Investors in Russia and Ukraine securities are facing the prospect of big losses after Russian president Vladimir Putin gave the go-ahead for an invasion of Ukraine, even though prices were recovering by the end of the week.

Many banks and fund managers had overweight positions on Russian and Ukrainian assets, despite ominous warnings for several weeks from policymakers and some EM strategists that a war was increasingly likely.

"The market went into this crisis long Russia and Ukraine, so it’s all taken most investors by surprise," said Tim Ash, senior EM sovereign debt strategist at BlueBay Asset Management, who had been warning bankers and investors for several months that Putin would order an attack on Ukraine. "Most big Western banks, and Russian banks, had the rouble as the best investment – they argued that strong balance sheet outweighs geopolitical risk – [and were] long local Russia rates and credit."

Given that Russia and Russian corporates are members of bond and equity indices, it would have taken a very brave investor to have completely withdrawn their exposure to the country even as Russia massed troops on Ukraine's borders. In one way or another "everyone is involved", said Holger Mertens, head portfolio manager for global credit at Nikko Asset Management. "Anyone who runs a corporate portfolio is exposed."

"Very few of our peers had got completely out of Russia and we hadn’t," said Paul McNamara, an emerging markets fund manager at GAM. "Nobody really expected a full-scale invasion, but I don’t think anybody was happy to assign it a zero probability."

Public filings of Russia's US dollar and euro bonds show US and European investors such as MetLife, Fidelity, AIG AM, Uniqa Insurance Group and Carmignac, among those with holdings. The US investors declined to comment, while Carmignac did not immediately respond to a request for comment.

Kurt Svoboda, chief financial and chief risk officer at Uniqa, said the Austrian insurer has €380m of assets in Russia (and €150m in Ukraine). While he acknowledged that in a "worst-case scenario" it would suffer a loss on these assets, it would be "economically manageable".

A senior banker said it had been difficult ahead of the invasion not to be bullish about Russian securities, given the broad macroeconomic backdrop and especially without knowing if any sanctions would be announced against Russia or Russian entities, and how harsh they might be. "With the rouble selling off and oil prices strengthening, from a credit perspective that's a gift for dollar exporters with a rouble cost base," he said.

Now, though, risk managers at banks and investment firms will be scrambling to quantify potential losses. Russian assets in particular took a beating as the threat of an invasion turned into reality on Thursday, although on Friday there were signs of a relief rally as the series of sanctions announced against Russian interests by the US, EU, UK and others were not as aggressive as initially feared.

Incredible levels

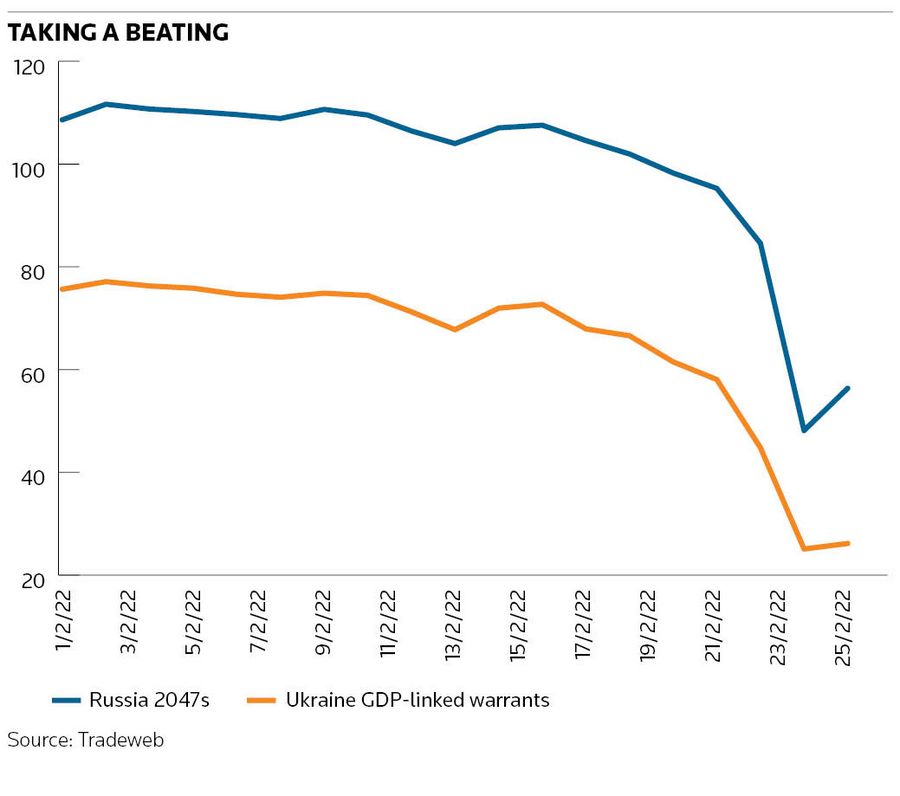

Even so, Russian securities were still trading at incredible levels given where they were earlier in February, with the sovereign's June 2047 bond, for example, bid at around 74 cents to the dollar after the US open on Friday, according to Tradeweb. Just two weeks ago it was bid at a cash price of around 110. At one stage on Thursday it had fallen to below 50 – although it is debatable how much trading was taking place. "Flows are close to zero," said a second banker. "Traders are marking their books."

