Companies making slow progress on ESG targets are seeking to refinance sustainability-linked loans early to avoid paying interest rate step-ups – and there are currently no guidelines in place to stop them.

None of the first generation of SLLs have been refinanced to date, but bankers are already hearing from a handful of borrowers about suspiciously early refinancings. On closer inspection, it seems that some companies are trying to refinance their SLLs to reset targets – or key performance indicators – before they fail them, bankers said.

“We have companies that have contacted us earlier than we thought they would and are talking about refinancing,” a head of sustainable finance at one bank said. “There might be some areas like female representation on the board where companies haven't found anyone, which means they’ve failed and it will cost them 2bp but they don’t want that.”

That 2bp would come as a result of the borrower missing the target embedded into its loan and having to pay a higher interest rate as a penalty. But if the loan is refinanced and the target removed or changed in the new loan, the issue goes away – and so does the higher funding cost and potential embarrassment.

Little thought

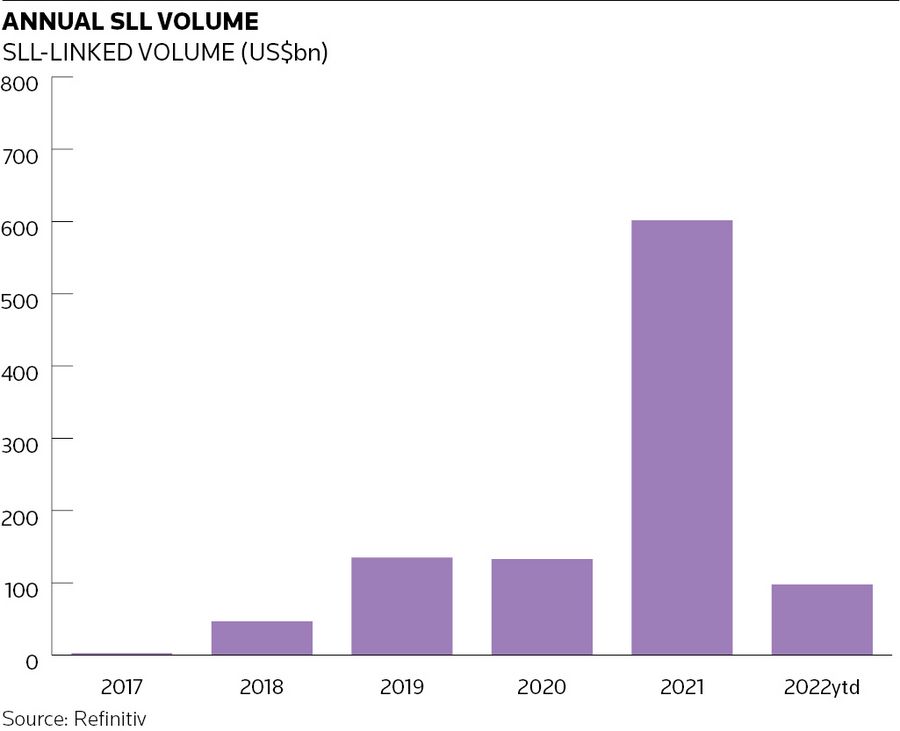

The sustainability-linked format was created in the loan market in 2017 when ING arranged the first SLL – a €1bn deal for technology company Philips – and subsequently moved into the bond market where the first sustainability-linked bonds were issued in 2019.

Volume has exploded. Some US$601.4bn of SLLs were issued in 2021 compared with US$2.56bn in 2017, while SLB issuance soared to US$91bn last year from US$4.3bn in 2019, according to Refinitiv data. But remarkably little thought seems to have been given to refinancing in either format.

Early refinancings are also an issue in the high-yield bond market, which is currently debating “callability”, as some borrowers can pay call premiums to redeem bonds before ESG targets are tested.

The issue could be particularly pressing for fossil fuel-related companies that are already finding it hard to refinance and could incur additional financing costs and reputational problems if they fail to meet ESG debt tests.

Sean Kidney, chief executive of Climate Bonds Initiative, an NGO, said that in the longer term investor pressure will keep borrowers from gaming their sustainability-linked financings. "If a few key investors kick up a storm about it, bad habits will disappear very quickly,” he said.

The bigger issue for him is that targets on such financings are too lax. “I'm more worried that the original claim by the entity is not up to scratch. I would say something like a half to three-quarters of SLBs are too weak."

No guidance yet

The Loan Market Association does not have any guidance on refinancing SLLs, but the trade body is gearing up to address the topic in market roundtables.

“The LMA's guidance is silent on the topic of refinancing and SLLs. I think we are going to have to have some guidance on this by the sounds of it," said Gemma Lawrence-Pardew, senior associate director for legal at the LMA.

"We will try to add this as an agenda point and get a feel for what is going on in the market and what the LMA may be able to do from a guidance perspective."

The subject has serious implications for maintaining the integrity of sustainability-linked products, as companies that avoid a breach with a refinancing could be accused of greenwashing.

Those following the market are also concerned that companies could even seek to put weaker targets in place, as there is currently no consistent way of measuring the ambition of targets or their effectiveness.

"I would like to see refinancing responding to a growing appreciation of necessary ambition – ie, upping the ante, not lowering the ante," Kidney said.

Maintaining standards

Maintaining the quality of SLLs and SLBs is also important for banks and is the subject of vigorous internal debate as any deterioration could impact banks’ own decarbonisation trajectories and sustainability ambitions.

Lenders are putting infrastructure and internal processes in place to track sustainability-linked instruments post issuance as such evaluations are increasingly becoming key business metrics that feed into banks’ own targets, such as the volume of sustainable finance that they are providing.

Some bankers are considering new SLL structures that include ambitious and stretching targets that offer savings of 4bp–5bp as well as more modest targets with savings of around 2bp if the stretching targets are not met.

“We may see more of those nuances appear in the next generation of SLLs," said Arthur Krebbers, head of corporate climate and ESG capital markets at NatWest Markets.

But for the sustainability-linked format to operate more efficiently, borrowers may have to overcome their fear of failure.

“I think it's healthy for the sustainability-linked asset class when there are cases when targets are not met, as we can assess how the instrument's price responds. It would certainly create tangible data points,” Krebbers said.