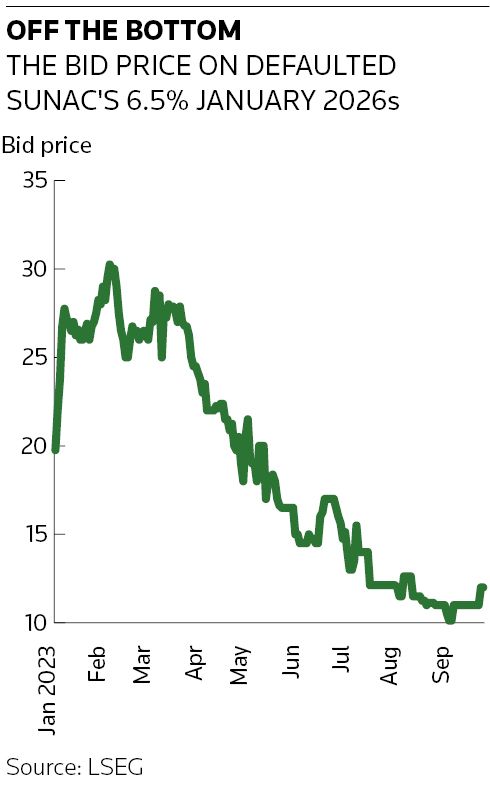

Defaulted property company Sunac China Holdings has secured approval from creditors to restructure its offshore debt of almost US$10bn, the first major Chinese developer to do so.

Other restructurings have stalled or dragged on for months, including that of China Evergrande Group with almost US$20bn in offshore debt, and market participants are hopeful Sunac’s success will nudge others to wrap up their own efforts.

“Sunac got their deal done, and others that are procrastinating should really follow. There’s no point hanging around on these deals,” said a restructuring adviser.

On Monday, creditors holding 98.3% of the outstanding claims approved Sunac's restructuring plan, which will see part of its debt exchanged into mandatory convertible bonds, as well as new conventional notes, and some swapped for shares in Hong Kong-listed subsidiary Sunac Services Holdings. Sunac raised its cap on the MCBs to US$2.75bn in response to investor interest, after initially planning US$1.75bn. The response for the equity-related portions was overwhelming, with the company announcing on Friday that creditors submitted to exchange nearly US$4bn for the MCBs and US$1.34bn for Sunac Services shares.

"The Sunac kind of success story ... is an indication of the kind of things that investors could potentially accept," said Jessica Zhou, a partner at law firm White & Case. "Investors are still looking at the quality of the underlying credit of whatever is offered up."

The restructuring still needs Hong Kong court approval at a hearing scheduled for October 5. Houlihan Lokey (China) is financial adviser to the company and Sidley Austin is legal adviser. PJT Partners and Linklaters are advising an ad hoc group of creditors.

Sources said Sunac's ability and willingness to give investors a menu of options in its restructuring helped speed up acceptance, as the diverse investor base had a range of needs, with some not being able to accept equity or take haircuts.

"A menu plan fares well, and you see it in the voting results," said a source familiar with the situation, noting the options allowed investors to mix and match, and did not force a haircut.

Other developers going through restructurings may not be able to replicate Sunac’s outcome completely as each faces a different balance of onshore and offshore debt, varying complexities of structures and debt-issuing entities, and a mix of long-only bondholders and distressed-debt buyers. But Sunac's success offers some lessons.

Sandra Chow, co-head of Asia-Pacific research at CreditSights, called Sunac's approval a “positive step forward” and a “good blueprint” for other companies, as it used asset sales, a maturity extension and an equity component.

“The company had more willingness to pay and wasn’t trying to squeeze [investors] too hard,” said Chow.

Follow the playbook

The restructuring adviser said a key difference between Sunac and other developers was Sunac’s willingness to manoeuvre through the restructuring process in a straightforward way, negotiating with the ad hoc investor group and following international norms.

“They acted in a way in which they had a certain urgency, as much as the bondholders," the adviser said. "I’d give them better marks than any of the other guys in their willingness to get a deal done.”

One property executive said it is especially hard to reach a consensus on Chinese restructurings because bondholders may have different goals and engage in talks individually, rather than as a group. Onshore and offshore investors also have conflicting views about what to accept in a proposal.

Restructurings by Chinese property developers prior to Sunac have generally involved maturity extensions and reductions in coupons, rather than big changes to capital structures.

“Most of the restructuring cases are buying time,” said the property executive. “Almost all issuers know a haircut is inevitable in order to hold on … but it is not something that creditors and bondholders can easily accept.”

Not holding out for par

The reluctance from investors to accept haircuts is one of the biggest sticking points in stalled restructurings, sources said, but attitudes are slowly changing and investors are taking implicit haircuts in many situations through lower coupons and longer maturities.

Investors are not holding out for par and are willing to recover 35–40 cents on the dollar at this point, said the restructuring adviser.

While company chairs, founders, and other major equity holders have become open to the idea of converting debt to equity, they are often unwilling to dilute their stakes too far.

"Even when you have a dynamic where creditors are willing to equitise meaningful portions of their debt, the challenge becomes how you do that and keep the meaningful sponsor," said the source close to the situation. Major shareholders need to have enough skin in the game to feel engaged in the restructuring and incentivised to ensure the survival of the company, he said.

Sources said many property companies are unwilling to commit to a decision while the outlook is so uncertain.

“A lot of issuers just don’t know what to do,” said the property executive. “The environment keeps deteriorating. Whatever plan you came up with last month doesn’t become that sensible from an issuer perspective.”

Companies that are unwilling to negotiate with investors or continue to hold out for more favourable conditions face a real possibility of being forced into liquidation, sources said. Such was the case with Jiayuan International Group, which the High Court of Hong Kong earlier this year ordered to be wound up after the company had extended the deadline for an exchange offer 11 times.

“They don’t actually believe these creditors will wind them up,” said the restructuring adviser. “I do think you will see some of [the developers] go belly up, and that will push others to move.”

Part of Sunac’s motivation to get its restructuring done may have been the hope that it would benefit from policy support in China, and it has put itself in a position to raise funds again as soon as possible.

The source close to the situation noted that China's supportive policies have so far benefited property companies that are not in default, meaning Sunac is in a better position by resolving its debt problems quickly.

Sunac's restructuring approval has been seen as a positive, but bad headlines continue to mount in the Chinese property sector. Country Garden Holdings, with nearly US$10bn of US dollar bonds outstanding, reportedly missed a coupon payment on Monday, and will be officially in default if it does not make the payment within 30 days.