Even seasoned bond traders were stunned by the moves. "It's so surreal, and the speed of the moves has been startling," said one on Friday. "It's quite amazing – all the off-piste Russian and Ukrainian quasi-sovereigns and corporates have been totally annihilated. The fallout is going to be enormous, as there’s no ability or door to get out of anything. Everyone who underestimated the chance of a [major] military conflict is in a pretty bad way from their investments."

Another trader said it was one of those look-back moments. "This kind of event stops the whole market ... some of these levels are ridiculous. Russia in the 40s is a proper fucked-up scenario. A lot of people [could] get carried out," he said on Thursday.

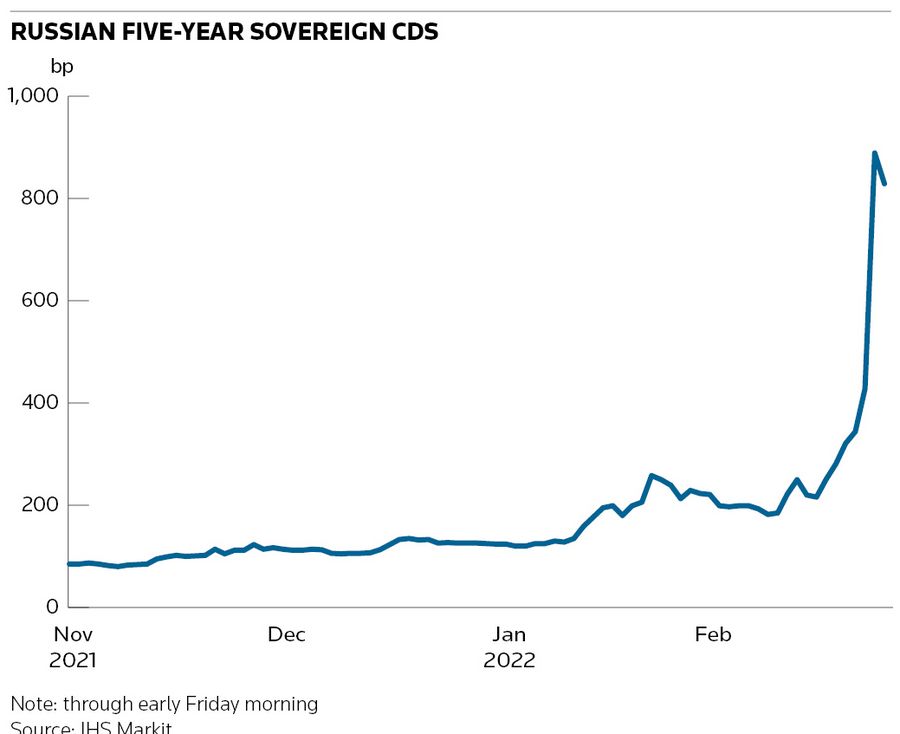

The magnitude of the moves was as shocking as the speed. The spread on Russia's five-year CDS, for example, more than doubled in the space of a few hours on Thursday from over 400bp to over 900bp, according to Markit. By Friday, though, it was back at 456bp.

Damaging

The moves were also big in Ukrainian assets, which a third trader reckoned could prove even more damaging for some investors than the fall in Russian prices. "If there is pain, it will be in Ukraine, I think. It has been consensus long for a while," he said.

Ukraine's GDP warrants fell to a sub-30 cash price on Thursday, according to Tradeweb, after being quoted at 45 at Wednesday's London close. Those securities peaked at over 118 last year. Payouts on those bonds, which were issued as part of Ukraine's debt restructuring in 2015, are linked to economic growth. Ukraine five-year CDS spreads, meanwhile, gapped out by more than 2,000bp on Thursday, from 1,439bp to 3,664bp, according to Markit. By Friday it was back down at 1,769bp, though there is very little trading activity, with positions in the warrants rumoured to be concentrated at a small handful of investors.

Lack of liquidity

Indeed, a lack of liquidity was cited as one of the main reasons behind the price moves across all Russian and Ukrainian assets. "The big thing is the lack of liquidity," said McNamara.

McNamara said the fallout from all the price action may be contained for most because he suspects there isn't much leveraged money exposed. "Leverage is always what turns a nasty day into a major blow-up and I really can’t imagine anyone was leveraged heading into this," he said.

