Global regulators in the coming weeks are set to outlaw certain "credit-sensitive" alternative reference rates to US dollar Libor, according to sources familiar with the matter, dealing a blow to parts of the finance industry that had lobbied for greater choice when replacing the controversial benchmark.

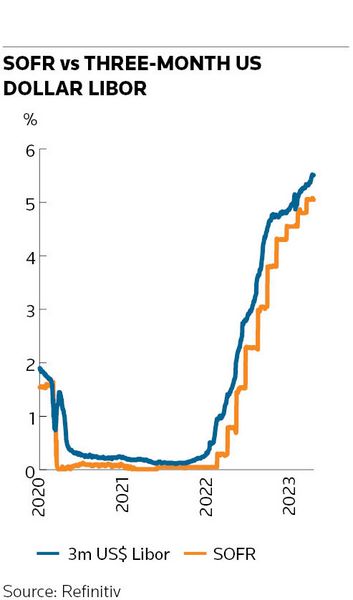

US dollar Libor will cease to exist from June 30, cementing the transition of more than US$200trn of financial products to other reference rates. Most of those instruments, such as derivatives, bonds and mortgages, have been migrating to regulators’ preferred replacement, the secured overnight financing rate.

The commercial loan market, though, has been slower to transition, with regional US banks in particular clamouring for a credit-sensitive alternative to the risk-free SOFR that instead tracks banks’ borrowing costs in a manner more akin to Libor.

Despite those pleas, the International Organization of Securities Commissions is set to rule that these new credit-sensitive rates do not comply with its standards for financial benchmarks when it publishes its final report on US dollar Libor alternatives this summer, sources said, effectively ending the prospect of their widespread adoption. IOSCO, which sets global standards for securities markets, declined to comment.

Regulators have made no secret of their scepticism about the various credit-sensitive rates that have emerged in recent years as alternatives to Libor. Edwin Schooling Latter, who until recently was the UK Financial Conduct Authority’s director of markets policy and chaired IOSCO's Task Force on Financial Benchmarks, said in a 2021 speech that regulators didn't want activity to shift to these rates.

“Authorities in both the UK and US have warned publicly about the risks embedded in these [rates]," he said. “They share many of the same flaws as Libor.”

That chilly reception has already put a dampener on activity linked to SOFR alternatives. “Cold water was poured on them from regulators on both sides of the Atlantic and from what we can see there’s limited appetite for these other rates,” said Richard Gibbard, counsel in the financial markets and products team at law firm Fieldfisher.

Dragging feet

A ruling that credit-sensitive rates aren't sufficiently robust will disappoint US regional banks that have argued they need such benchmarks to use in their lending activities. Libor loans still account for about 55% of the holdings in collateralised loan obligations, according to Barclays, making bank loans by far the slowest market to drop the troubled rate.

Some say there are good reasons for that foot-dragging. Forcing banks to price their loans off SOFR may create a mismatch between their assets and liabilities during stressed markets, they say, as banks’ borrowing costs will increase faster than the interest rates on the loans they’ve made. That could cause serious problems for the banking system, critics say.

It was exactly those concerns that led to the development of benchmarks reflecting banks' financing costs – which should eliminate the problem – after regulators signalled their intent to replace Libor.

Rates such as the Bloomberg Short-Term Bank Yield Index and American Financial Exchange’s Ameribor have looked to fill that role. These benchmarks calculate banks' short-term, unsecured financing costs using transactions such as overnight loans, commercial paper issuance, certificates of deposit and short-dated bonds.

Bloomberg and AFX did not comment for this story. Both companies have previously said they are compliant with IOSCO’s benchmark principles. Bloomberg also secured a third-party opinion for its “BSBY” index from accounting firm EY to support that assertion.

Difference of opinion

Regulators see it differently. For them, the main stumbling block is whether these rates are calculated using enough concrete transactions. Some banks routinely fabricated their Libor submissions and trades tended to dry up during times of market stress, leaving the benchmark vulnerable to manipulation.

Gary Gensler, US Securities and Exchange Commission chair, has flagged similar concerns around the new credit-sensitive rates. In a 2021 speech, he singled out BSBY – the then frontrunner in the group – and said he didn't believe it met IOSCO standards.

“BSBY has the same inverted-pyramid problem as Libor,” he said. “Like with Libor, we’re seeing a modest market, shouldering the weight of hundreds of trillions of dollars in transactions. When a benchmark is mismatched like that, there’s a heck of an economic incentive to manipulate it.”

In US dollar markets, there was a median of 32 three-month commercial paper trades per day in the first half of 2020 worth a total of US$873m, according to the Financial Stability Board, although that plunged by 75% to five trades worth US$214m in the Covid-induced market turmoil in March 2020.

“The markets underpinning BSBY not only are thin in good times; they virtually disappear in a crisis,” Gensler said in his 2021 speech.

That contrasts with SOFR, which uses US Treasury repo trades. Daily volumes were consistently above US$800bn in 2020 and remained robust during the March market stress, according to the Alternative Reference Rates Committee, the industry body convened by the US Federal Reserve to help US dollar Libor transition.

“We chose the repo market because it has held up for decades [including] through the financial crisis,” said David Bowman, senior associate director at the board of governors of the Federal Reserve System, at ISDA’s annual general meeting in May. “It’s the most resilient market we have.”

Additional reporting by Natasha Rega-Jones