Credit derivatives linked to Russian sovereign debt are trading well out of line with the country’s bonds, a dislocation that reflects concerns that the contracts could fail to work properly if Moscow defaults on its external debt, investors and traders say.

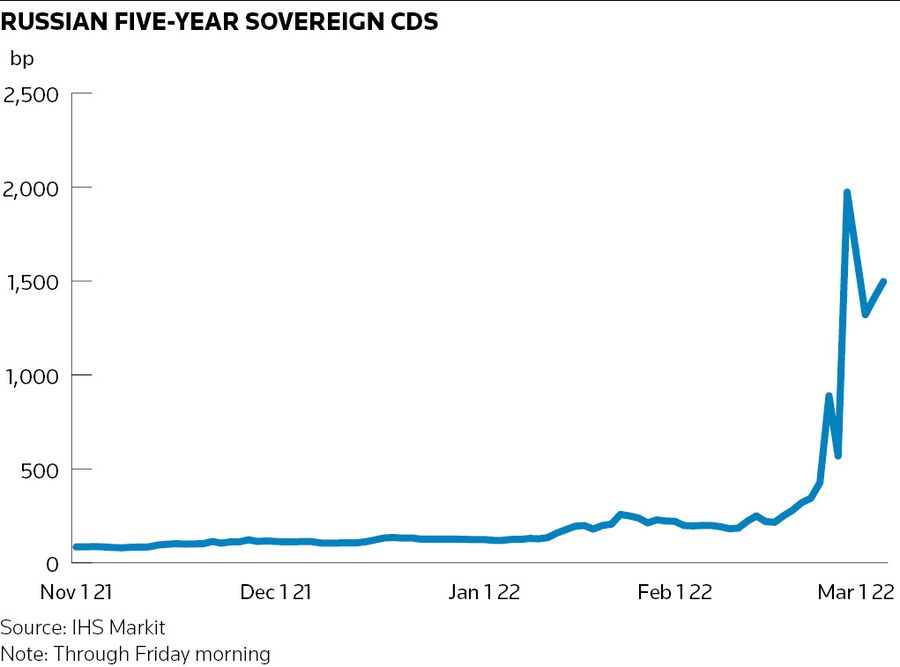

The cost of credit-default swap protection has surged since Russia’s invasion of Ukraine in late February, with traders demanding to be paid around 38 points upfront on Thursday. That means a CDS buyer would have to shell out US$3.8m to protect against a default on US$10m of Russian bonds for five years, with an additional US$100,000 annual fee.

But while those levels may be distressed, they still imply a far higher recovery rate in the event of a Russian default than bond markets predict. Russia’s US dollar bonds due 2028 were being bid at 30% of face value on Thursday, Refinitiv data showed, well below the roughly 60% recovery rate CDS markets imply.

Traders and investors attribute that 30-point disconnect – which suggests CDS holders could be left significantly out of pocket in the event of a default – to concerns that further Western sanctions may hamper trading in Russian government bonds that would ordinarily be used to determine CDS payouts.

“CDS are not trading at the same level as bonds," said Richard Briggs, an investment manager at GAM. "The reason seems to be concern about the settlement of CDS, otherwise CDS should be trading with [a] higher upfront."

"If secondary trading in Russian bonds is banned then settlement of the sovereign CDS could be an issue," he added.

Expectations that Russia could default on its US$39bn of external debt have risen significantly since the country’s invasion of Ukraine. Moscow has more than US$700m of payments coming due this month, strategists at JP Morgan said in a note on Wednesday, with the next relevant coupon scheduled for March 16.

Russian sovereign CDS reference the country’s hard-currency bonds and are designed to trigger payouts to protect holders if Moscow fails to honour its payments or restructures its debt. The JP Morgan strategists estimated there is US$6bn in net notional of Russian CDS positions across the market. In the event of a default, there is a mechanism known as a CDS auction where financial institutions deliver and trade eligible Russian sovereign bonds to determine the size of those payouts.

Ordinarily, CDS and debt markets should imply similar recovery rates for bondholders if a default occurs. The fact that Russian CDS buyers are having to pay far less for default protection than bond market prices imply, shows there is considerable uncertainty over not just the final recovery rate, but whether a conventional CDS auction could take place at all if sanctions prevent trading in Russian debt.

"Russian CDS are being quoted but there are a lot of questions about the settlement process. The most likely event of default is a failure to pay, although a moratorium or repudiation is possible too," said Simon Hinrichsen, a portfolio manager at Denmark’s Sampension. "Given sanctions and uncertainty on deliverables and the settlement process, there is a large basis to bonds driven by this risk."

Hard times

Western sanctions don’t prohibit trading in Russian hard-currency debt as things stand and decent volumes of transactions have passed through the market over the past week. However, investors are worried that could change given the intensification of the conflict in Ukraine in recent days, with an outright ban on trading in Russian debt having the potential to derail any CDS auction process in the event of a default.

Concerns over access to the hard-currency bonds that could be used in an auction are also weighing on the market. Bankers said local Russian lenders and investors hold many of these bonds, most likely limiting the amount of securities available to be delivered.

One emerging market debt trader agreed that doubts over the settlement of Russian CDS in the event of a default was preventing it from trading at even more distressed levels, noting the “universe of deliverables [is] smaller than people think".

Problematic

Strategists at JP Morgan pointed to a number of Russian bonds that could be problematic more broadly. There are six hard-currency euro and US dollar bonds that have fallback mechanisms allowing Moscow to make payments in other hard currencies, and in some cases even roubles.

There are also three securities that are subject to settlement with the Russian National Settlement Depository, which could be a further issue given reports from several banks of a halt in secondary trading of these bonds in recent days. That leaves six bonds with no rouble fallback language that are still tradable, the strategists said.

The rouble “optionality” in some securities “may render these bonds out of scope for CDS”, they added.

The JP Morgan strategists note there is a “waterfall of settlement fallback mechanisms” if an auction cannot be held for Russian CDS. Even so, there would still be considerable uncertainty over the outcome of such a process.

"It's more complicated than a normal CDS settlement,” said Briggs at GAM. “If you can't have physical settlement because people aren't able to deliver a sanctioned bond, you could maybe have cash settlement. But even then you still need to find a level – so what is the price of a Russian bond to settle the CDS? It's complicated."

Additional reporting by Sudip Roy