Extreme volatility in government bond markets has sparked a regional banking crisis and battered investors from macro hedge funds to UK pension schemes. It’s also proven hugely profitable for bank trading desks specialising in a complex breed of derivatives linked to interest rate moves.

The top 25 banks made US$2.7bn trading interest rate options and so-called non-linear rates in the first quarter, according to data provider Vali Analytics, more than double their haul a year earlier.

Citigroup, Goldman Sachs and Morgan Stanley are among the top firms benefiting from the options trading boom, reinforcing the bumper revenues in their rates trading businesses over the past year. That has come amid a surge in volumes as hedge funds and other investors have used these derivatives to take leveraged bets on the direction of interest rates.

"Interest rate options have become a more important part of our business now,” said Pedro Goldbaum, global co-head of rates at Citigroup.

“More volatility leads to more hedging and increased volumes. Hedge funds have also been active in trying to capture big macro trends, and expressing those views through options gives them a lot of leverage – they can invest a little bit of capital and get outsized returns,” he said.

Central banks raising interest rates at the fastest pace in decades has provided a bonanza for banks’ macro traders following a particularly fallow period for these desks in the calmer years leading up to 2020.

Interest rate volatility has surpassed levels reached at the height of the financial crisis in 2008 by some measures, notably at the front end of the curve as traders have scrambled to gauge when the US Federal Reserve will pause its hiking cycle.

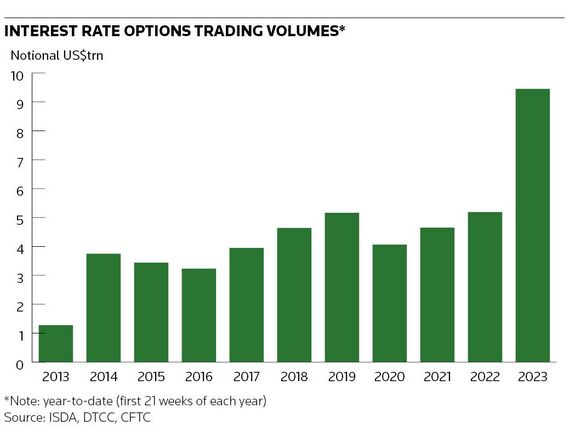

That backdrop has reinvigorated the business of buying and selling interest rate options, a type of derivative popular with hedge funds and other investors looking to wager on (or shield themselves against) changes in interest rates. Nearly US$10trn notional of these derivatives has changed hands so far this year, according to data compiled by ISDA, an 82% jump from 2022.

The severity of the rate market moves has also proved to be a headache at times for some, underlining the risks for banks in selling these instruments. Goldman’s interest rate options desk lost hundreds of millions of dollars around the time of the sharp market reversal in March when the regional banking crisis intensified, according to sources familiar with the matter.

Daily moves in two-year Treasury yields exceeded 20bp more often this March than in September 2008 when Lehman Brothers collapsed, according to Refinitiv data. That included a stomach-churning drop of 61bp on March 13, a few days before Silicon Valley Bank’s failure.

Goldman still made about twice as much revenue in options trading in the first quarter compared with a year earlier despite the losses, sources said, showing just how profitable this activity has become. Goldman declined to comment.

Leveraged bets

Interest rate options can take various forms, but one of the most popular structures is a “swaption”. This is where investors pay an upfront premium to have the right – though not the obligation – to enter an interest rate swap during a set period of time.

A portfolio manager who thinks, for instance, that rates are going to rise can buy a “payer swaption”. If the manager is proved right, they can exercise the option and receive a floating coupon that rises in line with market interest rates, while paying a lower, fixed coupon in return.

If the manager is wrong, and market interest rates fall during the swaption’s life, they can simply walk away from the trade, capping their downside to the premium paid for the cost of the option. That contrasts with a regular interest rate swap (or trading US Treasury bonds) where the only way to staunch losses is to close out the trade.

"Options are generally much more palatable for funds [compared with regular interest rate swaps]. There’s limited downside to the trade, but your returns can be really magnified,” said Goldbaum.

Options allow investors to amplify their returns using one of the oldest tricks in finance: leverage. Buying a government bond to bet that interest rates won't rise any further, for instance, usually involves investors shelling out the entire value of the security upfront. The initial outlay for a derivative can be a fraction of the size, typically confined to the option premium plus any additional margin the dealer requires. That can allow investors to make much bigger returns (or losses) on a small amount of capital.

Flow over structured

Trading options was less appealing during much of the previous decade when central banks kept interest rates pinned near zero. Most activity then centred on options embedded in structured notes, which dealers could strip out and sell to other clients.

The most famous of these are Formosa bonds – callable US dollar debt sold to Taiwanese life insurers. That market has tailed off over the past year as higher rates, a stronger dollar and fewer notes being called has dampened new issuance.

Now, options trading is more focused on the “flow” activity of investors such as hedge funds taking views on interest rates. The majority of that – about 60% of trades by notional – has come in US dollar markets, as the Fed’s actions have taken centre stage.

But euro markets have also been busy as the European Central Bank has lifted interest rates, with euro options accounting for 30% of overall volumes. A Morgan Stanley team led by Wolfgang Pammer, global head of structured rates trading, has been particularly active in the EMEA region, according to sources. Morgan Stanley declined to comment.

"These are the best rates trading conditions I've probably ever seen," said Goldbaum. “It’s been a great rates trading environment for over a year now. That means you invest more in the business – you deploy resources to the business.”