Banks’ macro traders are delivering another bumper set of revenues in this year’s choppy markets, reaffirming their position as a crucial money-making engine and drawing a contrast with macro hedge funds that have struggled to replicate 2022’s heady returns.

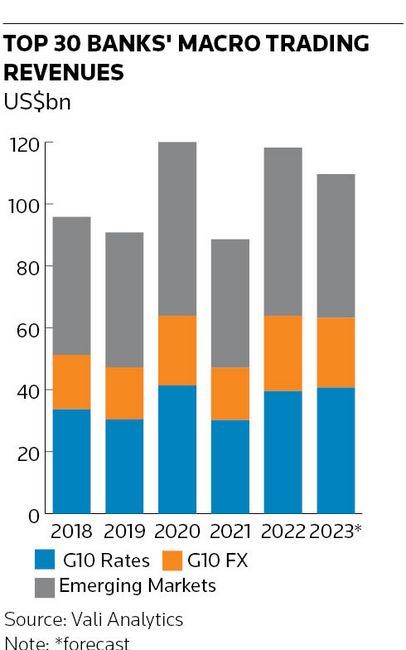

The top 30 banks are on track to make about US$110bn in macro trading revenues this year, according to forecasts from data provider Vali Analytics. That’s 21% above 2019’s level, the last pre-pandemic year, and within touching distance of the record hauls in 2020 and 2022.

Those revenues, which encompass trading in products linked to interest rates and currencies, come despite the macro trading environment becoming far more treacherous this year. Hedge funds have suffered as occasional sharp reversals have punctuated otherwise meandering market moves, with the asset-weighted HFRI Macro (Total) Index losing 1.5% so far in 2023, according to data provider Hedge Fund Research.

Senior bankers say they have adapted to the febrile market conditions, where government bond yields have swung as much as 60bp in a day, by reining in risk and keeping a close eye on crowded positioning that could trigger sudden gyrations.

“The absence of clear trends – or ones that appear less consistent with the fundamentals – has made this year's market much harder to trade,” said Tom Prickett, head of EMEA rates trading at JP Morgan.

"The market moves that we're seeing, especially in rate markets, are proportionally large compared to similar periods in the past,” Prickett said. “Intraday liquidity is lower. That means participants have to be more mindful of where there might be a build-up of position within the market.”

The strength of macro desks has further cemented their importance at the heart of investment banks’ operations, providing a consistently large stream of revenues that has helped offset a decline in dealmaking activities over the past two years. Investment banking fees are forecast to slump to US$70.5bn this year, according to Vali Analytics, a 44% decline from 2021’s peak.

The revival of rates trading in particular marks a departure from much of the previous decade when a combination of higher capital requirements and central banks pinning interest rates near zero crimped returns. The outlook for the business improved materially in 2020 when the outbreak of the pandemic convulsed markets. That continued last year when central banks raised interest rates at a breakneck pace in an effort to bring down inflation from multi-decade highs.

Macro returns

Macro hedge funds also capitalised on a series of clear trends which emerged last year such as a steep increase in bond yields and a surging US dollar. Hedge Fund Research’s macro index gained 8.6% in 2022, its best return in 12 years. But 2023's volatile markets have exposed a chasm in performance between these fund managers and the bank dealing desks that service them.

Rangebound bonds and currencies combined with periodic, severe bouts of volatility have repeatedly confounded investors. Bank traders, by contrast, have benefitted from a flurry of activity as clients have reshuffled positions. Interest rate derivatives volumes rose 14% to hit a record US$178trn in the first half of the year, according to trade body ISDA.

“This is still an incredible environment for rates trading,” said Niru Pathmanabhan, co-head of global interest rate products trading at Goldman Sachs. “Unlike macro funds, which are more reliant on a clean macro environment to capture those trends, being a leading market-maker allows us to interact with the whole array of clients and intermediate periods of volatility.”

That’s not to say the swift market reversals haven’t proved challenging for banks too. The US regional banking crisis in March rocked bond markets – including a stomach-churning, one-day drop of 61bp in the two-year Treasury yield shortly before Silicon Valley Bank’s failure. Goldman’s interest rate options desk sustained heavy losses around that time, according to sources, although that business still succeeded in increasing revenues significantly in the first quarter in what was an otherwise fertile period for such activities.

Many firms have pared back their risk exposures in response to the skittishness in markets. Bank of America has reduced its average value-at-risk, which measures how much a bank can lose from its trading positions, by 14% this year to US$93m in its global markets division.

“We're incredibly disciplined about the risk that we carry. This year, market dynamics are very different to last year, and this is taken into account when assessing risk,” said Jan Smorczewski, co-head of EMEA FICC trading at BofA. “With rates looking like they will stay higher for longer, you have to assume that there could well be further market disruptions."

Snigdha Singh, Smorczewski’s co-head at BofA, said there is a “commonality in where the cracks and fault lines" have appeared across financial markets. “Where you have high duration and high leverage is where the pain has been felt,” said Singh, who also heads EMEA markets initiatives at the bank. “People are now trying to look at other places where you might have something similar, be it sovereign debt or private credit or commercial real estate. But the reality is it’s impossible to know where the next surprise will come from.”

Pain trades

Traders have been scouring markets to identify areas where lopsided positioning could again trigger outsized moves. Many analysts attribute the fierceness of the rally in equities over summer to hedge funds scrambling to cover short positions. Crowded trades are also blamed for exacerbating a surge in UK bond yields when inflation ran hotter than anticipated earlier this year. Pathmanabhan said positioning has been a much bigger driver of price action this year compared with 2022, with consensus trades coming under much more pressure.

“We invest a great deal of time and resources into stressing our positions to see how they’ll behave as a function of both fundamentals and positioning," Pathmanabhan said. "What is our ability to exit that risk in a stressed scenario? Is there someone there to take it or will everyone be looking to get out of a very narrow door? That means we naturally don’t like to hold big positions on something that is consensus.”

Banks continue to invest in macro businesses despite the tricky trading conditions, signalling that they believe these activities will keep flourishing in the months ahead. Citigroup is one firm that has devoted more financial resources to rates trading, even as it has cut back in credit trading as part of a sweeping overhaul of that business. Rates and currencies accounted for a record 81% of Citigroup’s fixed-income revenues in the first half of the year, up from 67% two years earlier. Bank of America has also invested in its macro businesses, which accounted for 64% of its fixed-income revenues last year compared with 40% in 2019.

“It’s been a great rates trading environment for over a year now. That means you invest more in the business – you deploy resources to the business,” said Pedro Goldbaum, global co-head of rates at Citigroup.