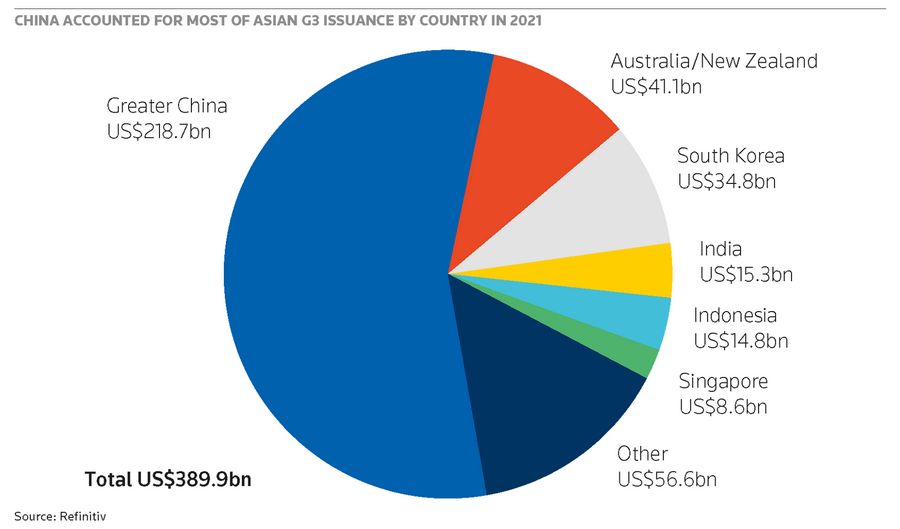

IFR Asia: Asian bond volumes hit a record last year, reaching $432bn, up about 7% from the previous year according to Refinitiv data, but that doesn’t really give the true picture of quite how difficult conditions in the bond market have been. Apart from concerns about when the US Federal Reserve might raise rates and how quickly, there has also been plenty of Asia-centric events that have been moving markets, and most of those relate to China. In March last year China Huarong Asset Management rocked the market by announcing it would be late publishing its annual results, and warned of a potential restructuring transaction.

That turned out to be a white knight investment by state-linked companies but it made markets re-think state support. Then by summer Chinese property companies were struggling and China Evergrande Group eventually defaulted in December. Even now there are more Chinese property companies getting into difficulties.

Chinese regulators have also been clamping down on industries like technology to break up monopolies as part of the country’s common prosperity goals, leaving investors to figure out which kinds of credits could be affected next.

With the 10-year US Treasury yield rising about 40 basis points since the start of the year, issuers and investors have to deal with all these factors as well as a rise in cost of issuance.

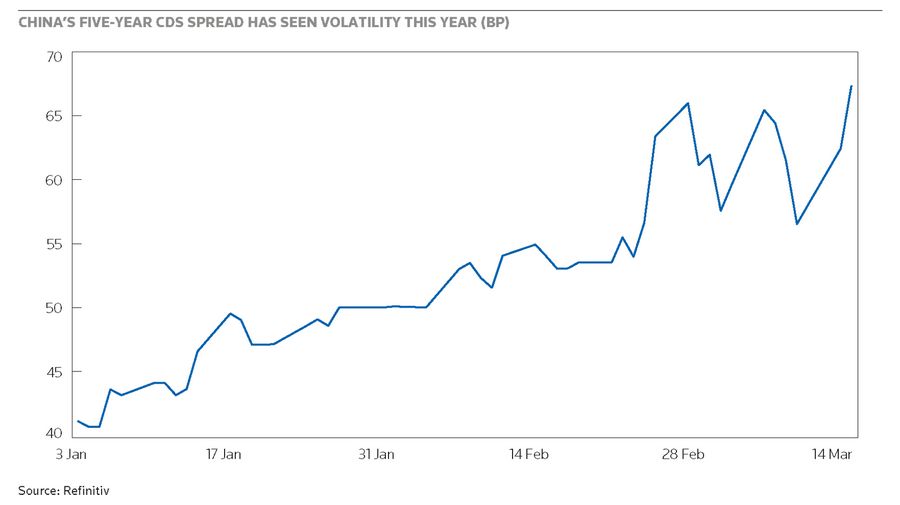

[This roundtable took place on February 22, two days before Russia invaded Ukraine, worsening market conditions further.]

Gary, how will factors like the end of quantitative easing, rising inflation and higher rates affect credit quality for Asian corporates?

Gary Lau, Moody’s: Certainly the elevated commodity prices, inflation pressure and volatile financial market are key challenges facing Asian companies in 2022, putting aside the regulatory scrutiny on certain sectors and also geopolitical risk.

To begin with cost pressure has emerged as the next challenge of the pandemic. The impact on corporate revenues and margins in the region certainly would vary across different sectors. For example, the commodity and raw materials producers such as those in upstream oil and gas or in the mining sector are benefiting from the current period of high prices. Similarly the steep rise in transportation costs has supported the margins of container shipping companies.

On the other hand, manufacturers of goods which depend on raw materials, transportation and logistics services which face capacity shortages, now have the added pressure of high energy costs. Not all the companies will be able to fully pass on the cost increases to the end consumer, resulting in margin compressions.

We also see that supply bottlenecks and input shortages are constraining the production of goods and services in many sectors, such as motor vehicles, electrical equipment and machinery, where a shortage of semiconductors has caused manufacturers to scale down their production. But that said, we expect the supply chain disruption to ease later in 2022.

The post-pandemic economic recovery, the labour market recovery and the current inflation dynamics means that monetary policy of central banks is set to tighten in many countries globally, and strengthen the case for a quicker normalisation of monetary policy than we previously expected.

In our view, the credit impact of a 75 to 100 basis points Fed rate hike in 2022 will be limited if the expected earnings growth of corporates materialises. Many of the corporates (mostly IG-rated) have enjoyed a long period of accommodative market access, and they have locked in low interest rates on most of their debt. The rise in the interest rate will only affect the marginal cost of borrowing. It will take several years before we see a material impact of a marginal rate increase on the average cost of borrowings.

