Futures trading volumes tied to the secured overnight financing rate have surged this year, the latest sign that the transition away from US dollar Libor across financial markets is accelerating.

Average daily volumes in SOFR futures reached 964,000 contracts in the two weeks ending February 4, according to derivatives exchange CME Group, up from about 290,000 in December and more than five times higher than their September level.

That steep rise in activity comes against the backdrop of traders scrambling to adjust positions in anticipation of the US Federal Reserve raising interest rates in March. On Thursday, preliminary CME figures showed SOFR futures volumes hitting a new daily record of over 2m after a closely watched gauge of US inflation came in higher than expected.

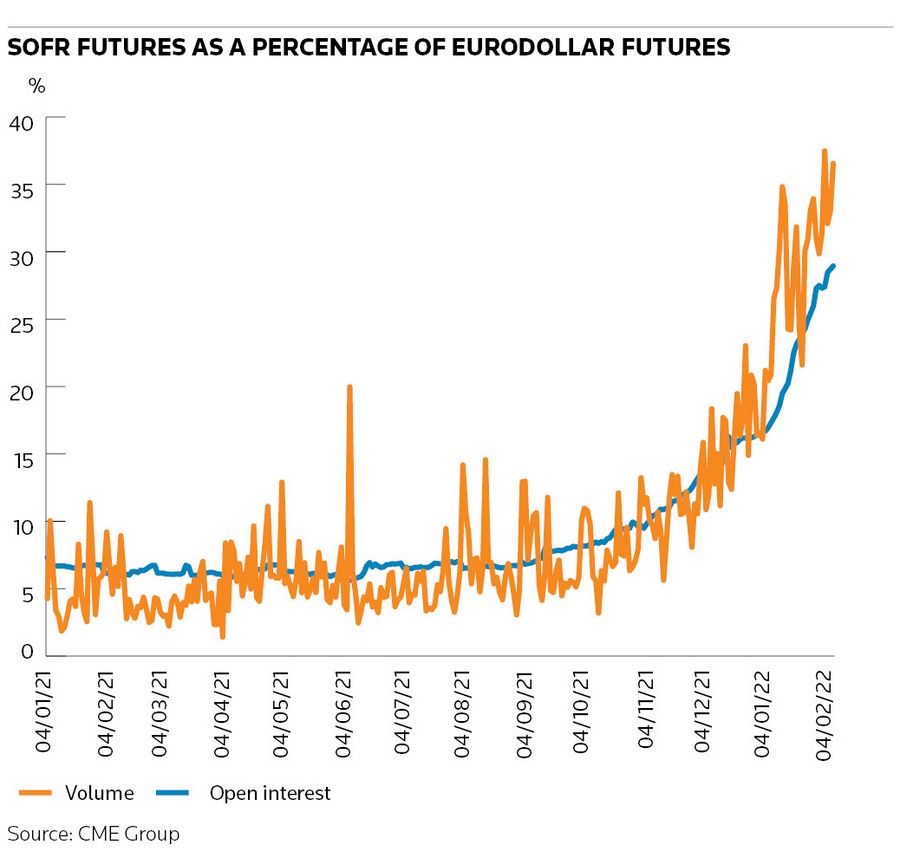

But SOFR futures have also closed the gap this year to Eurodollar futures, the Libor-linked contracts that have long been a mainstay of rates trading markets and that SOFR futures are set to supplant altogether from the middle of 2023. SOFR futures volumes as a share of Eurodollar contracts have reached as high as 37% this month, compared with an average of 10% in the final quarter of 2021.

“There’s been a significant change in behaviour over the last few months and we’re now seeing exponential growth in SOFR futures activity. Records are being broken almost daily,” said Mark Rogerson, head of interest rate products for EMEA at CME Group.

“We thought there’d be an acceleration moving into 2022 when the regulatory guidance provided a catalyst. We’re now at a point where we’ve achieved critical mass in SOFR futures: liquidity is more than sufficient for almost all customers’ needs.”

US regulators’ efforts to eradicate US dollar Libor from financial markets have stepped up a gear in 2022 as they look to catch up with other major jurisdictions that have largely succeeded in removing the controversial bank lending rate.

Banks faced a year-end deadline to stop offering clients over-the-counter derivatives linked to US dollar Libor, except for trades that would help investors reduce risk tied to the old benchmark. ISDA data show SOFR has now overtaken Libor as the main reference rate in US dollar swaps markets by trade count this year, though Libor-linked activity has still been larger when measured in notional terms.

Many firms active in trading futures markets aren’t subject to the same regulatory pressures to drop US dollar Libor as major investment banks, granting them greater leeway to continue trading Eurodollar contracts for now.

But with the remaining US dollar Libor fixings scheduled to disappear in mid-2023, the market still faces a looming deadline to transition to regulators’ preferred replacement rate of SOFR. CME Group has also introduced fallback language that will automatically convert any remaining Eurodollar positions to SOFR futures at that point.

“The challenges to transition are perhaps mostly human in nature – it’s a matter of habits in some respects. We’ve tried to reduce all of the friction that customers might face to make it as smooth as possible,” said Rogerson.

CME Group is seeing strong interest in trading SOFR futures across the interest-rate curve, though just over 50% of activity is in shorter-dated contracts right now. That is perhaps unsurprising given the current focus on central bank rate rises.

Activity in SOFR options has started to pick up too, albeit from a low base. Average daily volumes have rocketed from 36 last year to 12,000 in January and 79,000 in early February. Meanwhile, open interest has jumped from 2,700 contracts in early January to 504,000 on February 4.

“We always expected options would come second to futures in the transition,” said Rogerson. “Options markets in sterling went from zero to full speed in under three months. The pace of change in SOFR options could be even faster than in futures.”