Cellular proliferation

To say the euro market is part of BNP Paribas’ DNA would be something of an understatement. In 2022 it cast its net wider than ever in the public sector arena without missing a beat in its home currency. BNP Paribas is IFR’s Euro Bond House and SSAR Bond House of the Year.

“Every year we reset to zero,” said Frederic Zorzi, global head of primary markets, explaining how BNP Paribas managed to notch up yet another stellar year. But 2022 proved different in that the bank achieved success beyond the single currency, becoming a particularly trusted partner in a critical SSAR sector and enduring a year that Zorzi called “the most challenging since 2008”.

When to execute was “the biggest talking point we have had with issuers”, said Jamie Stirling, global head of SSA DCM. “We have been here before; we have the experience … When we have had tough trades to execute, we have waited [for the right window].”

In euros, the French agencies faced a unique problem: presidential elections limited their execution windows, and the tightening of OATs made them look expensive versus mid-swaps – the metric buyers use to assess value. Between April and May, BNPP went to every French agency to emphasise the importance of getting access to liquidity over the ability to squeeze price.

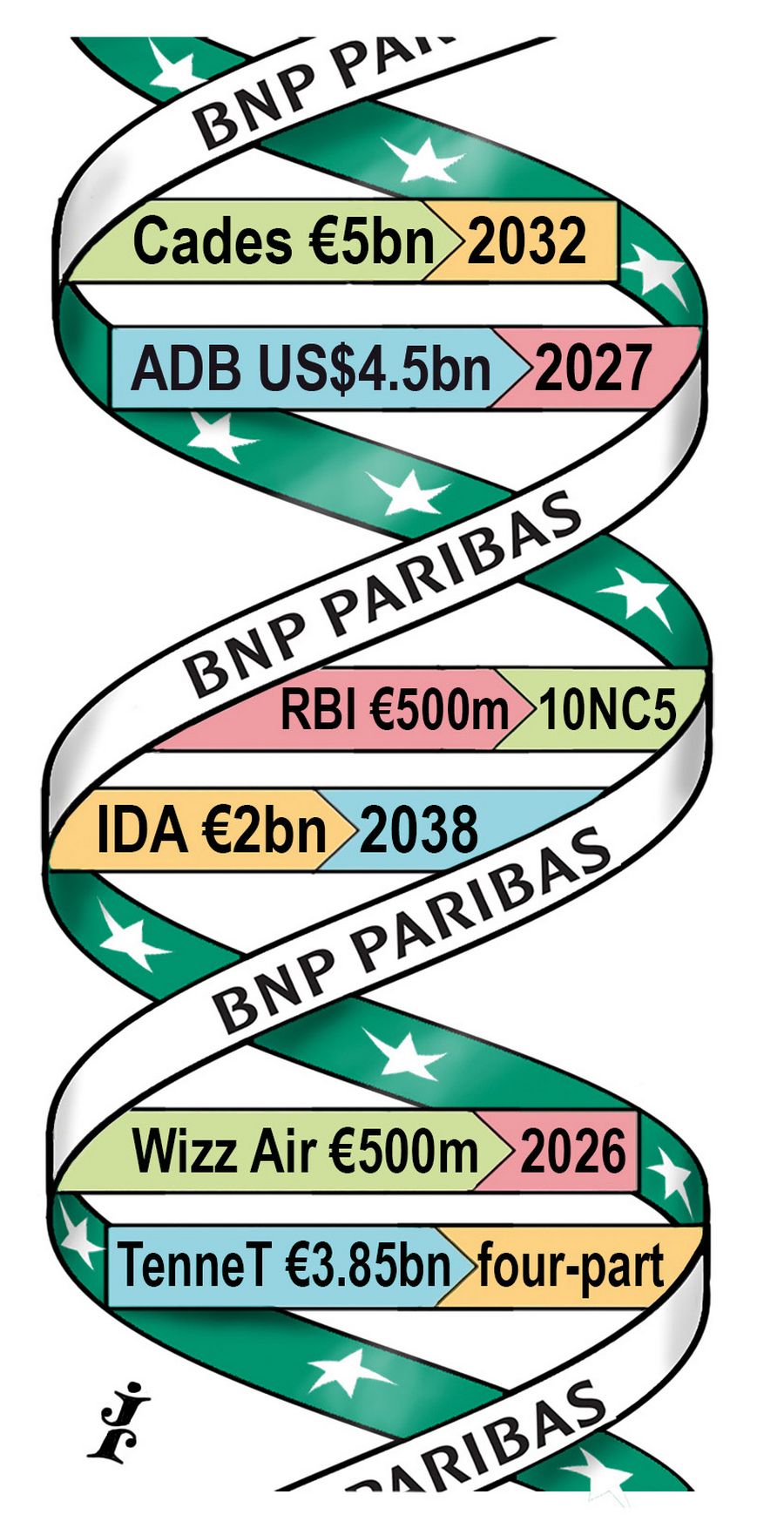

Among the subsequent deals BNPP helped ferry over the line was the €5bn 10-year social bond for Caisse d’Amortissement de la Dette Sociale in April, only two days after the results of the presidential elections were announced.

The bank’s services for the segment extended past the euro space, however.

For the Asian Development Bank in July, hitting the right market at the right time meant switching from what had been envisioned as a euro deal to US dollars. Finding a space in that market for a name that is not a mainstay is an achievement, given the number of pulled deals in 2022. And BNPP also managed to uncover demand in size, building a US$9.6bn book for ADB’s US$4.5bn five-year that helped reopen the market after summer.

Perhaps more unusual was BNPP's claim to fame in the sterling market – a place on the UK Debt Management Office’s now infamous 2053 green Gilt tap in September.

But as Mark Lynagh, co-head of EMEA debt capital markets, said: “It wasn’t tricky in just one asset class, it was every asset class.”