So, in summary, from a credit perspective the outlook for corporate earnings, the margins, the profitability, as well as continued access to funding for refinancing, particularly for high yield credits, will be more important than the impact of higher interest rates for corporates.

IFR Asia: Zhi Wei, normally rising rates are negative for emerging markets, historically, but what EFFECT do you think the rate rise is going to have on Asian offshore bonds?

Feng Zhi Wei, Loomis Sayles: There is really no simple answer. We currently are in the tale of two cycles – China easing and the USA tightening. Within Asia we also have a story of two halves: China and Asia ex-China. In general, inflation pressure for most Asian countries is still manageable. So we would like to break down the Asia offshore bond market by rating investment grade and high yield credits by duration, country and sector.

In general, investment grade is the most vulnerable to a US Treasury hike, especially on a total return basis. But, again, total return for short duration bonds should likely be isolated from a lift-off in long-end rates, and by country and issuer credit profiles.

Some Treasury impact could be cushioned by spread tightening from a credit quality improvement and stronger business prospects for Asia credit. We also see opportunities from risk-adjusted relative value and supply-demand dynamics in Asia. If we have more policy stability or we have more supportive policies, we would also see some opportunities for spread compression from Chinese credit.

Compared to investment grade, I think Treasury movement is less an issue for Asia high yield bond performance. But within high yield, I think those currently trading closer to investment grade level are the ones who will be the more vulnerable to a rate hike, but these are also the strongest names within Asia high yield.

The other asset class that probably will be affected by higher rates is fixed-for-life perpetual bonds, but I would say it is already reflected in the bond prices. Asian currencies could also be affected by a rate hike, but compared to the early years, I think the Asian currencies are more stable now and I do not think a rate hike will result in significant fund outflows from Asia.

I think the least affected by the rate hike will be Chinese high yield property because this sector is trading at distressed levels, and most are trading at more than 10% yield.

Lastly, I think geopolitical issues will also complicate the market. So, in short, I would expect some short-term volatility in the Asia offshore bond market.

IFR Asia: Obviously UOB has got a very high rating and when it issues it pays a low spread. So what effect will the rate hike and withdrawal of fiscal measures have for issuers like UOB?

Koh Chin Chin, UOB: With an improved outlook and the rise in inflationary expectations, generally the market has probably anticipated rate hikes on the horizon globally, and for most countries and central banks to be tapering their asset purchase programmes. However, it is the pace of the tightening cycle that has created a lot of uncertainties, given the rising inflation numbers and the increasingly hawkish tone from the central banks. Investors are currently trying to grapple with the current market dynamics.

Some investors are stepping away on the sidelines, waiting for more clarity. Some investors are expecting higher new issue premiums, as we have seen in the market earlier this year.

Another point about tapering that affects the non-eurozone issuers like us when we issue our covered bonds would be the European Central Bank’s covered bond purchase programme, the CBPP3. This implies normalisation of the artificially compressed spreads of the non-eurozone covered bonds that we have seen, and that will also reduce the relative attractiveness of the non-eurozone paper from the eurozone investors’ perspective.

Looking at the withdrawal of the fiscal measures that were put in place during the pandemic, for example, we talk about the A$210bn Australian term funding facility that expired last year in June, and also the more than €2trn TLTRO3 in Europe that expired in December last year.

Now banks who have had the benefit of drawing down from these programmes will have to find a way back to the wholesale debt markets to refinance, even on a partial basis, to repay these obligations going forward. This normalisation of bond supply will actually push spreads wider over time.

In all I feel that it is a more challenging set of inherent market conditions for issuers, whether or not they are high grade issuers like us. That also explains why issuers globally have been frontloading. As can be seen earlier this year, markets had been really busy and also new issue premiums have been paid. The geopolitical tensions that we are seeing now, such as the Russia-Ukraine tensions, add to another layer of uncertainties for issuers.

Going forward, I believe that the issuers have to be even more nimble than ever to navigate around volatility, market events, geopolitical tensions and to be more considered in the way we assess our true execution risk, given all these structural headwinds.

IFR Asia: Alan, you’re at the centre of issuance in Asia. How have rate expectations changed the usual front-loading approach for Asian issuers?

Alan Roch, Credit Agricole: When you think of whether to recommend an issuer to frontload its issuance or not, you think of the risk factors and rates really comes as factor number one. When you go back to the end of last year, the market was expecting two-plus hikes from the Fed across 2022. Now the consensus is that they hike pretty much at every meeting this year. That is a step change in a very short period of time and it argues for trying to frontload and to come ahead of that wave.

That obviously has had a big impact on term dollar rates as well, 10-year Treasuries moving in a 50 basis point range. It is obviously causing uncertainty as well in the investor community. At what point do they come in and buy the market? Is 2% for the 10-year Treasury the right number? Is it 2.25%? Is it 1.75%? You have seen pretty much all these outcomes in the last six weeks.

Euroland which was a beacon of stability in the past has really witnessed a lot of volatility as well with 10-year swaps moving pretty much within the same 50 basis points range, which was even more unexpected.

The greater hawkishness of central banks has caused a lot of uncertainty and, therefore, the only way you can really pre-empt that is by trying to come to the market as early as possible, even if that means there is some new issue concession.

Added to the mix you have geopolitical headwinds. It really goes to show that it is very difficult to predict how geopolitical events may unfold, in particular, with the one that is ongoing in Ukraine at the moment.

From our perspective we are pleading for a cautious approach for issuers that are deal-ready and have financials and documentation ready. Our advice is to take a close look at the market. That applies pretty much to everybody in investment grade, and for those who are in the high yield space, of course, it is more idiosyncratic. Yields still remain quite elevated, so that recommendation probably doesn’t apply to everybody in that sector but in investment grade it really does.

