Aroundtown announced plans last week to shore up its capital and tackle near-term liabilities as the German real estate owner battles to get back on an even keel, although a crushed share price and bonds trading at double-digit yields suggest more pain lies ahead.

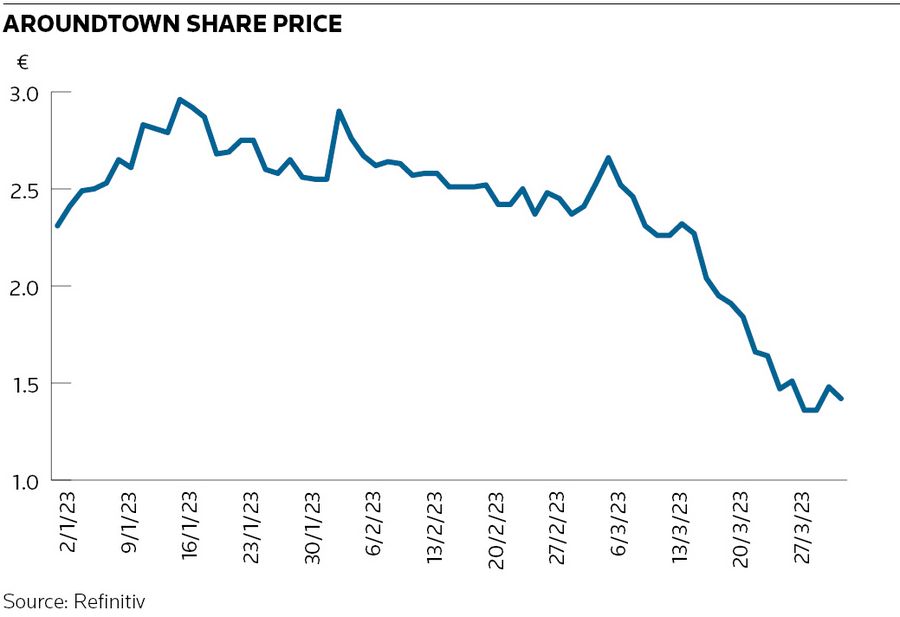

The company's share price, around €1.48 on Thursday, is down almost 35% this year. It is the third-worst performer in the pan-European Stoxx 600 index in 2023, behind Direct Line and beleaguered bank Credit Suisse. Its euro-denominated 1% January 2025 senior bond is trading in the mid-12% area, according to Refinitiv, or a cash price of 83.

In a sign of the pressure it is under, Aroundtown said in its annual results presentation on Tuesday that it was suspending dividend payments to preserve capital. The move followed a similar announcement earlier in March by Grand City Properties, in which Aroundtown has a 59% stake. Aroundtown also launched a tender offer below par on a series of senior bonds, its second such exercise this year, to reduce its short-term debt burden.

Some investors continue to hold a negative view on the company. Aroundtown has net tangible assets per share of €9.30, according to the European Public Real Estate Association, "yet the market will not buy the shares at a vast 85% discount to NTA”, said Orlando Gemes, chief investment officer at Fairwater Capital. "Who exactly wants offices, residential [properties] and hotels in Germany, European commercial real estate, apartments in Croydon, exposure to Center Parcs and developments?"

Other investors have a more hopeful outlook and believe the company has finally started to tackle its problems, including its indebtedness. Aroundtown's loan-to-value ratio is about 54%, after including its hybrids and making other adjustments, according to CreditSights.

"What I've heard this week was a complete U-turn in terms of looking at their financial priorities," said a fixed income investor. "What they are doing is the sensible stuff, building up cash by selling assets. They are doing the right thing by cutting the dividend – the next line of defence is raising equity, and then the last would be cutting the coupons on the hybrids."

That was something the company had hinted last year it would consider but subsequently backtracked on, though it – and Grand City Properties – decided against calling their hybrids in January.

Instead, they have targeted equity holders by suspending dividend payments. Aroundtown said it did so because of "the increase in macro-economic uncertainty and volatility, with currently limited visibility on the full impact of the current market environment on valuations, increasing financing costs and limited access to capital markets ... it is better to preserve cash and equity, thereby strengthening the balance sheet and better positioning the company to navigate the uncertainties ahead".

Cash through the door

Aroundtown is sitting on €2.7bn of cash, helped by €1.6bn of disposals in 2022 and another €150m so far this year. The company said cash, liquid assets and expected proceeds of signed disposals will cover debt maturities until the end of 2025.

The company, rated BBB+ by S&P, is using some of its cash to finance a tender offer targeting €400m of its senior bonds due in 2025 and 2026 through an unmodified Dutch auction.

Aroundtown in January had already bought back €110.5m of two notes due in 2025. It had been offering to buy back up to €300m, and a banker said the fact that some of the cash available for the buyback was not used showed that Aroundtown could afford to act again to manage upcoming maturities. It will also provide bondholders with liquidity.

But January's tender offer left some investors disgruntled, with one of the charges being that the company itself had triggered the drop in its bond prices through muddled messaging last year around its hybrids.

Gemes said the company could have bought back its series of hybrid bonds – Aroundtown and GCP have hybrids outstanding with a face value of around €4.8bn-equivalent – but was instead taking advantage of the depressed prices of the senior bonds.

"People say these are BBB+ senior bonds which are money good," said Gemes. "The buyback is happening at 71–83 – that is not money good. They are not buying back the hybrids but taking the chance to reduce debt and improve the balance sheet at a discount price."

Losing the battle

The hybrids, which are rated BBB– and had been callable in January, were left outstanding given the prohibitive cost of refinancing. They had been trading at about 75 but are now quoted at 47.

"The bondholders have given up on the hybrids," said the fixed income investor, adding that they were highly illiquid. "The buyer base has deserted that instrument. But the spreads on the senior unsecureds are also around 700bp–800bp, which is very much not investment-grade but rather distressed."

The chances of a return to the capital markets in the near future appears remote given the cost of bond financing, and damaged relations with the buyside. "Aroundtown in my mind has gone into a bunker and is trying to survive a future battle," said the fixed income investor. "They are tainted with bondholders. Prices can start to move up if we have new investors – hedge funds, distressed buyers – saying 'it looks stupid cheap, let’s just buy it'. But they've lost a lot of goodwill."

Aroundtown did not immediately respond to a request for comment. The company has been concentrating on secured bank financing. It had unencumbered assets of €22.2bn as of December and said it had high headroom before it would breach bond covenants.