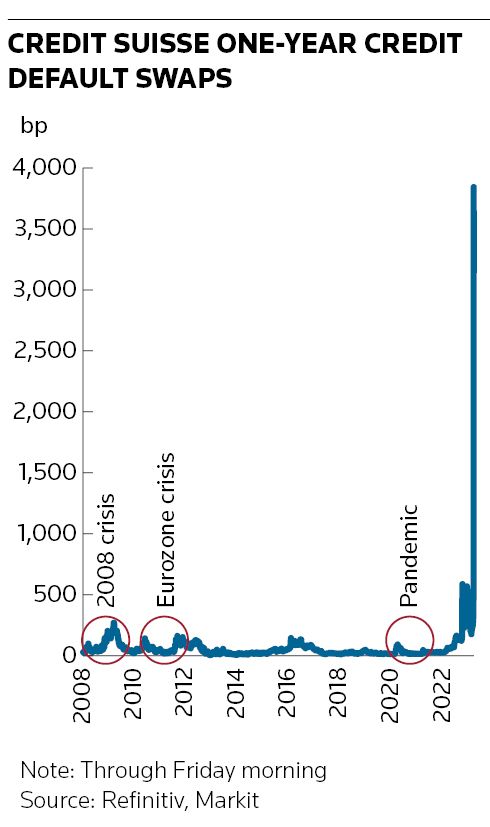

Credit default swaps referencing Credit Suisse were stuck at distressed levels on Friday despite the Swiss National Bank moving earlier in the week to shore up confidence in the embattled lender, a sign that traders in these markets remain highly concerned about a near-term debt default.

One-year Credit Suisse CDS was being quoted at about 3,280bp on Friday, according to Refinitiv, up from around 240bp at the start of the month. Buying CDS is one way for traders to protect themselves against the increased risk of a company going bankrupt. Banks’ counterparty risk management desks are among the heaviest users of these derivatives to manage trading exposures to other firms.

One senior bank trader said his firm still dealt with Credit Suisse, albeit under stricter conditions than it would with other major banks. But he also noted that banks have been tracking their exposure to Credit Suisse for some time now. His firm, for instance, has been more cautious about the business it conducts with Credit Suisse since the Swiss lender suffered heavy losses following the collapse of Archegos Capital Management in 2021.

“We’ve been monitoring carefully this exposure over the last year or so – and I guess all banks have been doing that. It’s not just yesterday or the day before” that this started happening, the trader said.

It's not clear how many CDS trades on Credit Suisse are changing hands at these distressed levels, where it typically becomes prohibitively expensive to transact in any size. Short-dated CDS referencing the Swiss bank are trading far above longer-dated contracts at present, another tell-tale sign of the heightened default worries despite the bank's undeniably strong financials.

Dipak Chotai, founder of consultancy JD Risk Solutions and the former head of risk management for UBS’s fixed-income business, said it was not really possible to protect yourself against Credit Suisse from a hedging perspective any more given the extreme levels at which CDS were being quoted.

“There’s probably very little liquidity out there and it’s getting to a point where the price you’re paying isn’t necessarily equal to the amount of recovery you can achieve – so you’re not really buying protection at all,” he said.

Lower exposure

Banks’ counterparty exposures to one another have fallen considerably since the 2008 financial crisis thanks to regulations that require most trades to be funnelled through central clearinghouses and increased margining requirements for uncleared transactions.

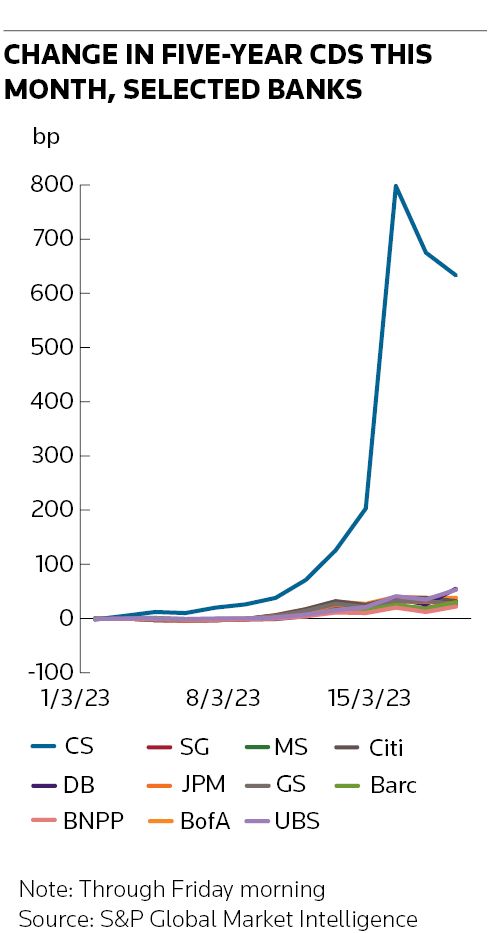

The performance of other bank CDS suggests that traders believe the risks to the wider banking system from Credit Suisse's troubles are contained for now. The cost of default protection on major banks has risen somewhat in the past week, but remains far below crisis levels.

Five-year CDS on Deutsche Bank and UBS are both up by more than 50bp this month to 143bp and 117bp respectively, according to S&P Global Market Intelligence, marking them out as the worst performers among the major investment banks. But that's still a world away from Credit Suisse's five-year CDS being quoted at nearly 1,000bp.

"Hopefully the situation is going to stabilise. But, at the end of the day, there will be clients not willing to deal with Credit Suisse any more; there will be counterparties not willing to trade with them and there will be counterparties questioning whether they should deal with other banks,” the senior trader said.

Chotai said the post-crisis regulations on margin and clearing for derivatives trades meant that “the risks of this situation are different to what we’ve seen in the past". As regards Credit Suisse, he suggested legal analysis rather than financial hedges could be the crucial factor now.

"What’s more important for Credit Suisse’s counterparties is to really understand what your contractual rights are on your ISDA documents and your margin agreements. Ultimately, that’s the best risk management you can do at this stage, as hedging isn’t really a possibility any more,” he said.