The last point though is to retain some flexibility. What we have seen within a given market is one day sentiment can be really poor and on the next day sentiment can be very strong. The ratio of go/no-go calls quite often ends up in no-go, and that can be frustrating to issuers but we would recommend to have a little bit of flexibility within a given window to ensure executions are timed perfectly.

The final point I would make is there is a first mover advantage when the market does open up. We definitely would recommend to seize and grab that market window and get ahead of the curve.

IFR Asia: Obviously China is a pretty big influence on the Asian credit market. How is the China common prosperity drive and the regulatory crackdown on sectors like technology affecting credit?

Gary Lau, Moody’s: A lot of the themes of common prosperity that we have seen in the national policy so far have focused on addressing longstanding issues related to housing affordability and the burden of after-school tutoring on children and parents, with the aim to reduce the financial burden on general households, in particular younger couples given the low birth rate in the country.

We also see specific policies to curb anti-competitive behaviour in the internet platform area which has grown rapidly in the last decade, with clear market leaders in a number of segments.

The tightening regulations relating to the property and education sectors have certainly resulted in significant negative impact in terms of a major shift in the operating and business models for most companies in the education sector. For the property sector we see tightening funding access and, subsequently, financial distress for a number of property developers nowadays.

For the tech sector, let us focus on the internet names. The tighter regulations have definitely raised uncertainty which has been negative. The impact of regulation has been to slow down internet companies’ revenue growth by limiting their ability to increase market share through mergers and acquisitions. Their Ebitda margins will also contract because the new regulations that encourage competition will push those companies to raise investment in developing new products and services, and marketing spend will also rise.

One question we may want to ask is whether the worst is over in terms of regulation of the internet sector. We believe the tighter regulatory stance is here to stay because in the last two years-plus of the pandemic, online services and products have become an increasingly important part of China’s consumption economy. That is probably why the regulators need to assert more scrutiny, particularly on the leading, large internet platforms. But there could also be more, but not necessarily new, areas of focus: for example, correct and appropriate content relating to the protection of minors, the protection of workers’ welfare and rights, and how companies treat and use the consumer data they collect online.

Despite all these challenges, we see the rated internet companies have a very strong financial buffer and are mostly in a net cash position to absorb the negative impact in the near-term. They also have experience of dealing with regulators and instituting changes as required.

So the near-term impact should be manageable. However, there could be changes along the way in areas that were touched upon previously, which we will closely monitor.

IFR Asia: Zhi Wei, what do you think will be the impact of Chinese policy measures and regulatory changes upon the Asian credit market?

Feng Zhi Wei, Loomis Sayles: I think the keyword so far is uncertainty. As an investor we really do not like uncertainty, whatever kind of uncertainty it is. For the Chinese credit market now, I think the policy uncertainty is really a key issue for every investor now, be it in the tech sector or the property sector.

Even if the policy intention is good and it is for the long-term benefit of the sector, the issuers and the people, uncertainty is not good for investors in the short-term. It really affects market dynamics and the investors’ views. Taking the Chinese property sector as an example, we have the longest, restrictive measures, in terms of policies, since about five years ago. Each year we were wondering if there would be some relaxation, but it didn’t happen, and actually the policy or the measures are getting stricter each year.

In mid-2020 we started with the three red line ratios to restrict the developers, then we moved to the lending cap for the banks, and then we have the centralised land auction for the local governments. They want the developers to have better credit quality. They also want to reduce the leverage in the system to the property sector.

That is a good thing in the long run, but I think execution-wise, there is some issue and the good policy intention does not translate into good results from the property sector. For the very capital-intensive property sector now, it is in a liquidity crisis.

Since last year we are more frequently looking at credit events or defaults. That is why, when you go into the market, nobody is looking at every developer’s three red line ratios, we are talking about liquidity, and whether they can survive.

The property market is not functional in a normal way. In addition to that, because of the rumours and social media, there is no trust between the investors and the issuers. I think the investor confidence and trust has gone. Looking at it now, I would think the offshore new issuance market is totally shut for the Chinese developers.

Policy for the tech sector is totally different. Tech companies are in good, strong liquidity positions and have strong credit profiles. But I think that kind of uncertainty has still affected investors’ confidence in those tech companies, and eventually all those uncertainties will also affect their credit profile in the end. It will take time, but it will happen if the uncertainty continues.

In summary, with the uncertainties on different policy fronts, the new issuance market would definitely be muted especially for the non-SOE Chinese companies, and in the longer-term it will have a credit impact.

IFR Asia: Obviously UOB is first and foremost a Singaporean credit but how does it affect UOB when there is uncertainty around China and volatility in Chinese credits?

Koh Chin Chin, UOB: The potential debt default around the Chinese developers and the regulatory crackdown indeed weakened the onshore investor sentiments in China. For our Panda bonds issuances into the onshore market, as well as the onshore financial bonds issued out of our subsidiary, our primary investor market is really the bank treasuries where we understand that they do not buy into such high yield issuances issued by the private property companies.

The asset managers and the insurance companies are not really the primary investor base for us in this market because of the higher absolute yield hurdle that they expect, and also their preference for longer duration, beyond three years, when three years is probably our tenor sweet spot.

In the offshore markets the sentiment was similarly affected: credit spreads widened, liquidity conditions tightened. However, investors in this market do not directly compare between a Chinese credit and a Singapore credit.

Despite that, in our annual roadshows where we meet our investors we have always been talking about such topics in a very comprehensive manner about our credit profile. Nevertheless, during such times, we do get investors coming back to us, asking for more updates on our potential exposure to such companies. They would like to ascertain whether there is any second order contagion effects on the investments.

As UOB is predominantly deposit-funded and we have access to the other funding markets we have that flexibility to navigate around such market volatilities. During such times we had the flexibility to stay out of this market, or alternatively if we really want to tap the market we can always go for the more insulated markets such as the Aussie bond market or the covered bond market.