With volatile energy markets at the centre of events, the bank applied its expertise across the utility sector with deals for the likes of TenneT, Suez, Vattenfall, RWE and Thames Water, extending its reach across the Atlantic with a reverse Yankee for Duke Energy.

Headline-grabbing trades were also part of the mix, such as L’Oreal’s multi-faceted debut.

“It was an intellectually challenging time – more complicated than Covid; Covid was one-directional in many ways,” said Lynagh.

This made the environment no easier when delving into the capital stack, and BNPP was again at the forefront of the hybrid market with tailor-made solutions – from Heimstaden’s equity-funded buyback, through various sector reopenings from SSE, Telia and Telefonica, to TotalEnergies’ long-call record-setter. Along the way, it introduced the rarity of a new issuer in the sector in the shape of Terna.

BNPP took this capital expertise into the FIG arena. In what was by no means a banner year for the product as rates rose and spreads available elsewhere chipped away at the product’s allure, non-call considerations also played their part.

Even so, the bank worked on some notable deals, buoyed by the belief that experience – and the timing and market read that came from that – placed it in an enviable position, able to suggest solutions that others might not. “Issuers maybe thought there wasn’t very much of an art involved,” said Damian Saunders, FIG syndicate manager.

A Tier 2 from Swedbank when much of the market thought it was still on summer holiday spoke to that market read, as did Rabobank’s first euro T2 since 2013 and Svenska Handelsbanken’s first since 2018. RBI was also brought to market despite concerns around its exposure to Russia, while Hannover Re, AXA and ASR added insurance supply.

Rabo was notable again in Additional Tier 1, with a highly oversubscribed deal, and SEB saw a back-end valuation discussion result in a lower coupon.

Meanwhile, BNPP was across the senior (preferred and non-preferred) sectors in a top-ranking position, while featuring highly in covered bond echelons despite a relative lack of reciprocity.

The one thing all asset classes had in common, however, was volatility. “You can solve an equation when you have one unknown but three or four is more challenging,” said Zorzi.

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com