Strong technicals and shrinking spreads have sparked a late-year surge in US junk bond issuance as borrowers focus on refinancing the approximately US$1trn in debt maturities due over the next few years.

Pennymac Financial Services, Alliant Holdings, Kinetik Holdings, NextEra Energy, Univision Communications, Crescent Energy, Enova International and Credit Acceptance all tapped the market last week to refinance loans or bonds due in 2024 and 2025. And more are expected to do the same this month.

By Friday, the US high-yield primary market was poised to close the week with nearly US$8bn in new supply from 14 issuers, easily overshadowing in just one week the US$2.27bn from just two issuers in December 2022, according to IFR data. It also sets monthly primary volumes on course to exceed the US$8.25bn which 13 issuers raised in December 2021, before the US Federal Reserve began to hike rates, and it marks the busiest week since September this year during the post-Labor Day rush.

“That is the mantra out there: ‘survive until 25',” said Stephen Repoff, portfolio manager at GW&K Investment Management. “If the market is open and yields are back down closer to 8% rather than 9.5%, then of course everyone wants to go out and take advantage of that.”

Limited supply this year stemming from the high cost of financing combined with investors’ need to recycle hefty coupon and principal payments has buoyed the asset class and are now supporting deals in the primary markets.

“People take for granted how much cashflow is generated by the asset class,” said Nicholas Burns, high-yield portfolio manager at Payden & Rygel. “Year to date, calls, tenders, maturities and coupons account for almost US$200bn in fresh cash that managers need to put to work.”

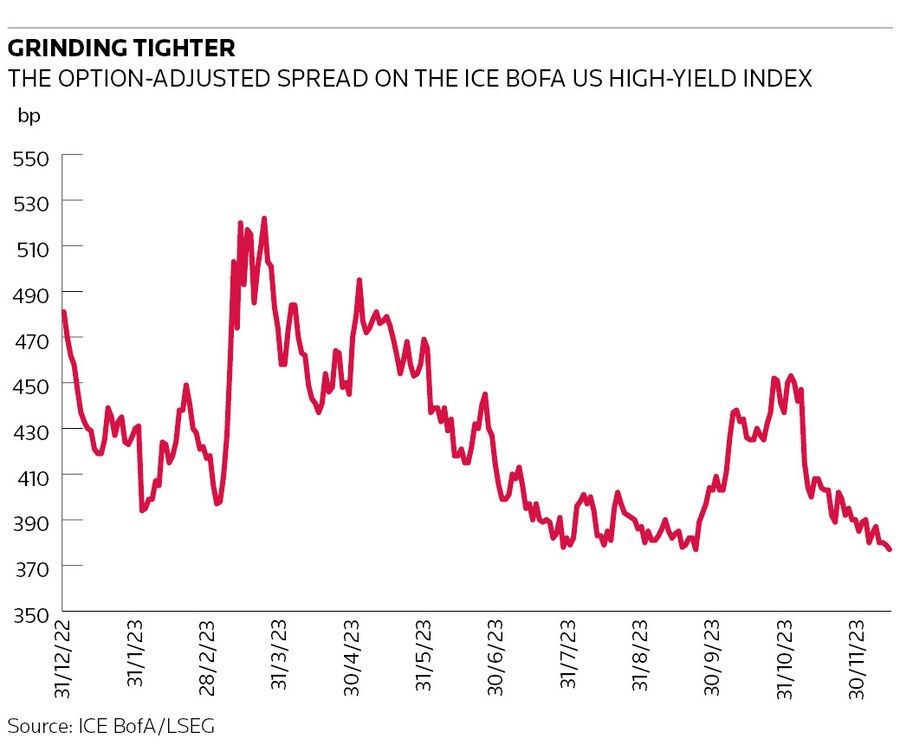

That supply-demand dynamic, plus hopes of Fed rate cuts next year, have helped squeeze high-yield spreads. As of December 5, the average high-yield bond spread was 379bp, 99bp tighter on the year and just 79bp wide of the post financial crisis low of 301bp on December 28 2021, according to ICE BofA data. It’s a similar story for yields. Since October 23, the yield on ICE BofA’s BB/B index has shrunk from 8.7% to 7.34% on December 6.

“Market appetite has risen but the market [in terms of outstanding bonds] has shrunk by almost a third [over the past few years],” said Repoff. “When you don’t have any credit events, it is going to be a positive technical in and of itself.”

No concessions here

That is all good news for corporates facing the painful prospect of refinancing cheap debt raised before the Fed started squeezing monetary policy in March 2022. While funding is nowhere near as attractive as it once was, borrowers have at least been printing trades in recent weeks with little to no concession to their secondary curves.

“We are seeing more and more deals coming on the screws, which effectively means they are not coming with material concessions,” said Jordan Lopez, head of Payden & Rygel’s high-yield strategy group.

That also means investors can no longer enjoy much upside post pricing in the secondary market.

“Companies have done a good job of catching the market the right way, but that doesn’t do great things for us in terms of returns,” said Ken Monaghan, co-head of high yield at Amundi US. “We are adding income, but we are not adding price appreciation, so we are doing most of our fishing in the secondary market.”

Mid-stream energy operator Kinetik, for example, issued on Monday a five-year non-call two at par to yield 6.625%. That was the tight end of price talk of 6.75% area and virtually flat to its 5.875% 2029s, which were trading on December 1 at a yield of 6.615% at a lower dollar price of 96.125, according to MarketAxess data. As of Wednesday, the new bonds were trading in a 100.375–100.50 range.

Other borrowers, meanwhile, have sacrificed pricing for size. Univision, for example, increased an add-on to its 8% 2028s to US$700m from US$500m, pricing the deal at 100.50.

While it arguably offered a nice concession on a bond that had been trading as high as 102 before the announcement, according to MarketAxess data, the deal helped it pay down a bigger chunk of its US$1.05bn bond due 2025. The bond was changing hands on Wednesday at 100.625.

It remains unclear whether market conditions will improve in 2024 despite expectations of Fed rate cuts. But for now, many borrowers are reaping the benefits of strong conditions to whittle down maturity walls.

“The last few weeks has been very attractive [for borrowers],” said a senior banker. “Some are saying 'I am okay paying for a maturity project because 2024 could be tougher'.”

Corrected story: Corrects December 2021 and 2022 volumes and updates weekly issuance in third paragraph