In short, the Chinese volatility had very limited impact on us. However, some people ask me, “So do you benefit as a Singapore credit when investors are diversifying away from Chinese credit?” I will say no. Investors have essentially gone and re-focused attention to markets like India and to a certain extent South-East Asia because the yields of Singapore credits are still viewed as too tight for such investors.

IFR Asia: Gary, Zhi Wei touched on this but what do you think the outlook for defaults is going to be this year?

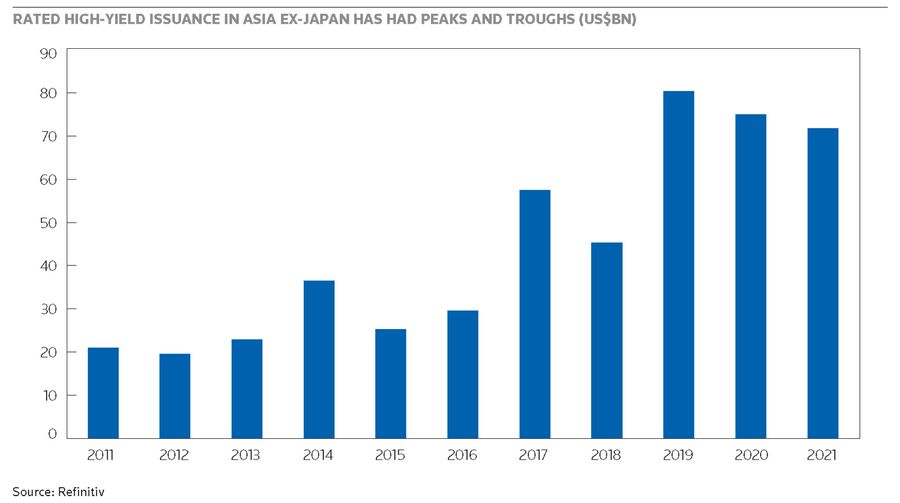

Gary Lau, Moody’s: What we expect is that the high yield default rate in Asia will remain high, similar to what we saw in 2021. The weakened access to debt capital markets reduced issuance and increased refinancing risk for a number of financially weakened companies, particularly Chinese property developers in the high yield space.

In our rated universe, the share of debt on the B3 negative list, which is at the lowest end of our ratings scale, has remained high since October 2021, largely reflecting a difficult operating environment and tight funding conditions for the Chinese property developers. They made up around 50% of the list at the end of 2021, compared with just 3% a year earlier.

We forecast a high yield default rate in APAC of about 6.2% level in 2022. This is slightly lower than the 7.4% trailing 12-month rate at the end of 2021, but higher than the pre-pandemic level and the average level of 3.9% for the past 10 years.

The default forecast reflects our expectation that the global and Asian economies will continue to recover steadily, and the monetary policy will change from accommodative to neutral stance. But it also reflects that Chinese property companies will remain under pressure with high default risks. Already, in January this year there were four reported defaults in Moody’s rated universe and they were all Chinese property developers, mainly in the form of distressed debt exchange, which by our definition is a default.

One of the trends in 2021 defaults in the region was that a large proportion of the defaults were payment defaults. But in 2022, the year-to-date defaults supported our expectation of a rise in distressed exchanges. It is more difficult to predict a distressed exchange because in addition to ability, it also comes down to the willingness of the issuer and the intention of the company to preserve liquidity by extending maturity date to avoid default, rather than to honour their repayment obligations on time.

In summary, our estimated higher than global default rate in Asia is due to the distressed situation in Chinese property sector which accounts for a large part of the rated high yield portfolio in the region. However, we expect the remaining portfolio will track the global trend.

IFR Asia: Looking at the primary issuance side, what do you expect the issuance volumes will be this year, and which countries or industries do you expect to be particularly active?

Alan Roch, Credit Agricole: With the start we have had I think it is hard to make any other expectations than a decrease in volumes versus last year. We are down, quite significantly, so far this year, about 30%. That is in contrast with other regions, as US investment grade is flattish and euros are up. So we are definitely undershooting.

We do think there will be a catch-up from the weak start of the year and we will probably end up 10%, 15% lower. The reason why we are quite optimistic is we have got to keep in mind that the absolute terms of funding in dollars or euros remain super compelling. Paying 10 basis points more new issue concession here and there against a steepening of the curve or higher yields isn’t going to change the fact the markets remains attractive in terms of levels. We still have, from a historical standpoint, a market in which it is attractive to fund. Even the large corporates did quite a lot of pre-funding in 2021 and we think they will be likely to continue to do some pre-funding in 2022. We do think there will be a catch-up in supply but we do think we are going to fall short year-on-year versus what we scored last year.

In terms of other variables in the outlook I think one of the big considerations is duration. It has been harder this year for issuers to get duration in Asia. About 10% of the supply in Asia, so far, has been over 10 years. That is in contrast in the US, where you have had regular 20-year and 30-year deals. But once the market stabilises we will see issuers, sovereigns, strong corporates accessing that lifer bid across the region and into duration. The duration play at the moment has been to favor short-dated transactions and FRNs – more defensive maturities in the face of central banks which have been much more hawkish. We do think that the bid for duration will return once the landscape for interest rates stabilises.

The other variable is the pattern of issuance – markets closes, markets opens. We are going to see lumpy issuance, and that will affect volumes and new issue concessions. When the market is open you tend to see five or six borrowers at a time.

At the moment for transactions which are short-dated, ie, up to five years, usually concessions are anywhere from flat to 10bp. For 10 years they are anywhere between 10 to 15 basis points and they can be higher in the longer end. So they are higher for our region compared to historical averages, but, again, they have to be put in context of rates which remain quite low.

