A US Treasury ban on US firms buying outstanding Russian government debt looks set to complicate the auction process used to determine payouts on credit default swaps referencing the sovereign, sowing fresh confusion over the fate of these contracts.

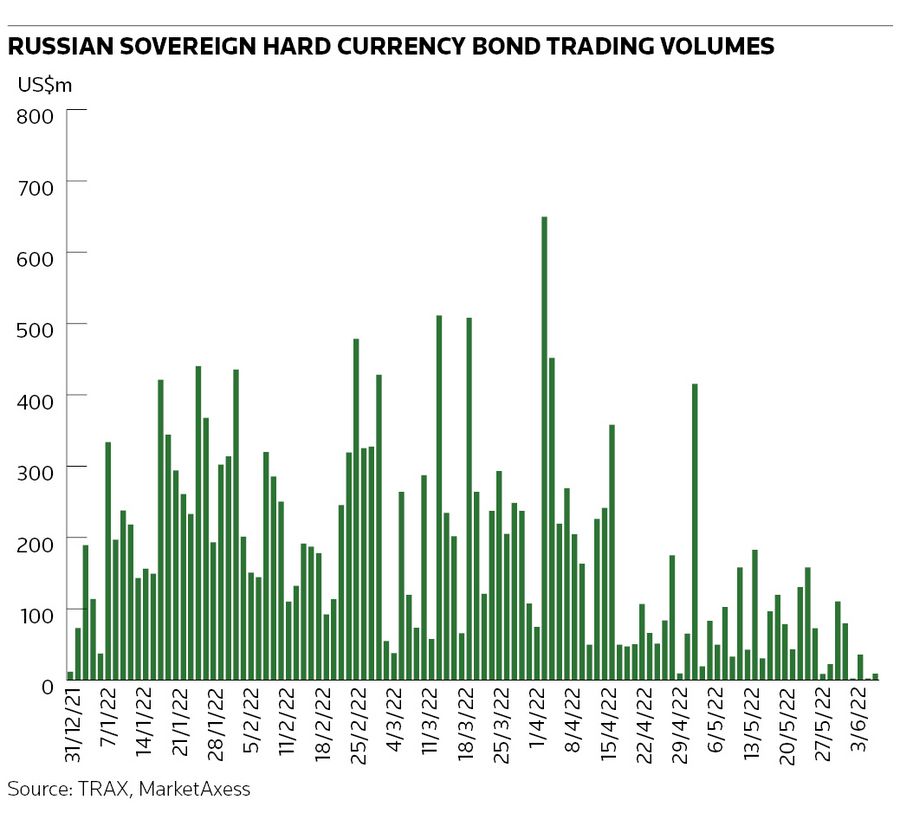

Trading volumes in Russian sovereign bonds have slumped following updated guidance from the Treasury’s Office of Foreign Assets Control published on Monday stating that US firms cannot buy Russian bonds or equities in secondary markets, though they can still sell these securities. That poses a problem for CDS contracts, which rely on trading in secondary bond markets to determine payouts to protection holders.

The Credit Derivatives Determinations Committee, an industry body consisting of banks and investment managers, ruled earlier in June that Russian CDS had triggered after Moscow failed to make US$1.9m of interest payments that had accrued during the 30-day grace period on its 4.5% April 2022s, after settling the bond's outstanding principal and coupon payments nearly a month after their maturity date.

Experts say derivatives users may have to agree on other methods to settle Russian CDS contracts if US restrictions on buying Russian bonds risk distorting a CDS auction.

“It throws into question how a CDS auction would work,” said one US investor, who said his firm was having multiple calls a day with lawyers to discuss trading of Russian bonds and the settlement of the CDS auction. “There’s lots of confusion and uncertainty – more questions than answers. As it stands, we’re frozen from trading Russian assets.”

The credit derivatives market has had to contend with a number of controversies over the years, but it has never had to grapple with such a wide-ranging (and fast-changing) set of international sanctions as those leveled against Russia since Moscow's invasion of Ukraine. That has prompted a series of questions to the Determinations Committee in recent months, culminating in a 12-1 vote in favour of a failure to pay credit event on Russian CDS on June 1.

The Committee must now decide how the roughly US$2.4bn of Russian CDS outstanding should be settled. Ordinarily, that would be through an auction – a complex mechanism that uses market forces to determine payouts to protection holders. Among other things, it allows investors and traders to buy and sell Russian bonds to help establish the value of those securities. CDS payouts can then be calculated to ensure protection holders are adequately compensated for losses that they face on bond positions.

The Committee met on Friday to continue discussions around the settlement of CDS trades after having decided on Wednesday to defer a decision over holding a CDS auction. That deferment was "to allow credit derivatives market participants time to assess the implications" that the Treasury's latest guidelines on trading Russian debt may have on their ability to participate in an auction, according to a statement. The Committee agreed on Friday to meet again in due course.

"It’s problematic for the auction process,” said Athanassios Diplas, a CDS market veteran who helped to design the auction. He added it was hard to comment further at this stage given the lack of details.

Trading pains

The Russia CDS market has more than halved from an estimated US$6bn in early March, according to JP Morgan strategists, suggesting many participants have closed out positions in recent months. Russia CDS have also dropped out of the CDX.EM index, which had accounted for about US$1.5bn of exposure. But while small compared to the roughly US$40bn in Russian external debt, traders and investors will still keep a close eye on the results of this whole episode and draw lessons for credit derivatives markets more broadly.

Sanctions prohibiting trading in Russian debt have long been flagged as a potential issue, prompting a dislocation between derivatives and bond markets shortly after Russia’s invasion of Ukraine. That gap between the two markets subsequently narrowed as banks were allowed to continue trading Russian bonds – with some reaping significant profits in the process.

The updated sanctions guidelines from the US Treasury only apply to US firms, but that has been enough to bring volumes in Russian hard-currency sovereign bonds to a virtual standstill, according to data collected by bond-trading platform MarketAxess's post-trade unit. Many participants are concerned that a ban on US firms buying Russian bonds could create an imbalance between buyers and sellers in a CDS auction.

“The CDS auction mechanism in its normal functioning needs a secondary market for bonds to allow price discovery and transfer of bonds,” strategists at JP Morgan wrote in a March 2 note. “In situations where secondary market trading of bonds would be prohibited by sanctions, the auction process would not be able to occur in its standard form.”

The strategists said CDS markets have a “waterfall of settlement fallback mechanisms” if an auction cannot be held. That includes bilateral cash settlement of CDS contracts.

"While possible, this will require a lot of administration to settle each trade bilaterally, and also economically can end up with different recovery rates on different trades. A mechanism that uses cash settlement through the auction mechanism is likely to look more preferable and would allow all CDS to settle at the same recovery rate and efficiently,” the strategists said.

As for the ruling by the Committee, the only member of the panel to vote against a CDS trigger was Citigroup. The US bank declined to comment. Industry sources noted members of the voting committee are not privy to their firm’s overall position in a particular credit.

Citigroup had previously voted that Russia had incurred a potential failure to pay on the same April 2022s, and its April 2042s, when a separate question had been put before the Committee in April after Moscow had threatened to make payments on those two US dollar notes in roubles. Any further action was subsequently averted after the sovereign eventually paid in dollars.

Adds details of DC meeting on Friday