Quick to adapt

CICC spotted windows of opportunity to connect Chinese companies with investors onshore and offshore in the most volatile conditions seen for years. For overcoming geopolitical challenges and being prompt to find new avenues to raise capital, CICC is IFR Asia’s Asian Bank of the Year.

Unpredictable lockdowns and knock-on effects from US-China tensions made the Chinese market a tricky place to navigate, but also offered rich pickings for those who were quick to adapt – and chief among them was CICC.

In a year when Asian offshore debt issuance stalled and global stock offerings dried up, CICC was in the perfect position to take advantage of a Chinese onshore market boom, as well as finding the best opportunities to raise funds offshore.

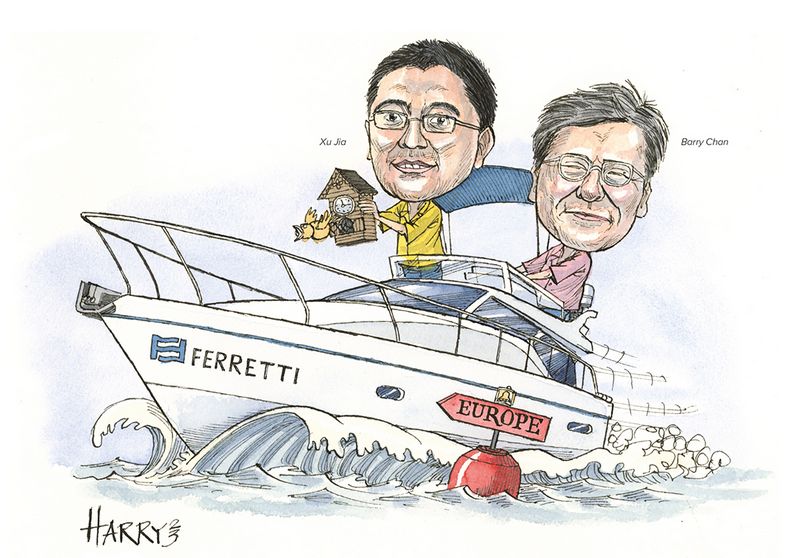

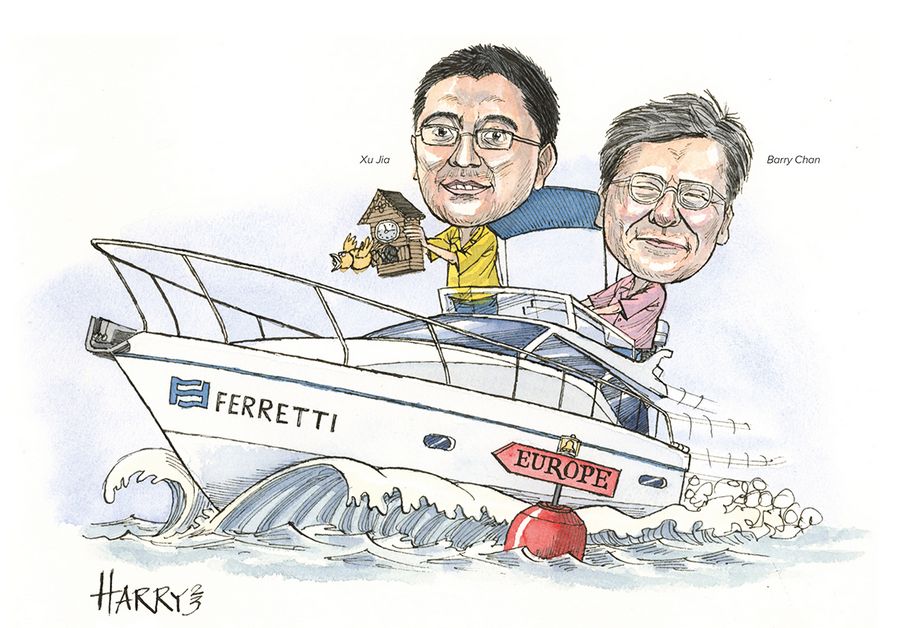

“At CICC, we are quite balanced between the domestic market and the international market,” said Xu Jia, deputy head of investment banking. “We can help our clients raise capital at home and in international markets.”

Not only did it grow its market share in China’s ECM market to 11.6% from 9.5% the year before, but it spotted opportunities to bring Chinese issuers to offshore markets – most notably through global depositary receipts listed in Europe.

CICC was sole bookrunner as building material machinery manufacturer Keda Industrial Group raised US$173m in the first wave of Chinese GDR offerings in Switzerland. The deal, and the swiftness with which it was executed, demonstrated that CICC had its finger on the pulse when it came to reading the regulatory environment.

“CICC has strong insight and keen observation about the business trends and policy directions in China,” said Barry Chan, CICC’s head of Hong Kong investment banking. “This has enabled us to put ourselves in the best position to anticipate and seize the business opportunities.”

In 2022 it was challenging, not to mention risky, for Chinese companies to attempt US listings. Several companies like CNOOC and China Mobile had been blacklisted because the US claimed they had links to the Chinese military, preventing US investors from buying their securities. Other US-listed Chinese companies were told they would need to delist if an agreement could not be reached on US inspections of Chinese audits, under the Holding Foreign Companies Accountable Act (the two countries eventually reached a deal in mid-December).

CICC spotted an outlet for Chinese companies, though, and helped bring an upsized US$707m GDR offering from Ming Yang Smart Energy Group to London in July – the first Chinese GDR offering there for 20 months – before broadening its horizons even further.