When we think of the outlook and markets which are choppy, we need two things. One is a greater engagement of issuers and investors in private placements. For those issuers that are specifically sensitive to new issue concessions or publicity coming in the public markets, then private placements can be a very good alternative for them. We have seen a very strong dialogue, and perhaps more so than in the past, around private placement products.

We think you will see private deals being struck at a greater frequency than in the past for a greater volume. For non-G3 currencies and local currency deals you can have arbitrages, and as the basis market dislocates then you will see issuers hunting for these sort of transactions, and particularly in the investment grade space. Lower volumes in the public market probably means also greater volumes in PPs, as well as in non-G3 currencies.

From a country perspective and topology we think ESG is obviously going to be a major theme across sectors, across jurisdictions, across ratings, and while that is not new, that will continue to accelerate. And within countries, Chinese corporates, we expect issuance will reduce somewhat, lesser M&A activity. They will continue to do the refinancing but there is less reason to do offshore transactions than perhaps in the past.

Also the PBoC has been cutting rates onshore so these issuers do have very good funding onshore and that gap between onshore and offshore probably favours onshore financing. So we think volumes there are going to reduce. However, for China FIG, the G-SIBs will start TLAC issuance probably in the second half of the year so we do think there will be greater volume of issuance coming from that sector. Otherwise, in other regions, we are calling for fairly similar volumes in South Korea or South-East Asia, and from sovereigns.

IFR Asia: Chin Chin, you mentioned funding in some different currencies but how do you look at the 144A and Reg S markets? Do you see any particular differences in the investor bases there?

Koh Chin Chin, UOB: Our objective to assess the 144A market primarily is from the investor engagement angle, with a long-term view to build a diversified global investor base to deepen our market funding capacity. So while we can test opportunistically and conveniently in the Reg S market for funding, we still prefer to engage the US dollar market through the 144A format on an annual basis, subject to market conditions.

However, there are times where it is not practical for an issuer to continue to stick to the 144A plan in a volatile market environment where you have a 135-day restricted market window, and when there is huge market volatility you do not know when you can actually access the market. So if you go beyond the 135 days window you will incur more costs, but more importantly, more time is needed to update financials and conduct further legal due diligence to extend the issuance windows.

A case in point was in 2020 when we experienced volatility throughout the most part of the year. Finally in September we decided that we should just offer our US dollar Tier 2 offering in Reg S-only format to achieve our deal-specific objectives.

If you are looking for larger prints and want added insurance given the difficult market environment and the fact there could be much smaller investor demand in the Reg S market because investors are still on the sidelines, it is good to be able to access the 144A market, given the depth of the market.

Other considerations that we have usually will be what is the intended objective of the planned issuance? What is the target audience and the key messaging? One good example that I can share was the US$1.5bn sustainability bond that we launched last year. We set up our sustainable bond framework in March last year, and we wanted to engage the global investors to share our sustainability strategy, our ESG profile and the progress that we have made on this journey. We deliberately structured a dual tranche senior Tier 2 144A/Reg S format to maximise the investor coverage across geographies, and also across the key investor segments.

Senior and Tier 2 are the two relevant products for our 144A investor base, while AT1 will continue to be a Reg S product. In terms of the Tier 2 market, US investors used to be more receptive to a 10-year bullet structure unlike the Reg S market where they are receptive to the 10-year non-call five. However, in recent years we have seen convergence on that as witnessed in last year’s sustainability bond issuance and also other market transactions.

Both markets have the typical investor segments such as bank treasuries, the asset managers, the pension funds, lifers, and money market funds. However, if you look at the depth of the investor base, we will be able to expect a larger consolidated ticket size in the 144A market coming from an asset manager where they have US-domiciled funds.

The other interesting investor base in the US is municipal funds. There is also the corporate cash pool from the tech companies, and increasingly pharmaceutical companies, where they have accumulated sizeable cash resources. Private bank investors onshore in the US typically do not gain bond exposure through the direct primary market, but rather through managed funds, unlike the Reg S investor base.

However, in recent years we have seen PB demand in the Reg S market decline, partly because of the less attractive bond yields versus the equity market during the low yield environment.

IFR Asia: Alan, you must have a good view of the Asian investor base. How do you think the investor base has developed in recent years?

Alan Roch, Credit Agricole: The first thing to keep in mind is the investor base for our product has considerably grown in recent years. It is considerably deeper than it was only two, three years ago. That being said, in the last couple of weeks and months we have seen transactions benefit from a bid which is closer to home, a bigger emphasis on local demand. We have seen this in, for example, China deals and the China bid and we have seen that pattern in other jurisdictions as well, which is understandable. When there is a little bit more volatility there is always value in keeping a bit close to home.

The other point is that issuers that have done consistent investor work in the last few years have managed to build an extremely good investor dialogue. In the current market environment there is a big differentiation between those issuers that have done that work in the last couple of years versus those that, perhaps, overlooked that aspect of that execution.

The large and best in class issuers do have access now to the Asia dollar liquidity pool, the global dollar liquidity pool in the 144A market, and the euro markets. That ability to access the largest pool of liquidity provides issuers with choice, and choice in the current market environment is a great luxury.

From a short-term technical standpoint, investors are keeping high levels of cash or a higher cash balance than usual. We have seen that in our survey and in some asset classes, in particular high yield, there has been some outflows. So the technical bit isn’t that strong today but that obviously will turn at some point, and then cash will need to be invested. We mentioned earlier the absolute level of issuance this year is probably going to be lower than it was last year, and you have coupons and redemptions.

That technical picture which today is negative but will be an advantage as we progress in the year.

IFR Asia: Looking at the Asian investor base from a different angle, Zhi Wei, how is the secondary liquidity situation these days for Asian bonds? Does it make sell-offs worse when there is thin liquidity?

Feng Zhi Wei, Loomis Sayles: Liquidity in the secondary market has been very, very challenging since mid-last year, but it is for a variety of reasons within different market segments. I think broadly for investment grade it’s demand, especially for duration, in both primary and secondary markets that is the main factor for liquidity, because of the US rate hike.

