Goldman Sachs’ trading division has regained its swagger in recent years, comfortably outpacing growth at rivals to once more become the most profitable markets business around.

Now, the Wall Street giant is looking to cement its position in the most precarious environment the banking system has faced since the 2007–08 financial crisis.

“We just got our first taste of contagion that can be linked to cumulative rate hikes,” Ashok Varadhan, Goldman’s co-head of global banking and markets, told IFR in a video call shortly after the collapse of Silicon Valley Bank and UBS’s emergency rescue of Credit Suisse.

“You never would have thought that a venture capital bank in Northern California seeing US$42bn of withdrawals would lead to Credit Suisse being sold to UBS on a weekend. It’s a healthy reminder of how the interconnectedness of sentiment can lead to knock-on effects you never would have anticipated.

"My job is to make sure that we contingency plan so that our business is okay whatever the state of the world,” he added.

Varadhan knows all about crises having started at Goldman in 1998 just as Long-Term Capital Management teetered on the brink of collapse. He therefore represents a vital link to Goldman’s storied past of swashbuckling traders when the bank’s reinvigorated markets division is reasserting its importance as a money-making machine.

Even as analysts and investors bemoan Goldman’s smaller presence in steady, fee-earning businesses like wealth management, the US bank has quietly registered its most fruitful period in global markets in over a decade.

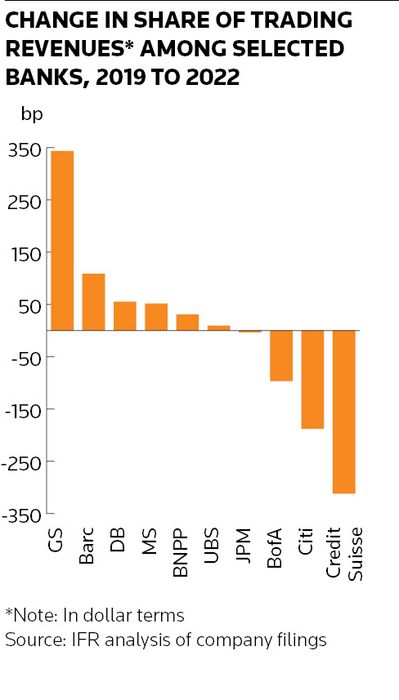

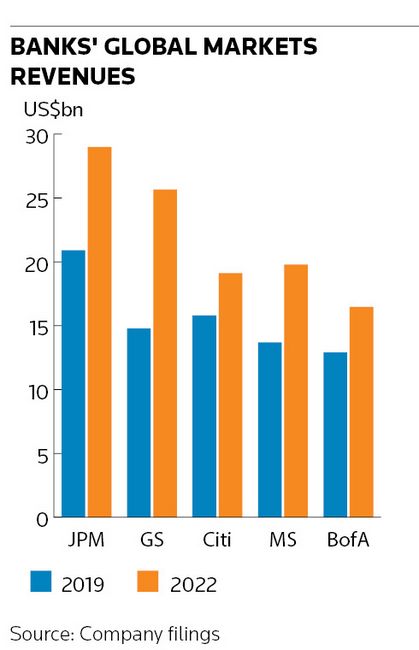

Goldman’s trading revenues have jumped 74% since 2019 to US$25.7bn last year amid the sustained rise in market volatility that accompanied the outbreak of the pandemic in 2020. That compares with an average revenue increase of 33% among the other big four US banks. As a result, Goldman has expanded its market share of trading revenues among its main rivals by 3.4 percentage points over that time to 17.1%, putting it ever closer to long-time top dog JP Morgan at 19.3%.

And it has done all that while becoming far more profitable than its peers. Last year, Goldman’s banking and markets division reported a return on equity of 16.4%, well above JP Morgan’s 14% and Morgan Stanley's 10%. Taken as a whole, it represents a remarkable turnaround for a part of the bank that had appeared to lose its lustre in the low-volatility years preceding the pandemic – a period when investment bankers increasingly came to populate Goldman’s senior ranks, including chief executive David Solomon.

Varadhan attributes the slump in industry trading revenues in the pre-pandemic era to a combination of post-crisis regulations, which meant banks had to hold more capital and reduce leverage dramatically, and central banks setting interest rates near zero, which squashed volatility. “In retrospect, if I was cooking up a cocktail of what would be most deleterious to our markets business, it would be those two things happening at once," he said.

Things changed in 2020 with the onset of the pandemic. Investors needed to reshuffle positions and firms like Goldman were well placed to help them do so. By this time, the bank had identified three strategic priorities within markets it believed would turbo-charge its operations: trading more with its biggest clients, offering them more financing, and keeping a lid on expenses.

