield market is trading at,” says Tan.

M&A opportunities

Bankers hope that consolidation in the Chinese real estate sector may lead to opportunities to fund mergers and acquisition in the offshore market as the larger players pick up distressed assets.

“Asset and project stake disposals are becoming common ways for developers and property service companies to ease liquidity issues these days,” says HSBC’s Kim. “Those with stronger balance sheets are set to act as ‘white knights’ to support the financially weaker market players, which provides the basis for market consolidation via mergers and acquisitions and corporate actions.”

With a wall of refinancings of US$80.5bn in Asia including Japan between now and the first half of 2023, more companies are expected to undertake liability-management exercises such as tenders and exchange offers.

But for the market to truly recover, more clarity is needed on the likely outcomes of debt restructurings, and on the true financial health of companies.

The tumultuous year is expected to encourage investors to be more stringent with their due diligence and could encourage them to look at issuers from more diverse industries.

“As we enter a rate increasing cycle, I think investors may want to focus on the quality of the issuers,” said ReNew Power’s Vaswani. “There will be a flight to quality.”

As HSBC’s Kim says, “it’s somewhat of a cleansing. Some names shouldn’t have been tapping the bond market for the amounts they were. But the capital isn’t going anywhere, so we shall see new sectors and new types of issuers including from China such as those in electric vehicles, data centres, renewables, tech and healthcare.”

PRODUCED IN ASSOCIATION WITH HSBC