The euro short-term rate, otherwise known as €STR, has become the default benchmark for the euro leg of cross-currency swaps, a new dynamic that is boosting the adoption of the risk-free rate in derivatives markets more broadly.

The euro area has become an outlier among major financial markets following the decision to reform rather than eradicate Euribor (its version of the troubled Libor lending benchmark) that underpins about US$150trn in financial contracts. But moves by most other regulators to drop Libor from their home markets have increasingly had an impact on derivatives trading norms in Europe in recent months too.

The demise of US dollar Libor in June – and its replacement by the secured overnight financing rate – marked a watershed moment in this shift after SOFR became the reference rate for the US dollar leg in euro-dollar cross-currency swaps. That in turn has fuelled a surge in uptake in €STR, the risk-free equivalent rate in euros, for the European leg of those trades.

Traders say €STR has become the go-to interest rate benchmark for all cross-currency swap transactions involving a euro leg, a trend that has contributed to €STR representing more than a third of trading activity across euro derivatives markets in October compared with about 20% a year earlier, according to analytics firm ClarusFT and trade body ISDA.

“One driver of this activity is the familiarity that clients now have with risk-free rates in other currencies,” said Mark Rogerson, EMEA head of interest rate products at CME Group. “The vast majority of cross-currency transactions include a dollar leg and with SOFR being an overnight index most participants want the non-dollar currency leg to also be an overnight index.”

The last vestiges of US dollar Libor disappeared on June 30, ending a decade-long saga to strip the controversial interbank lending rate from more than US$200trn of financial contracts. That left the euro area as one of few jurisdictions that hadn’t transitioned to a risk-free reference rate for derivatives and other instruments.

More than 85% of trades in the US$35trn cross-currency swap market feature a US dollar leg, according to data from the Bank for International Settlements, while around US$14trn of trades have a euro leg.

Simon Green, head of cross-currency and short-term interest rate trading at Nomura, said 80%–90% of the bank’s cross-currency swap business is now €STR-based for transactions that feature a euro leg, as risk-free rates have become the market standard for cross-currency swaps in interbank trades.

That development means client trades using €STR for the euro leg instead of Euribor will typically face transaction costs that are between a quarter and a whole basis point lower, depending on the size and tenor of the swap. There have been almost 6,500 euro-dollar cross-currency trades worth US$1.06trn since the end of June, according to swap data repository DTCC and ISDA.

“It’s fair to say that the Euribor fixing has been volatile in 2023 so avoiding that uncertainty is something our customers are keen to do,” Green said.

Euribor lives on

Despite this growth, Euribor is still prevalent in financial markets. New debt sales in euros are predominantly pegged to three-month Euribor, said Kilian Frensch, head of euro swaps at Nomura – with the “occasional €STR or six-month Euribor variations”. Most longer-dated interest rate swaps also reference Euribor.

But at the shorter end of the curve, “almost all” derivatives risk exchanged in Europe with a tenor of two years and below is pegged to €STR, said Rogerson. “Benchmark consistency is key. Following the transition to SOFR there has been greater education leading to more operational, back office, and P&L systems support when it comes to using overnight index products,” he said.

Concerns around the future of Euribor are also playing a role, said Lee Bartholomew, head of fixed-income and currencies exchange-traded derivatives product design at Eurex. “In Europe, there’s a lack of clarity from the regulator around whether Euribor continues or whether they follow what the UK and the US did in regards to Sonia and SOFR,” he said. "I think at some point the regulator will look into this in more detail. For now, it appears that €STR and Euribor liquidity pools will coexist".

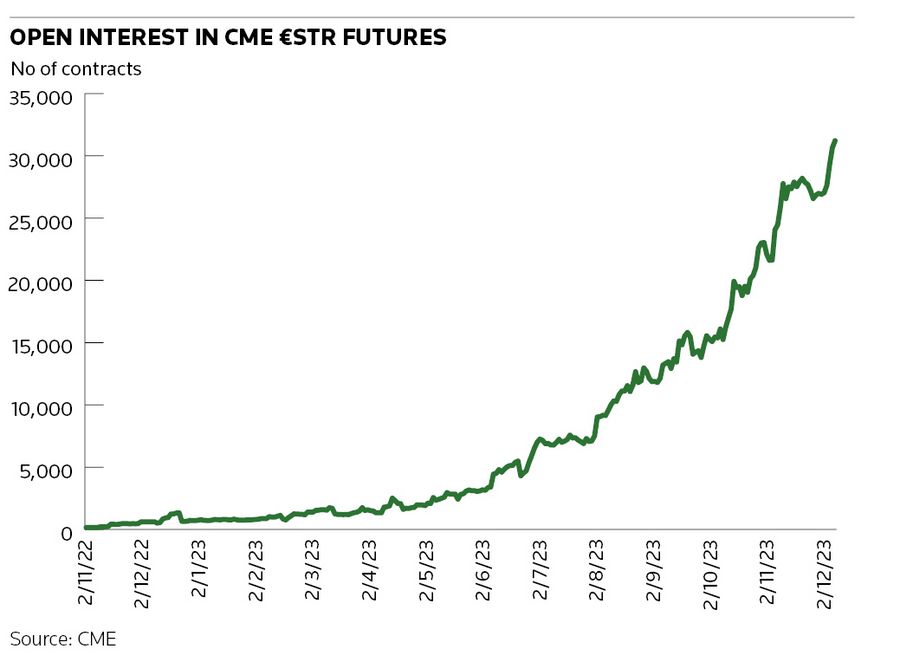

€STR is also registering healthy growth in the listed derivatives space, with CME seeing a rise in open interest for €STR futures to a record 33,900 contracts through November and December. Meanwhile, Eurex saw open interest for €STR futures reach 6,900 contracts in November – representing 17.5% of open interest market share, the exchange said. Both exchanges are planning to launch €STR options in the first quarter while ICE also recently launched its own €STR futures contracts.

“The exchanges are making this a very competitive market from a liquidity provider perspective, but there are genuine end clients looking to trade €STR," said Bartholomew.