“We’ve made sure that we can capture whatever cyclical opportunity arises,” said Varadhan. “The fact that we're global, broad and deep across our markets business, the fact that clients wanted certainty of execution following a shock of that magnitude [with the pandemic], the fact that we were in very strong financial health – and operating from a place of strength rather than weakness – enabled us to really differentiate ourselves with clients.”

Stickier revenues

Goldman says it now holds a top three position in FICC and equities trading with 77 of its top 100 clients, compared with 51 in 2019. Financing has grown from 12% of its markets revenues in 2013 to 22% of its revenues last year, worth US$7.1bn in total.

The US bank isn’t alone in believing such strategies will make markets revenues more stable and reliable. Rival firms are also looking to lend more money to hedge funds and other investors to leverage positions to bring greater diversification to their businesses.

Focusing on transacting more with big clients, so that banks can benefit from the huge asset growth at large investment managers in recent years, has been another popular ploy. So-called alternative asset managers held an estimated US$15trn of assets last year, Goldman said citing Preqin data, up from US$6trn in 2013. Assets are projected to grow to US$23trn by 2027.

“People love wealth management, partly because it’s not capital intensive, but also because the business grows with the accretion of a client’s wealth. In reality, the markets business is not too dissimilar,” said Varadhan.

“If Millennium [Management]’s assets have doubled in size, they’re going to require twice as much intermediation and twice as much financing. So as their assets under management have gone up, the revenue production of our business has also gone up. Unlike wealth management, our financial resources also have to go up, but there are economies of scale that give you elasticity to the upside that I don’t think the market gives credit for,” he said.

Warehousing risks

And what about the recent volatility that has enveloped financial markets, with the crisis among US regional banks and UBS’ emergency rescue of long-time rival Credit Suisse conjuring up memories of the financial crisis? While analysts don't expect well-capitalised, profitable banks like Goldman to run into trouble in this environment, near-term market moves can still prove painful for trading desks.

Swings in government bonds have already pummelled macro hedge funds, while the Financial Times reported Goldman’s rates trading desk lost about US$200m last month. A renowned macro trader himself – who became one of Goldman's youngest partners at 29 – Varadhan is philosophical about such episodes.

“Anytime you have an exogenous shock it’s always hard for anyone in the reinsurance business. A big part of what we do in providing principal liquidity to clients is we end up having to warehouse risks,” he said.

He compares the situation to an insurance company that has to pay out claims to clients after a hurricane, while seeing the future value of its business increase significantly as more people decide to take out policies to protect themselves.

“Once you reach that new equilibrium, there’s a lot of business to do and my sense is we’re working through that right now. We had a very strong 2020, but those first 10 days of the pandemic were very scary,” Varadhan said. “The last week hasn’t been fantastic in terms of our legacy positions. But relative to the pandemic, the headwinds the economy is facing are fairly small, so once we have more clarity with respect to monetary policy, that should lead to more certainty and more deal activity.”

Rivals often invoke Goldman’s risk-taking expertise to explain the huge strides it has made in recent years. In an era where it has become unfashionable to discuss such things openly, Varadhan was refreshingly frank about Goldman’s celebrated culture around trading and risk management.

“You can’t service hedge funds and asset managers without being like-minded and having comparable prowess,” said Varadhan, noting the prominent roles former colleagues such as Pablo Salame and Paul Russo have taken at Citadel and Millennium Management, respectively.

"That’s a hallmark of ours and it's a part of our identity that I'm personally very proud of and want to foster. There’s no free lunch – there will be times when you get on the wrong side of a trade – but over the long run, I think it will differentiate us in a good way,” he said.

There is also an emphasis on communication between Goldman’s senior partners – particularly at times of crisis. On the weekend when UBS bought Credit Suisse, Varadhan was on video calls with senior traders from across the world to wargame different scenarios and how that would affect a range of markets. Varadhan is also in regular contact with Solomon – often talking more than once a day – and spoke to him around 15 times in the week before IFR's interview.

Reaching the limits

Notably, Goldman is one of the last investment banks to maintain a fully fledged commodities trading unit, which has proven a significant advantage in recent years as natural resource prices have whipsawed.

Varadhan sees the rates business and fixed income more broadly as being an area of focus.

“Interest rates as an asset class were largely dormant. Now people have to immunise themselves from interest rate risk, as we learned with SVB,” he said. "If rate hikes are now in the last innings, then you should see a lot of allocation to fixed income."

A peaking in the US Federal Reserve's hiking cycle, and potential slowdown in the US economy, could lead Goldman to trim headcount further, Varadhan said, as it retains its focus on costs. So are we reaching that turning point in Fed policy after about 500bp of rate hikes in the space of a year?

“My sense is we’ve reached the limits,” Varadhan said. “There’s been such a dramatic policy shift and up until Silicon Valley Bank there hadn’t really been any contagion associated with it. We finally saw that this economy is penetrable."