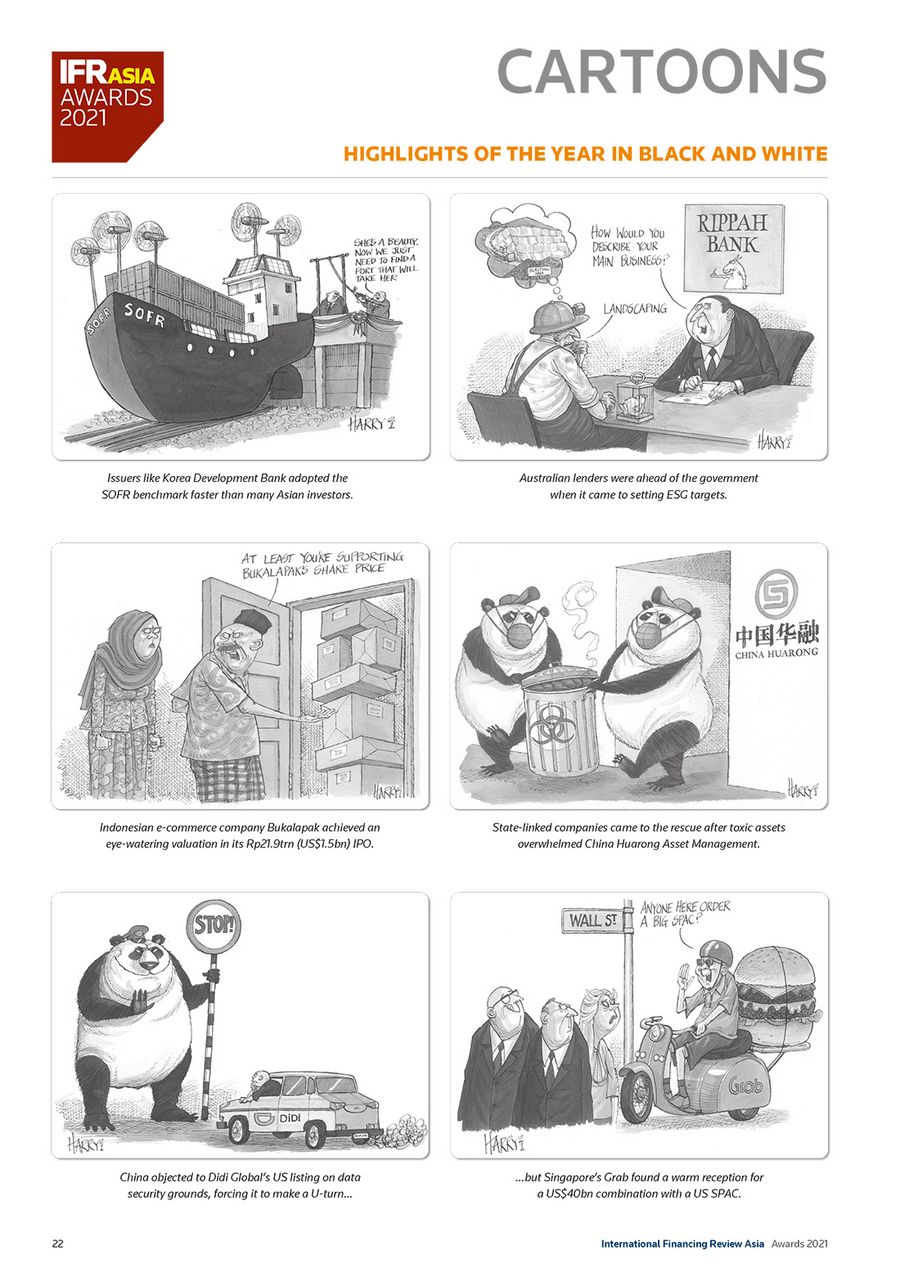

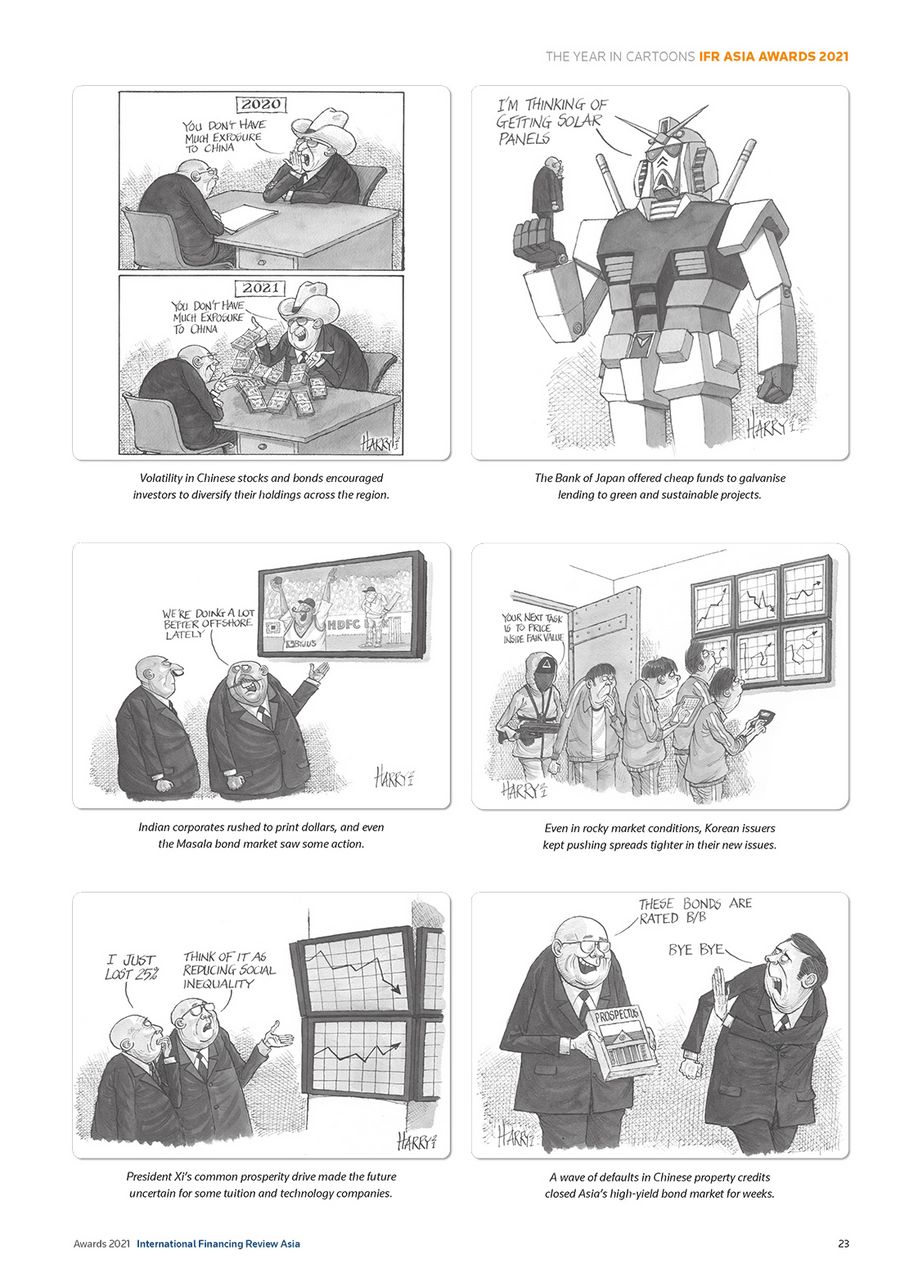

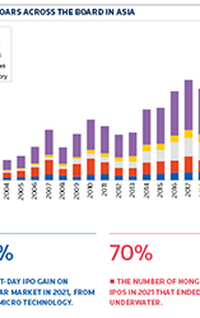

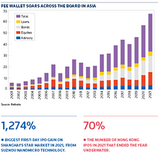

Highlights of the year in black and white

To see the digital version of this report, please click here

To purchase printed copies or a PDF, please email gloria.balbastro@lseg.com

To see the digital version of this report, please click here

To purchase printed copies or a PDF, please email gloria.balbastro@lseg.com

Asia’s debt restructuring landscape in 2021 revealed its increasingly dual nature: China, and the rest of the region. South and South-East Asian legal regimes remain challenging although reform is underway, led by India, Singapore, Malaysia and the Philippines and hope springs that greater transparency and predictability will emerge as markets develop. “Undoubtedly China distressed is perceived as the new frontier for Asian debt restructurings,” said Jamie Mclaughlan, director at advisory firm PJT Partners in Hong Kong. “Over many, many years...

When India’s Masala bond market was launched in 2014, the hope was that it would become a vibrant issuance arena underpinned by deep secondary liquidity and a wide variety of foreign investors and traders. To say that the market has disappointed would be an understatement, but optimists are calling a turn. The International Finance Corporation opened the Masala market with the announcement of a bond programme in 2013, following severe stress in India’s capital markets as a result of concerns about the country’s budget deficit and the “taper...

It’s all change at the Tokyo Stock Exchange, or at least it will be on April 4. But opinion is divided about whether the planned upheaval will do enough to inject new life into one of the duller corners of the world’s equity markets. Japan Exchange Group, which was formed in 2013 through the merger of Tokyo Stock Exchange and Osaka Securities Exchange, is to simplify the TSE, cutting the five market sectors to three. The current First, Second, and Mothers sections and the two sub-sections of Jasdaq will be split into Prime, Standard and Growth...

To see the digital version of this report, please click here To purchase printed copies or a PDF, please email gloria.balbastro@lseg.com

To see the digital version of this report, please click here To purchase printed copies or a PDF, please email gloria.balbastro@lseg.com

Admiralty Harbour Where offshore vehicles dock after hitting the rocks AI-powered Fair marketing claim, as long as your business uses computers Archegos Proof that being banned from trading in Hong Kong doesn’t have to limit your career Beijing Stock Exchange Niche market for issuers that weren’t quite right for the four existing boards in Shanghai and Shenzhen Bond buyback Attempt by an issuer to reassure investors that its US$50bn of debt is manageable by repurchasing US$10m of paper in the secondary market Carrie trade Going all-in on...