“The benefits of GDRs are that they broaden the financing channel for A-share listed companies from overseas and provide opportunities for foreign investors to participate and become shareholders of A-share listed companies without requiring any QFII [qualified foreign institutional investor] qualifications,” said Shi Qi, CICC’s head of ECM.

China in late 2021 added more European countries to the Shanghai-London Stock Connect trading link. Some Chinese companies had already sold GDRs in London, but politically neutral Switzerland turned out to be a receptive market too.

Keda’s market-opening Swiss GDR offering came with a US$44m cornerstone investment from Guangdong (Foshan) Manufacturing Transformation and Development Fund to ensure its success. The deal priced at a discount of just 9.3% to the equivalent A-share quote, much tighter than Chinese companies could achieve in the Hong Kong market, and with quicker execution than in the domestic market.

A wave of Chinese companies followed, and CICC helped bring Swiss GDR offerings for Lepu Medical Technology (Beijing) and Gotion High-Tech. CICC had already helped introduced Volkswagen as a strategic investor in lithium-ion battery manufacturer Gotion.

“We believe there will be more and more GDRs,” said Xu. “This can be an important product for A-share-listed companies. This can help companies raise foreign capital and valuations are pretty decent.”

The primary market in mainland China led the world for IPOs in 2022, and CICC was well positioned to lead the wave of listings.

Its standout deals included Shanghai United Imaging Healthcare’s Rmb11bn IPO on the Star market.

Usually, Star IPOs allocate only 30% to strategic investors, but CICC managed to win approval to increase it to 50%, through solutions like combining multiple mutual funds under the National Social Security Fund’s account, freeing up more space for other strategic investors. The institutional order book was more than 1,000 times subscribed.

The Hong Kong market found it harder to attract international listings, but CICC was sponsor and joint bookrunner for the only major Hong Kong IPO by a foreign company this year. Luxury yacht maker Ferretti, which is based in Italy but majority-owned by a Chinese company, completed a HK$1.9bn IPO in late March, despite the shock to emerging markets from Russia’s invasion of Ukraine on February 24.

After Hong Kong saw a series of disappointing listings, China Tourism Group Duty Free’s HK$18.4bn offering, the year’s largest new listing, traded well enough for stabilisation agent CICC to exercise most of the greenshoe.

“Even against this background of a tough market, CICC remains the top bank in the Hong Kong IPO market,” said Chan. The bank had a team of 26 Hong Kong IPO principals as of December 2022, showing its commitment to the market.

It also took a different approach to some foreign banks, many of which either advised clients to wait for better market conditions or walked away from deals when sizes shrank.

“In a challenging market like the one we see this year, instead of simply telling our clients to ‘wait or withdraw’, we formulate alternative plans that would be in the best interest of our clients, including, eg, sticking to the original listing timetable with a smaller size of funds raised so that the clients will enjoy the listing platforms earlier,” said Xu. “This helps establish and continue our long-term partnership with our clients.”

CICC acted as sponsor on Hong Kong listings from Tianqi Lithium and electric vehicle manufacturer Zhejiang Leapmotor Technology, the city’s second and third-largest floats of the year. These deals showed how it has built ties to the supply chain for EVs and batteries, which was a hot sector with investors in 2022, as well as tying in with CICC’s ESG ambitions.

And when US regulators showed signs of warming to Chinese companies in November, the bank brought a US$52.3m Nasdaq IPO from Atour Lifestyle, the first sizable China-to-US listing in more than a year.

In the domestic market, CICC led a range of innovative deals with ESG angles. The Mirattery 2022-1 Green Battery ABN raised Rmb400m in the first ABS transaction to use NEV batteries as the underlying assets. The deal was Mirattery’s capital markets debut, and was subscribed 2.92x.

CICC arranged one of the first subsidised rental housing REITs: the Rmb1.3bn CICC-Xiamen Affordable Housing Group Subsidized Rental Housing Closed-end Infrastructure Fund, which was subscribed more than 100 times.

It was also lead underwriter on the first rural revitalisation bond to have a carbon-neutrality label, CECEP Solar Energy’s Rmb1bn Green Rural Revitalization corporate bond.

“We are actively promoting standards of domestic green bonds to be in line with international standards to facilitate the flow of green finance between China and the EU,” said Zhang Xing, executive head of fixed income.

Much of the offshore activity from China was by local government financing vehicles as many other issuers stayed onshore, but while CICC was happy to join those straightforward LGFV deals, it also introduced more complex trades.

It led a US$700m five-year offering for China Tourism Group that priced 40bp inside initial guidance and came flat to its curve – even though the deal came on February 22, when investors were already concerned about developments on the Ukraine border, and Chinese tourism was practically non-existent.

As Dim Sum volumes surged, CICC worked on the Chinese sovereign’s Rmb3bn dual-tranche offering in Macau, as well as ESG-themed trades for Shenzhen Municipality and Hainan Province. Shenzhen’s Dim Sum had blue, green and conventional tranches, while Hainan’s deal comprised blue and sustainability notes.

All these deals came amid the most challenging conditions seen in years, with offshore rates surging and China’s economy slowing, while Covid-19 restrictions made it hard to even arrange investor meetings. Despite these challenges, CICC was able to reshape its plans against the ever-changing landscape and deliver the best outcomes for its clients.

To see the digital version of this report, please click here

To purchase printed copies or a PDF, please email shahid.hamid@lseg.com