In terms of high yield, Chinese high yield probably has the most deterioration in secondary liquidity, since mid-last year. The sector has witnessed extreme swings in levels on an intraday basis. We have a lot of news reports, whether fake or real, affecting the individual credit perspective on an intraday basis.

Going into the end of last year, it became a sector issue. With that kind of intraday volatility it can be in both directions. Sometimes you have a bond going up in the morning and then when London opens the bond will go down when the sellers come.

The intraday volatility is high in addition to the already very weak liquidity. There is a kind of investor fear of sectors like China property high yield with all those large intraday price movements. This volatility together with the investor fear makes it very, very difficult for dealers to pick risk, so that is another layer on the liquidity impact.

If you are looking at Chinese high yield property, now we have a price curve instead of a yield curve. You have prices going from the 80s and 60s to the 20s and the teens. When the price moves the holders’ profiles will change, which also affects secondary liquidity. So combined, I would say we are in a circular flow of illiquidity at this moment. For liquidity to be improved, we need to have reduced market volatility, or reduced uncertainty for the market. Then we need the new issuance market to reopen, and then we will see an improvement in secondary liquidity.

IFR Asia: We will talk in more depth about the Chinese property sector in a minute but Chin Chin looking at the local currency markets in Asia, have you seen those deepening recently?

Koh Chin Chin, UOB: Let me touch on the key South-East Asian markets. Generally the issuance activities in Singapore, Malaysia, Indonesia and Thailand over the last five years have largely been stable. Government and FI issuers continue to dominate the domestic issuances, and the higher government supply for infrastructure financing offset the decline in private sector issuances due to the pandemic.

The Singapore dollar and Malaysian ringgit markets are relatively more mature. About 15%–30% of the issuances are in the subordinated bond format but that is to a much lesser extent in the Indonesian rupiah and Thai baht market. All the typical investor segments are present in these markets, but there is a very limited investor universe that can invest into the subordinated bond space.

Despite the fact that these markets are not growing in a material way over the last few years, however, we do see very encouraging developments, that we believe will propel further developments of the local currency markets. For example, in Singapore we are seeing a growing ESG issuances it jumped from less than S$700m over the last few years to about S$4.2bn last year.

There are also efforts in the industry to leverage on blockchain technology to digitise the bond market. This is starting with the bond market processes such as post-trade demonstration, hoping to minimise operational risks and expedite the settlement frequency, and with the eventual view to build a robust digital capital markets infrastructure that can support Singapore’s aspiration to become a regional hub.

We believe in ASEAN’s potential and therefore we believe that these local currency markets will continue to grow and deepen over time. We hope that the local authorities will continue to enhance their market infrastructure, reduce the time to market for market participants, improve the issuance activities in the primary market and also deepen the secondary market liquidity.

IFR Asia: Last year was a pretty awful year for a lot of high yield China property developers. Gary, do you think credits from the Chinese property sector are in for more problems this year, or is it possible they can benefit from supportive policy moves?

Gary Lau, Moody’s: Investors’ weak confidence and risk averse sentiment are overhanging the property sector. Despite some signs of policy easing in the sector, we expect the financial and liquidity profile of the rated developers to remain under stress, particularly those lowly rated names.

The overall policy direction remains tight and the policy target of “housing is for living, not for speculation” will remain unchanged. We have seen recently the lending to developers and home buyers has been relaxed, together with lower down-payment requirement and mortgage interest rate in order to support the declining sales in the broader market. However, investor sentiment remains weak and risk averse sentiment prevails particularly in the offshore bond market.

Traditionally January is a very active bond issuing month for property companies but this year, in January, we have only seen US$700m offshore bonds and US$1.3bn-equivalent onshore bonds issued by our rated property companies, the lowest level in the last 10 years. So this tight funding and liquidity situation hasn’t turned around, despite the government providing some easing policy.

Among the relaxation measures, the standardisation of control over the cash in the escrow account at project level is still developing. It could potentially return some more control and give the developer some more flexibility in mobilising cash at the project level, but we do not expect substantial cash to be released for debt servicing at the holding company level because the primary objective of the government is still to ensure timely delivery of pre-sold residential units to the homebuyers.

We also see the government coordination for buyers with a state-owned background to buy assets from distressed developers, but these state-owned enterprises are selective and mostly will act in a commercialised manner, so our expectation is that it will take time for a massive asset disposal to materialise. We also do not expect the government will ask state-owned companies to bail out individual distressed property developers.

There are a large amount of bond maturities in the next six to 12 months: around US$40bn in offshore US dollar bonds and also around US$30bn-equivalent onshore bonds for our rated property developers. The majority of maturing bonds are issued by high yield names so refinancing risk is still high and we will not be surprised to continue to see defaults, including distressed exchanges, in the next few months.

IFR Asia: Zhi Wei, there is a big maturity wall for Chinese property developers this year, so what do you think the chances are of them being able to refinance everything?

Feng Zhi Wei, Loomis Sayles: Looking at the current market situation and what we see day in day out in the headlines, it is difficult for them to issue and then refinance.

Offshore investors have no trust, no confidence. So I think if they cannot issue what can the developers do? They are fighting for survival. They need to live first before they can think about any other things.

That is why you can see in the past few months we see a lot of exchange offers and maturity extensions. The developers will be trying to extend maturities from this year to next year, but that only kicks the can down the road. That will not solve the problem because the obligation is still there.

I think investors are now more receptive of exchange offers compared to the early days. When, for example, China Fortune Land or even Fantasia tried to do an exchange, people may not have been really receptive, but now I think investors are more realistic about the market.

We also know how bad the situation is for the developers to refinance. There is no other better choice compared to an exchange offer to avoid a hard default. That is why I think we still see the exchange offers going through. Going forward, whether they exchange or not, using cash to pay every liability is not normal for any business.

