The recent surge in commodity prices has presented companies active in these markets with what should be the most profitable trading environment in years. There’s just one crucial hurdle for them to clear first: weathering the largest and most sustained liquidity crunch most will have ever faced.

Commodity prices have soared since Russia invaded Ukraine in February, broadening out from a jump in energy prices that began last year to include a steep rise in the price of metals, agricultural products and many other commodities. While that is good news for miners and trading houses sitting on physical assets, it has also triggered an unprecedented cash crunch in the form of billions of dollars of margin calls for those same companies because of their use of derivatives to hedge exposure to falling prices.

Financial institutions so far have stepped up to meet much of the industry’s cash shortfall, providing a mixture of conventional loan facilities and more bespoke transactions such as liquidity swaps. But many warn of a prolonged liquidity squeeze over the coming months that will force companies to scythe back exposures and potentially lead to consolidation among some of the more niche commodity traders.

“As prices go up, [trading houses] can’t collect margin on the value of their physical positions increasing, but they have to post margin against the value of their derivatives hedges declining,” said Jonathan Whitehead, an industry veteran who most recently headed commodity markets at Societe Generale. “Trading firms and other producers will have got massive margin calls this year, probably well in excess of what their loan facilities were designed to cover.”

Commodity companies have long been prone to liquidity mismatches during times of market stress. Gains on physical positions like barrels of oil take time to realise (cargoes must first be shipped and sold over the course of weeks or even months), whereas margin calls on underwater derivatives hedges must be met immediately.

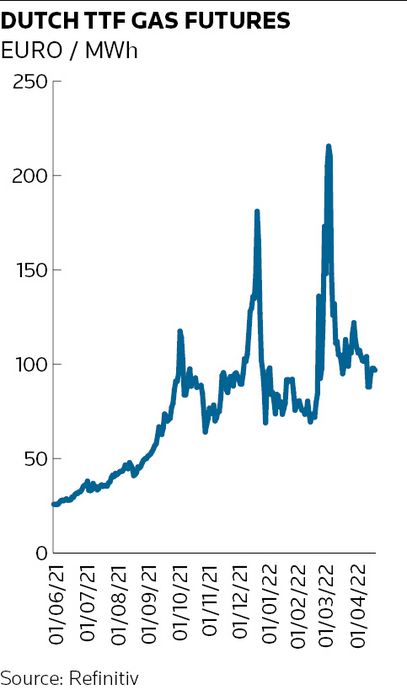

Traders have been ramping up preparations for a once-in-a-generation cash call since last year, when a surge in energy prices provided a foretaste of 2022’s wild price swings. European wholesale gas prices nearly tripled in under two weeks following Russia's invasion of Ukraine, and quants at trading giant Trafigura calculated broader commodity markets were at their most volatile in 60 years by early March.

Bumper profits

For those able to ride out the turbulence, though, the promise of bumper profits awaits. Gunvor reported 2021 net profits of US$726m on Tuesday – more than double its 2020 earnings. That came after the energy trading specialist dismissed what it called "erroneous speculation" about alleged margin call-related stress in its gas trading business in October. Gunvor said in March it had adjusted its trading volumes in liquefied natural gas and it had also secured about US$4.7bn in debt over the past five months to maintain “adequate liquidity”.

And it's not alone. Trafigura has raised significant amounts of money on top of the US$10bn cash buffer it already held going into the Ukraine crisis – a buffer that allows the trading company to pay millions or even billions in margin calls when there is a crisis, according to Christophe Salmon, Trafigura’s chief financial officer.

“Liquidity risk has always been and will always be the biggest risk for a commodity trading house,” Salmon said. “We use derivatives to hedge our physical inventory and by doing so we take liquidity risk when we face margin calls. Commodity prices have increased significantly this year, which means the whole industry has had to pay margin calls on the hedging side.”

Salmon said Trafigura had enjoyed “great support” from its banks which, combined with the physical turnover of its cargoes, has allowed it to “manage through this unprecedented volatility safely". In March, the Singapore-based trader roughly doubled the size of its nine-month multicurrency revolving credit facility to US$2.3bn after 12 banks joined the underwriting group and it also increased the size of its Japanese loan facility to ¥93.8bn (US$790m).

“The crisis has tested our funding model. We started in good shape, but as we don’t know how long the crisis will last, we have raised backup lines of credit to have another layer of safety should commodity prices increase to unprecedented levels,” Salmon added.

Liquidity concerns

Mining and trading firm Glencore said in its latest annual results the margin calls it paid out increased 60% to almost US$6bn over the course of 2021, giving a sense of the scale of the rising cash demands companies would have faced earlier this year when volatility soared further.

In one dramatic example, the London Metal Exchange chose to suspend trading of nickel futures and cancel a raft of transactions after prices more than doubled in the space of a day. That debacle was linked to a short derivatives position from Chinese nickel tycoon Xiang Guangda, who later secured a loan facility from a group of banks led by JP Morgan to help meet margin calls. JP Morgan reported a loss of about US$120m in the first quarter related to counterparty exposure from “clients closely linked to nickel producers”.

