Trading in hard-currency Russian government debt has continued this week following Moscow’s invasion of Ukraine, as a number of Western investors opt to accept punitive losses to exit their positions.

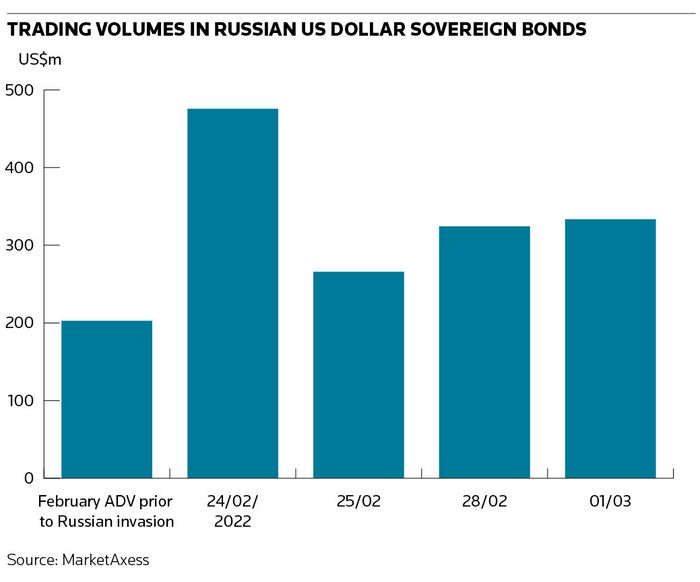

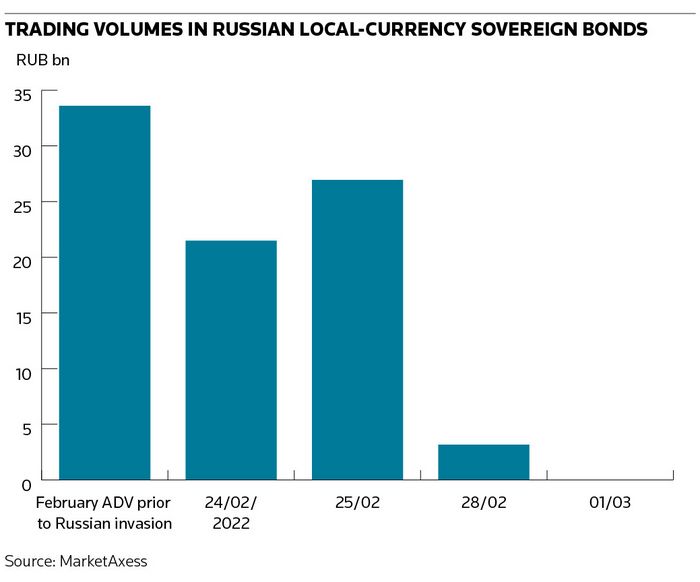

Average daily trading volumes in US dollar-denominated Russian sovereign debt jumped to about US$350m in the first four trading sessions since the invasion, according to bond trading platform MarketAxess, compared with a daily average of roughly US$200m in the first three weeks of February before the conflict. That is a stark contrast to trading in local-currency Russian debt, where deals have ground to a halt following Western sanctions.

Investors and traders report a broad-based rotation from Western institutional investors out of Russian hard-currency bonds, with Asian accounts as well as a handful of global hedge funds and distressed debt funds willing to step in. But trading costs remain extremely high given the yawning gap between where banks are willing to buy and sell these securities in what remains a deeply illiquid market.

“You can trade dollar or euro Russian sovereign paper if you want to get out – but the bid-offer spread makes it prohibitively expensive,” said Simon Hinrichsen, a portfolio manager at Denmark’s Sampension. “We’re hearing there’s been quite a bit of rotation out of Russian dollar debt, with European institutional investors like pensions and insurance companies selling.”

Many investors were quick out of the blocks in dumping their exposure after Russian president Vladimir Putin announced the military attack on Ukraine on February 24. Roughly US$475m in hard-currency debt changed hands that day, more than double the average daily volume throughout the rest of February, as bond prices tumbled.

Sally Greig, head of emerging-market debt at Baillie Gifford, was among those to head for the exit. “We sold all our Russian bonds on Thursday, thankfully. Since then they have collapsed in value,” she said.

Refinitiv data show Russia's US dollar bonds maturing in 2047 were bid at 25 cents on the dollar on Wednesday compared with well above face value in mid-February.

“The markets are in complete chaos now,” Greig said, and she had heard of banks being unable to settle trades they have executed.

Local market freeze

Trading in local-currency Russian debt has dried up following Western sanctions targeting local banks, which have effectively halted the settlement of these transactions. Post-trade firms Clearstream and Euroclear have told clients they will stop settling rouble trades.

MarketAxess data show a measly Rbs1.8m (US$16,280) of local-currency bond trades changed hands on Tuesday – down from a high of nearly Rbs80bn earlier in the month and Rbs27bn as recently as Friday.

“Liquidity is challenging. Local-currency markets have been effectively frozen and hard-currency bonds have been trading sporadically on an order basis or if a trader is set up to do a specific trade,” said Philip Fielding, co-head of emerging markets debt at MacKay Shields.

Sky high

While Western investment banks are reportedly still trading hard-currency Russian debt, investors looking to sell now will encounter sky-high transaction costs. The bid-offer spread on Russian US dollar bonds is around 10 cents (so equal to 10% of the bond’s face value). Investors say banks are reluctant to take risk on their own books and instead are merely looking to match buyers with sellers where they can.

“The way these bonds are trading, the quotes – the level of bid-offers – suggest that if the trader doesn’t have an axe, they won’t give you a price," said Thomas Christiansen, head of emerging market sovereign debt at Union Bancaire Privee. "Liquidity is practically non-existent.”

Investors note that while there is no blanket ban preventing Western banks from trading Russian assets, there remains considerable uncertainty over the outlook given the intensification of the war in Ukraine and potential for more sanctions. One fund manager said there is already no trading in some hard-currency bonds with "RU" (for Russia) in their ISIN – the unique identifier for individual securities.

For the time being, transactions still appear to be passing through the market and could even be set to increase dramatically if Russian debt is ejected from the most widely followed industry investment benchmarks.

“There is still a significant amount of money in the Russian bond market – there will be passive accounts that had to hold it,” said Baillie Gifford’s Greig. “I expect Russia to fall out of the major bond indices soon due to the capital controls. It also starts to be a moral question when you are essentially forcing passive investors to support the Russian government through index inclusion.”