Banks are optimistic FICC has settled into a durable new "normal" level that is significantly higher than in the past.

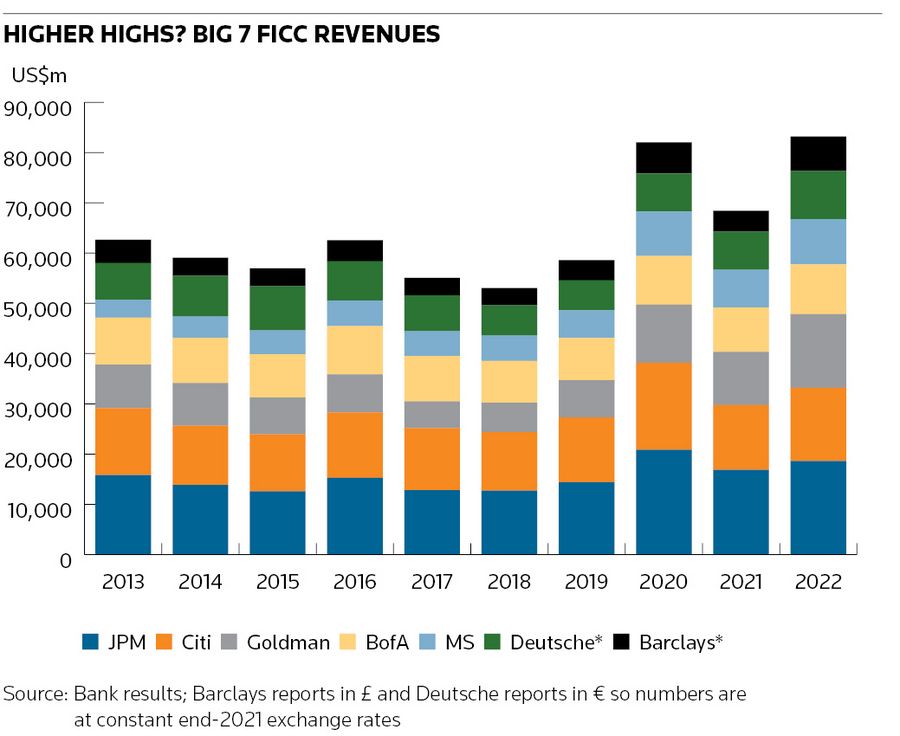

Global banks pulled in FICC revenues of almost US$100bn last year as clients hedged FX, interest rate and energy price exposures in an uncertain world. But gauging what new normal revenues are for fixed income, currency and commodities trading is fraught with difficulty, and banks are wary of getting too bullish given past volatility in the business.

FICC typically accounts for 40%–45% of investment bank revenues and it was a shining light last year with an 18% jump in revenues, making up for a slump in dealmaking fees. But FICC is regarded with suspicion by bank shareholders because of its unpredictable revenues and significant capital requirements. It also encompasses multiple products, geographies and types of client, adding to uncertainty and risks.

That makes bank bosses cautious about predictions, although several recently said they were confident FICC revenues have moved up a gear.

“If you go back and look at the intermediation trading businesses from 2017 to 2019, I can’t tell you what you saw in 2021 and 2022 is going to be the new normal – but whatever it is, it’s more than it was in 2017, 2018 and 2019,” Goldman Sachs CEO David Solomon said at the bank’s investor day on Tuesday. “There’s been structural growth in the market and structural growth in the opportunity set.”

That opportunity has come from more volatile markets. Rates trading has surged as central banks aggressively lifted interest rates; FX trading has swelled due to the new rates cycle, events such as Russia’s invasion of Ukraine, US-China tensions and interest in emerging markets; and higher and more volatile energy and commodities prices have been providing a boon for banks which kept FICC units fully staffed.

Each area has seen increased hedging by corporate and institutional clients, and more activity by hedge funds and speculators. And while the geopolitical backdrop may improve, it appears unlikely there will be a return to the low rates and inflation era of the 2010s any time soon.

“We were completely wrong in budgeting in 2021 and in 2022,” JP Morgan head of global markets Troy Rohrbaugh said at a conference last month. He said JP Morgan had expected revenues to dip back towards the level of 2019.

“And good for the firm and for everyone involved in the business, we were wrong. It normalised at a much higher level,” Rohrbaugh said. “We predicted more normalisation in 2022, and we were wrong again. And last year was the second-best year we've ever had in markets.”

More durable?

Bank bosses could be rewarded by shareholders with higher valuations if they can show FICC revenues are more durable and diversified.