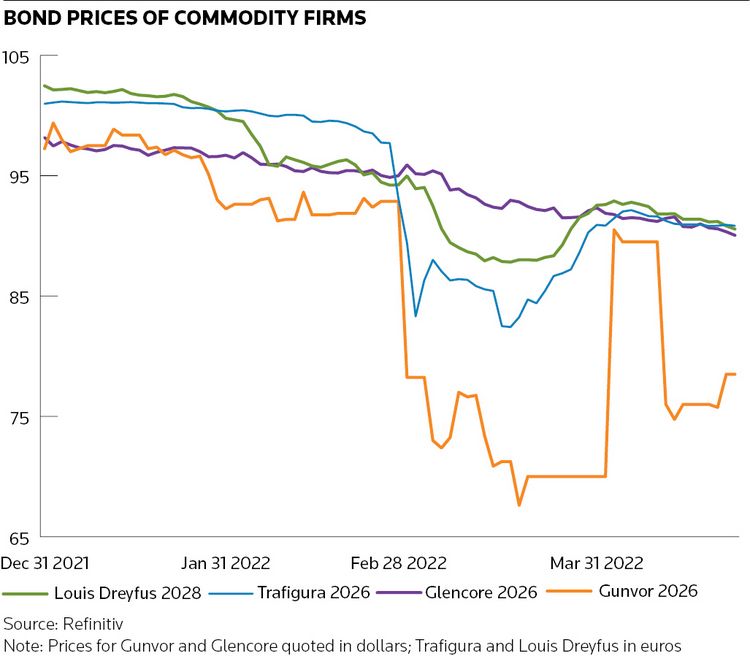

The scale of the market moves – as well as concerns over exposure to Russia in some cases – inevitably put commodity firms under pressure. The bonds of commodity traders slumped in March before recovering somewhat, while the European Federation of Energy Traders even called for emergency public sector support to alleviate the liquidity squeeze.

“The trading firms are aware of liquidity issues and they have sized their credit lines accordingly. But the extreme situation has exhausted those resources, so firms have been scrambling to increase the scale of those lines,” said Craig Pirrong, a professor at the University of Houston who specialises in energy markets. “So far the banking system has stepped up, but who knows how long this is going to last and what future needs might arise – or whether the banking system will be as accommodating as it has been so far?"

Funding round

The largest commodity firms haven’t shown any outward signs of difficulties in accessing bank financing, with the likes of Glencore, Vitol and Mercuria Energy all raising money this year. Some have cast the net even wider, with reports in March of Trafigura discussing an investment from private equity group Blackstone, which ultimately fell through.

“We want to diversify and to widen our funding pool in terms of the number of financiers we use, which includes going beyond the banking space," Salmon said.

Banks have also stepped up with some more innovative financing structures, often secured on physical commodities. Such deals include so-called liquidity swaps, where firms can move derivatives hedges on exchanges to over-the-counter transactions directly facing an investment bank, which allows the client to pledge a wider range of assets as margin.

“The cost for clients of being active in commodity markets has increased tremendously," said Yoven Moorooven, global head of new business ventures for commodities at Citigroup. "We have had to examine new ways in terms of how to assist them to go beyond their usual loan facilities to ensure that we keep the lights on and there is not going to be any shortfall. Liquidity swaps, where we take a commodity as collateral, have been very popular."

"Many of these companies are very healthy in terms of business plans – it’s more about the short-term cash needs to cover hedging positions,” he added.

Only a limited number of banks can contemplate such complex structures given the need to be able to liquidate the underlying collateral if the loan soars. The International Monetary Fund commented in a recent report that fewer banks are active in commodities markets in recent years, while noting that there are some signs the severe market stress “may be starting to weigh on dealer banks’ balance-sheet capacity and appetite for intermediation".

Margin calls

It's hardly surprising then that many commodity firms are reducing exposures in the face of rising costs that few believe are going away any time soon. Derivatives exchanges and clearing houses have raised the amount of initial margin that companies must stump up on futures positions because of the elevated levels of volatility, increasing the amount of capital they must have locked up permanently to keep positions open. The EFET said in March the amount of money needed to maintain a position in gas futures had multiplied six-fold from a year before as a result.

That has led to a decline in the amount of outstanding contracts in several futures markets. The open interest in Brent crude oil futures has declined from over 426,000 contracts at the end of March to about 179,000 contracts, according to Refinitiv.

“It’s costlier to do business now, so firms are going to scale back," said Pirrong at the University of Houston. "That is going to have a bigger impact proportionally on the smaller firms. The niche players will face some challenges."

Whitehead agreed smaller traders will be challenged, but said most of the larger houses should be fine. “This is the ideal time to be in the trading house business. My guess is most of these firms will be reporting very strong earnings by the end of 2022,” he said.