To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com

While equity capital markets bankers around the world spent much of 2022 twiddling their thumbs, those in the Middle East were busier than they’ve ever been. IPO volumes across EMEA dropped to just US$39.1bn in 2022 from US$112bn in 2021, according to Refinitiv data, while Middle East IPO volumes increased to US$23.1bn from US$13.4m. Put another way, the Middle East accounted for 59% of IPOs by volume in the EMEA region in 2022 against only 12% in 2021, while the number of IPOs in the Middle East surged to 56 from 41. As a result, Middle...

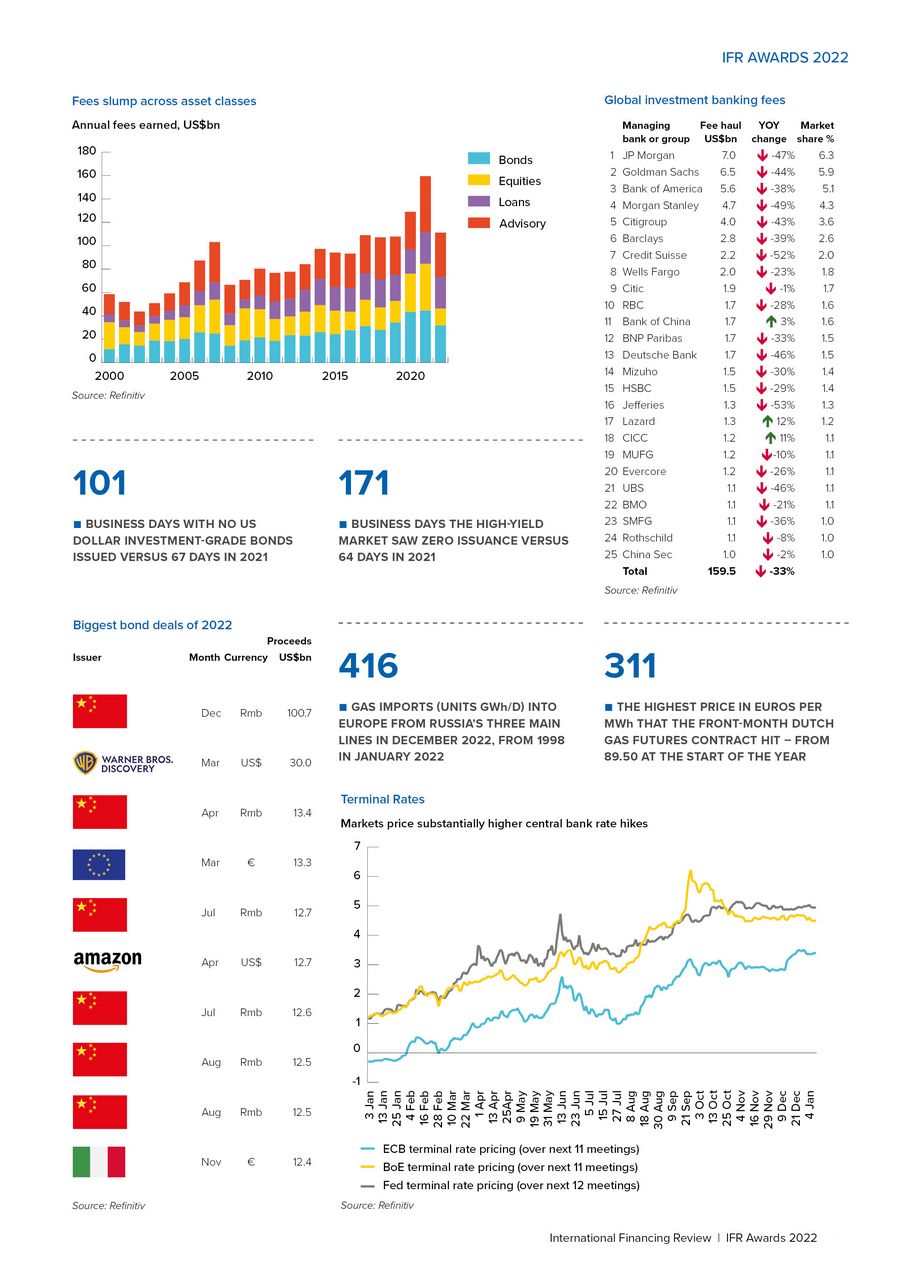

Not many people would have had a liquidity crisis in pension funds threatening UK financial stability on their 2022 bingo cards. But that is what happened in the immediate aftermath of the UK’s then Chancellor of the Exchequer Kwasi Kwarteng delivering his “Growth Plan” to the House of Commons, promising the biggest package of tax cuts in 50 years. The pound dropped to its weakest point against the US dollar since the early 1970s, and 30-year Gilt yields, which had risen by 283bp over the previous three years, soared by 120bp in just three days...

Calm seems to have returned to the market for UK government bonds after the turbulence induced by the short but catastrophic administration of Liz Truss that meant the UK was hours away from a meltdown in some of its major non-bank financial institutions. Indeed, Gilts are enjoying an unexpected purple patch after autumn's unprecedented volatility. But the return of an orderly market could well prove fleeting as huge supply looks set to increase risk again in 2023, meaning there could still be more trouble ahead as the market attempts to absorb...

Financiers led by HSBC chief executive Noel Quinn put on a united front in November when Hong Kong hosted the Global Financial Leaders Summit. Timed to coincide with the resumption of the Hong Kong Sevens rugby tournament after a two-year coronavirus-induced hiatus, the conference was designed to herald a return to business as usual. "We have to help Hong Kong through this next phase of post-pandemic restrictions and continued economic growth to strengthen the confidence of Hong Kong as an international financial centre,” Quinn told the...

Japan made waves in the green finance world with its announcement in May that it would issue ¥20trn (US$157bn) of bond instruments to finance its transition efforts. There was just a little hiccup with the yet-to-be-ratified grand plan: the financing instrument of choice is transition bonds. This is a vaguely defined category of fixed-income instruments to help companies move to renewable energy sources. This softly-softly approach is perhaps not surprising, given that coal and natural gas still fuel 68% of electricity generation in Japan,...