“Historically, people have viewed this business as volatile and therefore harder to predict, harder to project and harder to value,” said Goldman's co-head of global banking and markets, Dan Dees, at the investor day. “We think the reality is more nuanced than that, and we think the reality has changed."

FICC financing is key to that, and adds to intermediation revenues – or core sales and trading. FICC financing is asset-secured lending, and banks including Goldman and Barclays see it as a growth area with attractive returns. It can include repos, structured credit, warehouse and asset-backed lending.

Goldman said FICC financing contributed US$2.8bn last year, double the US$1.4bn in 2019 and up from US$500m in 2013. “In FICC and equities trading there’s now a big, sizeable financing business that still has the potential to grow,” Solomon told analysts.

Barclays estimated markets financing (including FICC and equities financing) revenues were £2.9bn in 2022, up from £2.2bn in 2021 and £1.8bn in the previous two years. “Intermediation income goes up and down with volatility. Whilst financing will also fluctuate to some extent with the leverage needs of our clients, it has a more stable base than intermediation,” Barclays CFO Anna Cross told analysts last month.

Goldman has led the FICC surge and revenues in the business hit US$14.7bn last year, up 38% from 2021 and its highest level since 2009. The bank’s FICC revenue has averaged US$12.3bn in each of the last three years, up 60% from the average of US$7.7bn in the previous nine years.

The FICC pool is big enough to have lifted most banks in the past three years, although the revenue rise has been most marked at Goldman (up 99% vs 2019), Barclays (up 69%), Morgan Stanley (up 63%) and Deutsche Bank (up 61%), according to IFR analysis.

FICC revenues across the top 14 corporate and investment banks last year was US$97bn, up from US$82bn in 2021 and above the US$96bn in 2020, according to data analysis firm Tricumen. Tricumen estimated FICC revenues in the past three years have averaged US$91.7bn across the 14 banks, up 26% from the average of US$72.5bn from 2016 to 2019.

US bank analysts expect the new normal in FICC could be as much as 20% higher than 2019 levels.

“The positive trends we noted in 2021 and 2022 – better tech, higher client flows, etc – still stand,” said Tricumen partner Darko Kapor. “With that in mind and, of course, barring any unexpected geopolitical/similar shocks, I'd expect 2023 at around the same level as 2022, maybe slightly ahead. But I don't expect a drop in overall FICC revenue,” he told IFR.

Kapor echoed the caution of bankers, however, and said predicting FICC was tricky due to macro factors, including the strength of the US dollar as well as geopolitics (in particular the war in Ukraine and the relationship between China and the US).

Tricumen estimated last year's FICC revenue basket included US$38bn from rates and municipals, up 31% from 2021; FX revenues of US$33bn, up 32% on the year and up 83% from 2019; and commodities revenue of US$12bn, up 20% on 2021 and three times the level in 2019. Those rises easily outweighed a 22% drop in credit revenues to US$14bn.

Goldman and the four other US powerhouses – JP Morgan, Citigroup, Bank of America and Morgan Stanley – brought in US$66.8bn in FICC revenues last year, up 18% from 2021. That was behind only their 2020 tally of US$68.3bn and a US$78.3bn bonanza in 2009 when trading revenues surged after the financial crisis.

FICC revenues for the five banks have averaged US$63.9bn in the past three years, or 33% above average annual revenue of US$48.1bn in the previous nine years.

Europeans too

European banks have also ridden the wave. Barclays’ FICC revenues hit £5.7bn last year, up 65% on the year and the best year since it changed reporting lines in 2013. Its FICC revenues have averaged £4.8bn in the past three years, up 50% from the previous seven years.

Deutsche Bank’s revenues from fixed income and currencies were €8.9bn last year, up 26% from 2021 and the highest for a decade and BNP Paribas reported a 33% rise to €5.2bn last year.

All three appear to have won market share. Much may have come at the expense of troubled Credit Suisse, where FICC revenues sagged to SFr2bn (US$2.13bn) last year, down 44% on the year, hurt by the shrinking of its investment bank, particularly in securitised products.

In contrast, Deutsche's rise in trading revenues – from what it refers to as "FIC" since it shut most of its commodities trading business in 2013 – has been timely and helped the debt powerhouse’s recovery.

“I do think we've turned a corner and there is a secular increase in FIC revenues coming or that we're in the middle of or at least started,” Deutsche finance chief James von Moltke told reporters last month. He said that was in contrast to several years ago, when many thought the industry was facing “a secular downward drift” in FIC revenues.

That has changed, although he told analysts not to expect last year’s FIC revenue of €8.9bn to necessarily be the new run rate. “But I think we would take the view that the baseline has simply moved up based on both the environment and the way we [are] … executing on the opportunity,” von Moltke said.