Some European ESG bond funds hold no labelled ESG bonds at all and nearly half of the "darkest green" funds have under 15% of their assets in the instruments, new research shows. While some see this as evidence of fund managers misleading end-investors about these products’ ESG credentials, others contend that the approach is not only justified but proves fund managers are not taking bond labels at face value.

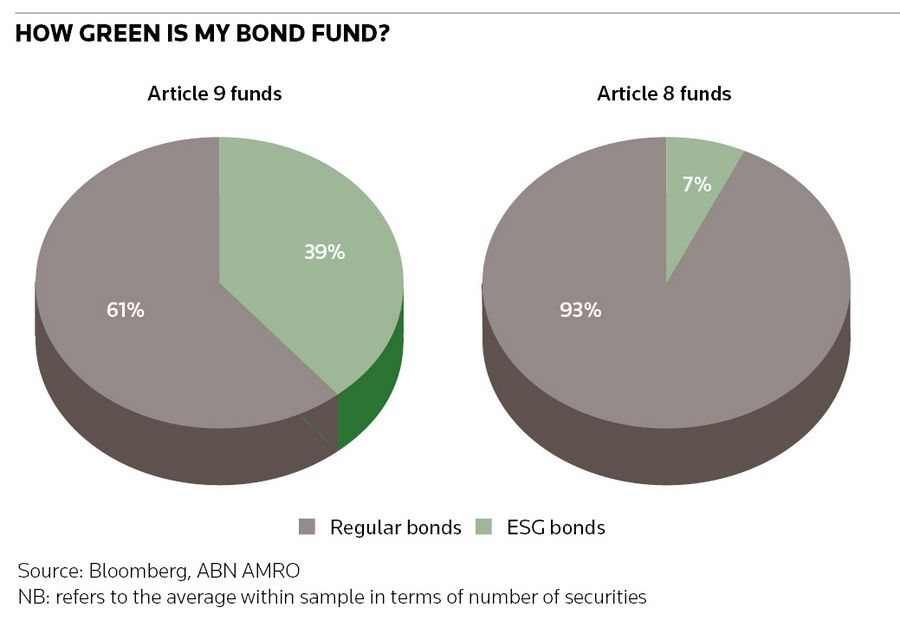

Research from ABN AMRO shows that the almost €1trn of fixed income funds classified as Article 8 investments under the European Union’s Sustainable Finance Disclosure Regulation hold just 7% of their assets in labelled green, social, sustainable and sustainability-linked bonds.

Article 8 funds are a less restricted “light green” category of sustainable investment defined under SFDR as promoting “environmental and social characteristics”.

A handful of Article 8 funds even hold zero labelled bonds, according to Larissa Fritz, ESG and corporates strategist at ABN AMRO. Only 8% of the entire Article 8 fixed income fund universe hold more than 15% of assets in the instruments.

Labelled bonds account for 39% of more rigorous “dark green” Article 9 funds on average, the bank said. These funds are defined as having sustainable investment as their objective.

However, the €50bn Article 9 sector features a notably wide spectrum of approaches. At one extreme, green bond funds managed by firms such as Allianz, Axa, BNP Paribas, Eurizon, Lxyor and NN Investment Partners invest exclusively in labelled bonds. At the other, some Article 9 funds from Degroof Petercam and Robeco have under 5% of assets in the instruments and nearly half (41%) of such funds have holdings of labelled bonds below 15% of overall assets.

Fritz had expected to find that ESG fixed income funds held at least half of assets in labelled bonds and potentially up to 80%.

Liberal approaches

So what's going on? The most obvious explanation is that ESG funds may be overstating their ESG credentials. This would accord with Morningstar’s decision in February to no longer treat 1,200 mostly Article 8 funds across multiple asset classes as sustainable investments after scrutinising their legal documents.

“It seems to me that there have been different approaches out there and they've been a little bit more liberal than certainly the approach that [we] have taken,” said Simon Bond, director of responsible investment portfolio management at Columbia Threadneedle Investments.

Bond manages the Threadneedle (Lux) European Social Bond fund, an Article 8 fund that holds just over three-quarters of its €395m in assets in labelled bonds.

“You can find some pretty strong evidence through surveys that people have taken fairly sweeping assumptions that they're going to be compliant with Article 8 and 9 and they're going to retrofit the data. And they don't actually come up to the mark sometimes,” he added.

Funds may also be seeking to work around the tendency of labelled bonds to trade at a greenium due to buoyant demand and still limited supply. If they do not apply an impact measure such as Columbia Threadneedle’s social intensity score, some may not be able to justify receiving a lower yield from labelled bonds, said Bond.

Self-evident

A more charitable explanation is that some ESG funds are holding unlabelled bonds of issuers in sectors so self-evidently sustainable that the use-of-proceeds structure is unnecessary. Wind farms are one example.

Even so, while acknowledging that the percentage of labelled bonds held is not the only measure of funds’ ESG credentials, Fritz concludes that “it brings a bit into question in the end whether these funds are labelling themselves correctly”.

Accordingly, she judges that end-investors need to “look under the hood” of ESG bond funds more.

Not at face value

A further rationalisation has it that some funds’ low ownership of labelled bonds may actually be a positive – an indication that fund managers are not buying up the instruments indiscriminately.

“To me, it's encouraging to see that the managers aren't just taking labels at face value,” said Julius Huttunen, responsible investment manager at Aegon Asset Management. “Taking them as-is is not a robust process.”

Aegon’s sustainable fixed income funds’ ownership of labelled bonds is “normally” in the high teens, according to Huttunen, though this could rise as their low share of fixed income benchmarks grows with increasing issuance. He imposes “a pretty high bar” on the instruments as he sees both “a lot of opportunistic behaviour” by issuers seeking lower funding costs and a risk of deficiencies in impact reporting.

Since the firm’s ESG focus is on identifying sustainability leaders whose performance will improve with time, Aegon may well favour their cheaper conventional bonds over labelled alternatives. Managers may then seek to combine those with green bonds from less sustainable names to achieve portfolio diversification, Huttunen said.