Another source of comfort for investors is that, despite a few fraught hours when it looked like events in Ukraine would spill over to broader markets, the contagion was eventually contained. "From Thursday morning until about three o’clock it was going much broader: Turkish lira, Polish zloty were getting hit. Everything came back after mid-afternoon London," said McNamara on Friday. "Today we haven’t seen follow through. Everyone is trying to get a feel for what everybody else is doing."

On Thursday, global equity markets swung one way, then the other, but the upshot was that by the New York close the S&P 500 and Nasdaq Composite were up on the day. Bond markets, meanwhile, were at one stage pricing in fears of stagflation based on big moves in US 10-year real yields and breakevens but by the day's close the changes were relatively modest. In cash markets, the yield on the 10-year Treasury fell by less than 3bp to 1.96%. By Friday the benchmark note was at 2%, suggesting that investors were starting to put risk back on their books again.

Yet the situation remains precarious. Although Russia remains part of the Swift international payments system and investors can in theory still trade outstanding Russian bonds and shares – for now – there were several moving parts for market participants to digest as a consequence of the various sanctions announced.

Some financial institutions are taking matters into their own hands to manage any risks. Clearstream, for example, on Thursday said that "due to increasing demand from its customers, and in the context of current circumstances" it was excluding trades from Russian entities, in roubles or with Russian ISINs, "until further notice". It also stopped settlement for trades denominated in Ukraine's hryvnia, although the language of that statement was different, saying that trades "cannot be executed for the time being".

Trading halt

Just as dramatically, a number of international banks have halted trading in Russian equities. JP Morgan, Goldman Sachs, Citigroup, Morgan Stanley, Bank of America, HSBC and UBS have all stopped trading locally listed Russian stocks, according to sources familiar with the matter. Spokespeople for all of the banks declined to comment.

Russian stock markets have swung wildly in the two days following the invasion. The benchmark MOEX Russia index plunged a record 33% on Thursday but had rebounded 20% on Friday.

The stock-trading pullback underscores the caution among international banks, with one source indicating the decision came from senior management due to concerns over sanctions. Even though Western governments have stopped short so far of explicitly banning trading in most Russian assets, the US has looked to cut off Russian banks from much of the US financial system by levying sanctions on its largest lenders, including Sberbank and VTB. Such a move makes it harder for Western financial institutions to trade Russian assets given that many will use local brokers to connect to onshore Russian markets such as the Moscow Exchange.

Most banks are still trading depository receipts on Russian companies that are not subject to sanctions, sources said, but won't trade DRs on the likes of Sberbank and VTB. Listing GDRs in London or ADRs on US exchanges is an established way for Russian companies to access a wide pool of international investors, including those that do not typically invest in emerging market stocks.

Seismic decision

The invasion also prompted the Swiss banks UBS and Credit Suisse to stop accepting Russian sovereign bonds as collateral in their wealth management businesses, reported Bloomberg. Both banks declined to comment. The most likely group of investors to be affected would be Russian oligarchs, with Ash describing the decisions as "seismic". He said that "financing conditions are tightening around Russia".

On the other hand, Ash remains disappointed with the sanctions that have been announced so far, which have been mostly concentrated on certain Russian banks, individuals, sectors of the Russian economy and the ability of the sovereign to raise new debt.

"Letting Putin off on Swift, not sanctioning the [Central Bank of Russia] and failing to impose full blocking sanctions on all Russian banks was a case [of] bottling out," he said.

From a bond manager's perspective the most important of the sanctions came from the US Treasury that said on Tuesday that investors will no longer be able to trade new Russian sovereign debt from March 1. "The sanctions so far are relatively benign,” Gustavo Medeiros, head of research at Ashmore, said on Wednesday.

But with so many measures from different governments being announced so quickly, some investors said that it is becoming increasingly time-consuming in trying to work out all the ramifications. "Besides the big price action, a lot of the issues we’re facing now are technical in nature," said Viktor Szabo, an emerging markets debt fund manager at abrdn. "There have been so many sanctions coming out, it’s difficult to reconcile them and we’re having to spend a lot of time working on that with legal experts. There is no clarity over who can trade with whom, who can settle, whether you can trade sanctioned names or have a line with a sanctioned name somewhere along the chain of trade. It adds a lot of complexity."

Last week's sanctions are just the latest steps in measures imposed against Moscow over the years since it annexed Crimea in 2014.

Policymakers will need to be mindful of the impact on financial markets if they push out more aggressive measures, such as banning trading on existing Russian debt or forcing investors to divest their debt holdings of Russia altogether.

That latter measure was applied by the US Treasury to aluminium producer Rusal in 2018 when it became subject to sanctions. “You were toast, as you’d be in breach of sanctions unless you got rid of positions in a matter of days or weeks. The problem was trying to find someone to take the bonds. At one point, a Russian broker was offering a negative price to take the bonds off US investors,” said the first banker.

The situation was only resolved after intense lobbying from other governments and after Rusal's then controlling shareholder Oleg Deripaska, also subject to sanctions, agreed to relinquish control.