The US Securities and Exchange Commission will have a fight on its hands if it pushes through controversial rules intended to rein in the special purpose acquisition companies IPO market, according to several groups that have publicly criticised the proposal.

The public comment period closed on Monday.

The proposal seeks to offer myriad new protections for SPAC investors, partly by significantly expanding the liability for banks involved in the IPOs and business combinations that follow.

The rules as proposed are unlikely to survive judicial review, according to law firms and banking advocacy groups.

The SEC's proposal includes a new rule, Securities Act Rule 140a, that would vastly expand the responsibility of banks advising on de-SPAC transactions (that is, the merger of a SPAC with another company) compared with those leading traditional IPOs.

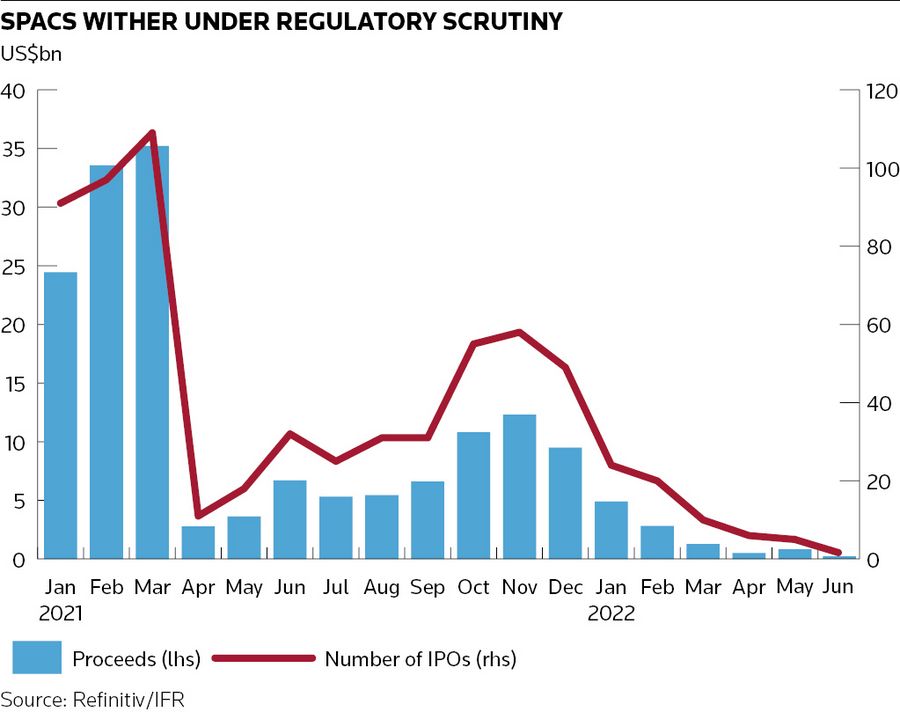

Banks have backed away from SPAC underwriting since the proposal was published at the end of March, with EF Hutton the only US-based firm to lead a SPAC IPO this month, but they may have reason to be optimistic.

The rule exceeds the SEC’s statutory authority and is therefore unlawful and should be abandoned, said the Securities Industry and Financial Markets Association.

“Proposed Rule 140a founders on its defects as a matter of law because it stretches the statutory definition of 'underwriter' beyond its limits, ignoring the statutory text, legislative history and judicial interpretations of its meaning,” Sifma wrote in its response.

Sifma argued that to extend underwriter liability from the SPAC IPO to the de-SPAC transaction the SEC attempts to erase the distinction between the two entirely separate distributions of securities, in violation of section five of the Securities Act, which requires distinct registrations for each transaction. The new rule also violates section six of the act, which provides that a registration statement is effective “only as to the securities specified therein as proposed to be offered”, Sifma said.

For a SPAC IPO and de-SPAC to be one transaction, as suggested by the SEC, the IPO registration statement would have to describe the securities to be issued in the de-SPAC transaction – which is often impossible.

Sifma argues the proposed rule also runs foul of multiple other provisions of the Securities Act, saying it conflicts with longstanding policies and practices of the SEC and violates the Administrative Procedure Act intended to guard against unreasonable interpretation of the unambiguous text of law.

Everyone’s an underwriter

In the proposal, the SEC said underwriters play a critical role in the securities offering process as gatekeepers to the public markets. "By affirming the underwriter status of SPAC IPO underwriters in connection with de-SPAC transactions, the proposed rule should better motivate SPAC underwriters to exercise the care necessary to ensure the accuracy of the disclosure in these transactions,” it said.

But the SEC policy goals cannot override the plain meaning of the statutory language enacted by Congress in the Securities Act to create new gatekeeper responsibilities, opponents of the proposals said.

“The Commission has no authority to deem persons to be gatekeepers and therefore 'underwriters' without reference to the statutory definition created by Congress,” Sifma said.

New York law firm Ropes & Gray said the rules, if adopted, would potentially lead to unintended consequences not only for transactions involving SPACs, but in other merger transactions involving public operating companies.

“The proposed rules go well beyond placing de-SPAC transactions on a more equal footing with traditional IPOs and overlook the fundamental differences between a traditional IPO and a de-SPAC transaction,” the law firm said.

Too imprecise

The American Securities Association urged the SEC not to adopt Rule 140a “as it would disincentivise investment banks from advising on de-SPAC transactions”.

A number of SPAC mergers have been called off in recent weeks, including on Thursday the US$1.7bn merger of VFX company DNEG with Sports Ventures Acquisition Corp.

In a traditional IPO, investment banks understand the amount of potential liability they are assuming for a transaction (and can factor in that liability when deciding what fee to charge), the necessary disclosures and even whether to work for the company.

If the SEC adopts the new rules it would be unclear if each investment bank involved in a de-SPAC transaction could potentially have liability on the entire amount of the securities being distributed in the deal.

That risk would make it untenable for investment banks to continue advising on de-SPAC transactions and, as a result, the regulation could have the effect of shutting down the market. There are currently 590 US-listed SPACs searching for a target, according to SPAC Insider.

The CFA Institute said declaring advisory parties to the de-SPAC transaction to be subject to liability clauses of the Securities Act “is a bold approach” but rule 140a is too imprecise.

Several respondents said the SEC, if it does adopt the rules as written, should clearly state they are not retroactive.