We will need to have the refinancing market open for the developers. Both the onshore and offshore refinancing markets need to open, but we are looking for a couple of signals first. Number one is the asset disposal for the developers or for M&A transactions to go up to a meaningful volume, and also at a reasonable price.

Meaningful M&A will help the developers generate some cashflow, and reduce immediate debt. The other thing is the sales market needs to recover. Sales is the main cash generating source for the developers, and if the sales are down they still need to pay their opex, their capex, their tax, interest, and everything.

We would also like to see them normalise the use of proceeds from sales, so we can see their escrow accounts, and know which cash is restricted or which is not. Even so, say, ensuring project completion is the key for the government.

We will need to see onshore refinancing markets open for the developers. In the early days, other than project financing or construction loans, the developers had access to onshore bonds, ABS, trust loans, and wealth management products.

We have news that the onshore market is opening to the SOEs, so I think whether they will open to the POEs, the private developers, from the stronger ones to the provincial ones, is another signal we need to monitor.

There is still a long way to go for the offshore refinancing market to open for developers at this moment.

IFR Asia: Gary, if Chinese property companies keep having problems, is there a spill-over effect to the rest of the Asia high yield market?

Gary Lau, Moody’s: We already see the spillover impact. The Chinese property developers are the largest group of issuers in Asia high yield space and account for nearly 70% of the total issuance over the last five years.

With the turmoil in the sector, the high yield issuance is shrinking. In 2021 we see less than US$30bn in our rated universe, down 23% from 2020. Investors are shying away from the Chinese developers. We see such negative sentiment extended to other high yield companies in the region as well.

January is usually a strong issuance month in the offshore market, but what we have seen is only two tap issuances in the month. A few new high yield issuers in the region, outside China, who were looking to launch bond issuance but decided to put it on hold due to pricing and weak market sentiment. We believe this situation will continue for a little while and increase the refinancing risk in the high yield portfolio.

Overall the impact is obvious, not only for refinancing risk but also rising funding cost. No doubt the Fed rate hike is one driver, but investors also demand a higher risk premium due to the volatile market conditions, looking for higher yields and shorter tenors.

On the other hand, the slowdown in supply from the Chinese property sector could potentially open the door for companies from other countries to come to the high yield US dollar bond market when the market conditions stabilise.

IFR Asia: Are the clouds from the Chinese property sector hanging over the rest of the Asian high yield sector and making it hard to issue?

Alan Roch, Credit Agricole: When you hear the words missed coupon more often than you hear the words initial price guidance then for sure it has got impact on the investor psyche. So the clouds are definitely still there.

All these liability management terms and extensions are drawing so much time and effort from the investor community, and they are extremely important decisions for the investor base to get right. If you want to generate performance in 2022 in your high yield portfolio getting Chinese property right will be absolutely critical. So that is drawing a lot of energy away from the new issue markets.

In our view we are not too far away from a market outside of China property re-opening. We actually have seen some transactions so far this year. I think the recipe book for these deals is quite simple. You need to keep it quite short, at least, at the moment, and you need to make sure that covenant packages are really well thought through. That sounds like an obvious thing to say, but we have seen covenant packages being lighter and lighter in the last couple of years. I think the ability to compromise on these today is nil.

We do feel there will be more transactions out of India which is now the second largest high yield market in Asia, and has a big renewable story there. Indonesia has a few names which the investor base is very comfortable with. You have also names outside of Asia, and then within China itself the renewable story, the tech story, the datacentre story.

All of these are worthy of a lot of investor interest. When these clouds, which are very present at the moment, start to drift away, these conversations will begin in earnest, and the price or the cost that is required for these issuers to come to market will reduce accordingly. There are reasons to feel a little bit more optimistic in the months to come.

IFR Asia: Let’s talk about something a bit more optimistic that is growing: ESG issuance. Zhi Wei, how do you see the ESG bond trend continuing this year?

Feng Zhi Wei, Loomis Sayles: ESG is really the hot topic and the only certainty for demand.

I think we will see growth in issuance from ESG bonds in this year and going forward. ESG issuance is also a very demand driven process, currently, for investors. Funds that focus on sustainability are gaining more and more attention. They also play a very important role in terms of integrating sustainability factors into portfolios, and encouraging companies to incorporate ESG elements into their business plans.

Companies are talking to us, and they want to know what they can do to improve their ESG presentation. When we embrace sustainable investing from our end, there also needs to have some internationally recognised standard to check accountability from the issuers. For example, we need to vet the companies, like their carbon emissions and screen them from their ESG compliance and also disclosures.

When the market is growing we also have the rising concern of greenwashing. Investors, regulators and the general public, need to see and track how companies act on their plans. Companies will need to set executable goals and also be transparent about all this.

On the one hand we expect to see more interesting investment opportunities with continued growth in ESG bonds. On the other hand, we will need to preserve the legitimacy of this financing instrument.

IFR Asia: Gary, do companies with high exposure to ESG risks face difficulties in the credit market right now?

Gary Lau, Moody’s: The answer isn’t very clear cut because the implication can vary significantly across different markets and different sectors. But no doubt, ESG consideration is becoming more important for issuers, investors and also rating agencies like Moody’s. Last year we started to roll out our ESG score for rated entities.

We have two sets of scores. We first assign what we call issuer profile score to assess the E, S and G exposure separately on a five-points scale, from very highly negative on a score of 5 to positive exposure on score of 1. We also assign a credit impact score, again on a five-points scale, which is an output of the rating process that more transparently communicates the impact of ESG considerations on the rating.

Assigning ESG scores itself is not going to change any rating, because ESG is always part of the considerations embedded into our rating assessment. We just provide more granular view on the exposure and credit impact of ESG on a rated entity.

