JP Morgan and Goldman Sachs have reaped significant profits trading Russian debt and derivatives this year amid a dramatic reshuffling in investor exposure to the country following Moscow’s invasion of Ukraine in February.

Emerging market specialist Akash Garg at JP Morgan has been one of the standout traders during this tumultuous period, helping the US bank generate around US$100m in revenues from Russia-related debt exposures, according to sources familiar with the matter. Goldman Sachs has also made about US$100m with Steven Gooden one of the traders to perform strongly, sources said. Elsewhere, Barclays has made at least US$50m in revenues with head of CEEMEA corporates Oleg Sarzhin among those to do well, sources said.

Trading Russian sovereign and corporate debt has not been for the fainthearted this year following the start of the war in Ukraine. Prices have whipsawed on concerns over defaults spreading across the Russian economy as Western sanctions bite. International lenders have also had to tread carefully to avoid breaching the complex set of new rules limiting contact with many companies and individuals.

Still, those sanctions have stopped short of prohibiting trading in Russian credit derivatives or bonds in secondary markets, allowing banks to cater to the surge in demand from Western asset managers to dump positions, often at fire sale prices. That volatile backdrop has created a fruitful trading environment for the small group of banks possessing both the expertise and risk appetite to remain active in these markets.

"Some banks have been well positioned for the move and are still actively trading,” said one EM trader. “The reality is there are only a handful of banks in the Street that would have the risk appetite to facilitate client flows in this environment.”

A spokeswoman for Goldman told IFR: "Our trading activity in Russian securities is focused on clients’ risk reduction so they can proceed with an orderly wind down of exposure."

Spokespeople for JP Morgan and Barclays declined to comment.

Price collapse

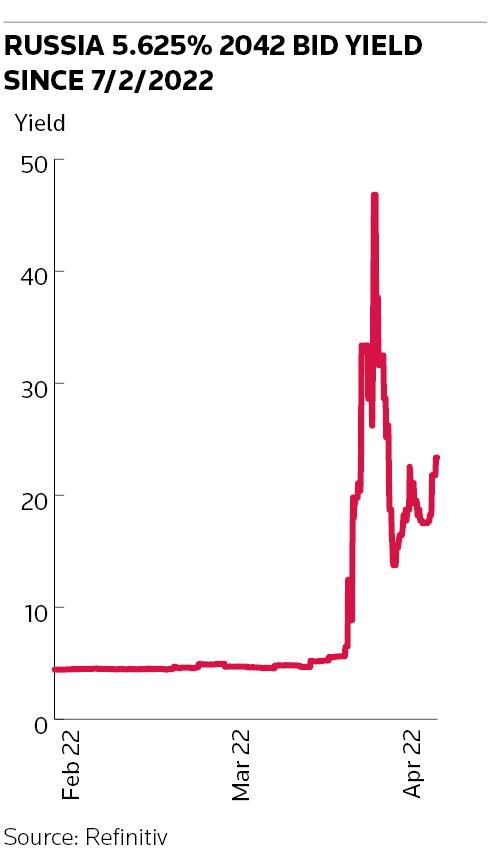

Russian debt prices have collapsed since president Vladimir Putin ordered the invasion of Ukraine in late February, as international fund managers have rushed for the exit. Credit strategists at JP Morgan have estimated that US$9.1bn in market value of Russian debt is at risk of forced selling following the country’s exclusion from global bond indices.

Bond trading activity has risen sharply. Daily volumes in US dollar-denominated Russian sovereign debt have averaged more than US$240m since the Ukraine invasion, according to bond trading platform MarketAxess, more than double last year's average. That has provided more client business for bank desks brokering these transactions.

The ensuing volatility, meanwhile, has made trading far more profitable by allowing banks to widen the bid-offer spread between where they will buy and sell Russian securities. That means traders can take a juicier cut when buying bonds at steep discounts from conventional asset managers before shipping them on to distressed investors.

Refinitiv data show just how wide the bid-offer spread on US dollar Russian sovereign bonds is at the moment. Traders were bidding for the 2030 bond at 23 cents and selling at 27 cents on Friday, according to Refinitiv. That compares with a bid-offer spread equivalent to roughly a tenth of a cent in early February before the conflict began. The 2030 bond was trading above face value – at about 108 cents – in early February before falling as low as 15 cents in early March.

“The price collapse we’ve seen across sovereign and corporates has been unprecedented with reports that clients have sold paper at low single-digit levels, and clearly bid-offer spreads remain considerable,” said the EM trader.

A second trader put it more bluntly: “It’s hard not to make that much money when the bid-offer spread is that wide.”

CDS payoff

But it’s not just buying and selling Russian bonds that has proved profitable. Sources said trading in Russia credit default swaps had also been an important driver of revenues. Russian sovereign CDS prices have swung wildly in recent weeks amid widespread confusion over whether Moscow will default on its external debt.

The upfront cost of insuring against a default on US$10m of Russian debt for five years was US$7.3m on Friday, according to IHS Markit, compared with a recent low of US$4m in mid-March. That came amid concerns that a default is looking increasingly likely after the US Treasury told US banks that funds in accounts held by Russian entities that are subject to sanctions should not be used to make debt payments.

In a separate development, an industry body known as the Credit Derivatives Determinations Committee said it would meet on Friday to discuss further whether a CDS trigger event had occurred on Russian Railways following the state-owned company's failure to make a coupon payment to bondholders within the allotted time.