From a credit perspective the net zero carbon emission goal will continue to raise pressure for decarbonisation across different industries. Some sectors we see already undergoing a rapid transition in certain markets while others are under mounting pressure to articulate a trajectory to net zero emissions. Gathering momentum behind the energy transition has intensified, putting the spotlight on longer term credit challenges, especially for the hydrocarbon industries.

We have also seen increasing awareness from issuers in those high carbon emitting sectors such as steel or cement, through their own articulation of the path towards reducing carbon emissions, if not carbon neutrality, and issuing sustainability linked notes or bonds through their commitment to sustainable productions and better disclosure. The impact varies. For example, the coal mining and oil and gas sectors in China and India may not face imminent financing pressure considering the government support, the booming demand and the sufficient support from the domestic financial markets.

However, in the longer term the pressure to reach net zero targets will grow for companies from China and India. The policy easing now could mean stricter requirements and higher costs to transition in the future. Eventually Chinese and Indian companies from fossil fuel driven sectors will face higher transition risk and credit pressures.

In other markets like Indonesia where the domestic financial markets are more limited and depend more heavily on foreign funding, the issuers from this sector will face more near-term funding pressures as global investors are accelerating the decarbonisation of their portfolios.

While some Indonesian coal companies were still able to raise new bonds and loans last year, we expect their access to credit, especially from international market, to decline over the next few years as global initiatives like GFANZ grow in popularity, and an increasing number of financial institutions or fund houses announce restrictions on lending to carbon intensive sectors, such as coal mining.

Generally speaking, over time we expect investors will become more vigilant when taking exposure to issuers with high ESG exposure, especially those in the high carbon-emitting sectors.

IFR Asia: Chin Chin you mentioned the big sustainability bond last year, what kinds of questions are investors asking now? What kind of disclosures are they looking for around ESG?

Koh Chin Chin, UOB: There have been several forces at play in relation to this topic that are collectively driving all of us to a common goal of promoting more transparency and more robust disclosures in the sustainable finance market. A few years ago issuers probably anticipated a trend where ESG would become a hygiene factor for everyone and not just for the sustainability focused investors. Issuers including ourselves have been proactively engaging investors to share our sustainability strategy or ESG profile and what we are thinking and how we intend to walk this journey.

We also tried to adopt the best practices in terms of voluntary disclosures, such as the recommendations of the Task Force on Climate-related Financial Disclosures in addition to the current mandatory reporting requirements which vary from jurisdictions.

The industry has also made an effort to improve on the impact reporting but the problem is that the fast pace of growth in the sustainable finance market has created room and concerns in regard to potential greenwashing. Investors and regulators will definitely demand more transparency on this front and rightly so.

Progress on better disclosures at the same time is also being accelerated by regulators worldwide. For example, EU companies are required to adopt mandatory reporting under the EU taxonomy regulations on environmental objectives in 2030 and investors are asked to adopt a phased-in approach to comply with the sustainable finance disclosure regulations by the same year as well.

What this means is that EU investors will be increasingly screening all investments against the EU taxonomy, and to disclose what percentage of the funds mix is in compliance with the EU taxonomy, because non-EU issuers are currently not within the scope. EU investors will have to, eventually, request issuers to provide gap analysis or otherwise they may be leaning towards replenishing maturing investments with the EU taxonomy aligned formats that will allow them to avoid the hassle of doing the gap analysis to facilitate their own disclosure requirements.

Different jurisdictions are also developing their own domestic green taxonomies: for example, Singapore, Korea, Indonesia and so on. If the capital is only mobilised onshore, that is not a problem given that the domestic green taxonomy will serve its purpose. But there has been increasing interest and also a willingness to mobilise capital across borders. So we believe that investors will be looking at the need for green harmonisation in terms of standards and redefinitions.

The international platform for sustainable finance has formulated a draft of Common Ground Taxonomy which compares the EU criteria and the Chinese criteria and that is, primarily, because these two markets are two of the largest green financing markets. I suspect that the common ground taxonomy will also be used eventually to broaden the global harmonisation efforts.

The International Sustainability Standard Bond has also been announced, following COP26, to streamline global sustainability reporting. So in all I think all these forces are coming all together to drive more robust disclosures and transparency.

Alan Roch, Credit Agricole: I would like just to respond on a comment Chin Chin made on harmonisation, because I think that is a really important point. Harmonisation and standardisation are two super-important points for that market to continue to grow.

Very recently we have had the publications of official taxonomies. We have had a China taxonomy in November last year, Korea in December, common ground taxonomy in November as well. So plenty has happened in the last few months and I think that is really going to boost the growth of this market, and obviously the green market is very mature in Asia. But as to the extent of the growth there has been very little by way of sustainability-linked bonds. I think there have been 10 bonds in Asia Pacific that are sustainability-linked, and that is fairly mainstream in Europe or in the US.

So we would expect this market to grow. We are very thoroughly engaging issuers and borrowers on that topic, and we are quite optimistic on the near-term growth prospect of sustainability linked bonds, overall. The other driver is the expectation of the Asia investor base. I think it is very noticeable that they have sharpened their pencil around everything which is ESG, and we have really felt that trend. As for other geographies, investors that are committed to responsible investment will ask for more transparency of our sustainability commitments from issuers. There remain in our region a lot of issuers that haven’t really published concrete sustainability targets or, where relevant, decarbonisation roadmaps that are ambitious enough. They are being held accountable more so today than in the past by investors.

There is a lot of focus that is no longer being top-down or issuer-driven, but also investor-driven. That is a positive dynamic of the investor having high expectations. As Zhi Wei mentioned, larger delegated investable funds are ready to be invested, but the criteria for investment, or the bar, has gone higher as time has passed.

In a nutshell, the focus now is on sustainability-linked bonds and with all the publication of official taxonomies a lot of groundwork has been achieved. So we are very optimistic here that this market is really going to go from strength to strength in 2022.

To see the digital version of this roundtable, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@lseg.com